elf0724/iStock via Getty Images

The bearish arguments against Hudson Pacific Properties (NYSE:HPP) seem strong as the mainly San Francisco-focused office REIT faces a disruptive post-pandemic economic reality. Working from home, once thought to be an exceptional measure to contain the spread of the virus has undeniably now morphed to be a pillar of the new ways of working. This has driven the 5.28% short interest in Hudson Pacific and has been a factor along with rising interest rates that’s contributed to its stock price declining by nearly 60% on a total return basis year-to-date.

Hudson Pacific owns 55 office properties measuring 16.7 million square feet. These are all located on the US West Coast and Vancouver. The company also owns studio properties across Los Angeles and London, England. Hudson Pacific recently acquired Quixote Studios in September, a firm that provides sound stages and production services to the entertainment industry. The $360 million acquisition will strengthen the company’s core studio offering and will mean it continues to meet strong secular demand for content production.

The Bearish Vision For Leasing Activity

I’m attracted to the company’s portfolio which holds a number of iconic properties like San Francisco’s Ferry Building and 901 Market Street. A large number of Hudson Pacific’s tenants are also technology firms with Google, Amazon, Netflix, Nutanix, and Riot Games forming the top five tenants and 28.1% of annualized base rent as of the end of the company’s fiscal 2022 third quarter. Google alone accounts for 13.1 of the annualized base rent. Admittedly, this is quite a high level of tenant concentration and creates another layer of risk. Technology companies have in recent months initiated large layoffs and signaled an intent to slim their office footprint. Hence, Hudson Pacific could experience some weakness in leasing activity just as interest rates peak and the economy is forecasted to fall into a recession.

It’s clear what the bleak near-term vision the bears are spelling out here is. One where FFO gets compressed by increasingly poor occupancy rates from weak leasing demand. This situation becomes even more destructive against a rising rate environment which would discombobulate the corporate debt market and make it marginally more expensive for Hudson Pacific to finance developments. The Fed, on the back of a 50-basis point hike last week, anticipates rates rising by three-quarters of a percentage point in 2023 to hit a 17-year high of 5% to 5.25% from its current level. However, at the end of its third quarter, 91% of Hudson Pacific’s unsecured and secured debt was fixed or hedged and came with a weighted average term of maturity of 4.4 years. This is bullish and reduces the overall stress on their financials from the current rising rate environment.

The company’s financials continue to be somewhat strong with over 380,000 square feet of leasing activity during its last reported fiscal 2022 third quarter. Rent spreads were also positive at 8.7% GAAP and with total revenue of $260.4 million, up 14.4% over the year-ago quarter.

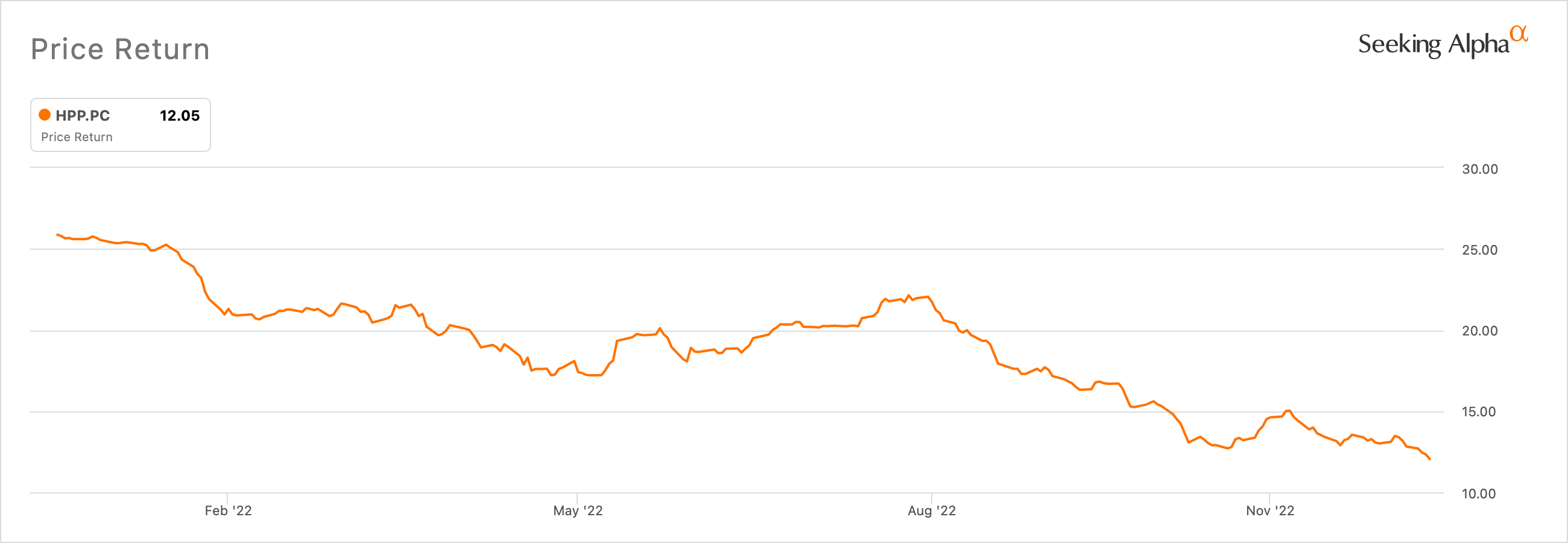

Why The Preferred Shares Are The Way To Go

QuantumOnline

Hudson Pacific Series C Cumulative Preferred Stock (NYSE:HPP.PC) offers a great way to gain exposure to the company. These have fallen materially year-to-date to trade at $12.16, a 51% discount to their $25 redemption value. Essentially, Hudson Pacific will pay holders of its preferred $25 for each share at a certain time on or after the 16th of November 2026. Further, the company will also pay a $1.1875 annual coupon which currently amounts to a 9.8% yield.

Seeking Alpha

The company issued the preferred towards the end of 2021, offering 16 million shares for gross proceeds of $400,000,000. Annual interest will come in at around $19 million which is more than covered by FFO. Indeed, FFO, excluding specified items, for the company’s last reported third quarter was $74.1 million. Whilst this was down from $77.3 million in the year-ago comp, it covers by nearly 4x the dividend paid to holders of the preferred shares. Specified items consisted of a one-time property tax expense of $0.4 million and transaction-related expenses of $9.3 million.

Hence, assuming a full position is entered today and held to redemption, owners of Series C would expect to receive at least $4.45 in dividends and a further $12.84 cash payment. This works out to be a 142% return on investment over a four-year holding period and around 35% annualized. Bears might be right to argue that redemption at the call date is not guaranteed and would be especially unlikely if their bleak vision plays out to reduce the ability of Hudson Pacific to make a $400 million outlay.

Fundamentally, the preferred dividends should be safer than the commons in the event the WFH trend more heavily disrupts leasing activity especially when renewals come up. The current discount to their redemption value looks overdone from a fundamental perspective and represents an opportunity to build a position. I am long.

Be the first to comment