Fokusiert/iStock via Getty Images

Introduction

I’ve written two bullish articles about talent solutions provider Hudson Global (NASDAQ:HSON), the latest of which was in October when I said that many large U.S. companies still aren’t putting the brakes on hiring and that the purchase of India-based recruitment services provider Hunt & Badge which should provide a small boost to Q3 revenues.

Unfortunately, pro forma revenues barely improved in Q3 as Hudson Global saw a reduction in project recruitment process outsourcing (RPO) work as well as a slowdown in hiring activity in the technology sector. In addition, unfavorable foreign exchange rates pushed the company into the red. I’m concerned that days sales outstanding rose to 50 and considering the slowdown in hiring activity in the tech segment is expected to continue in 2023, I’m changing my rating to neutral. Let’s review.

Overview of the Q3 2022 financial results

In case you haven’t read any of my previous articles about Hudson Global, here’s a quick description of the business. The company is involved in the provision of RPO permanent recruitment and contracting outsourced recruitment solutions and currently has direct operations in 14 countries worldwide. The majority of revenues come from APAC and the Americas, and enterprise RPO work accounts for about three-quarters of revenues. The clients include mainly Fortune 500 companies which are concentrated in three main sectors, namely healthcare, financial services, and technology. The remaining quarter of the business consists of recruiter on-demand work for the technology sector and project RPO work. Hudson Global completed two acquisitions in 2021 and 2022 – Chicago-headquartered recruiting services provider Karani in October 2021 and Hunt & Badge in August 2022. The latter focuses on APAC, and this was a small purchase worth just over $1 million.

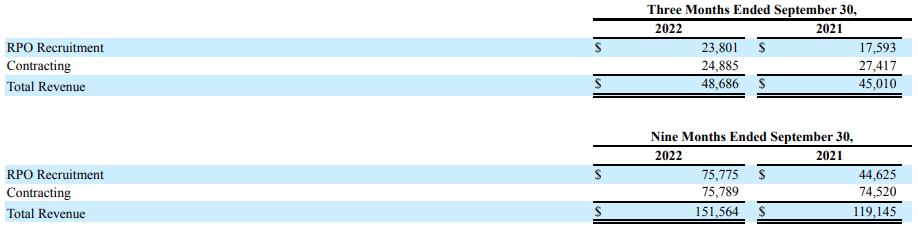

Turning our attention to the Q3 2022 financial results, there was significant growth as revenues rose by 15.9% year-on-year in constant currency to $48.7 million thanks to higher RPO recruitment revenue. Adjusted net revenue, in turn, soared by 41.8% in constant currency to $24.2 million. In Q1 2022, a contracting customer that accounted for $44.9 million of revenues in 2021 ended its agreement with the company and this event can explain why contracting revenue decreased by 9.2% in Q3 2022. SG&A expenses as a percentage of revenues increased due to a lower mix of contracting revenue, where most of the costs are reflected in adjusted net revenue. In addition, Hudson Global experienced operational challenges with two enterprise RPO clients in Q3 – one had disruptions due to implementing new IT systems, while the other was a health care company that spun off part of its business. These issues are likely to have abated by now.

Hudson Global Hudson Global

Hudson Global mentioned during its Q3 earnings call that it experienced a slowdown in hiring activity in the technology sector. Looking at the pro forma financial results, there was barely any growth as Karani accounted for $2.5 million of the revenues for the quarter. Hunt & Badge, in turn, contributed just $18,000 to Hudson Global’s revenues in Q3 2022 (see page 10 here).

Hudson Global

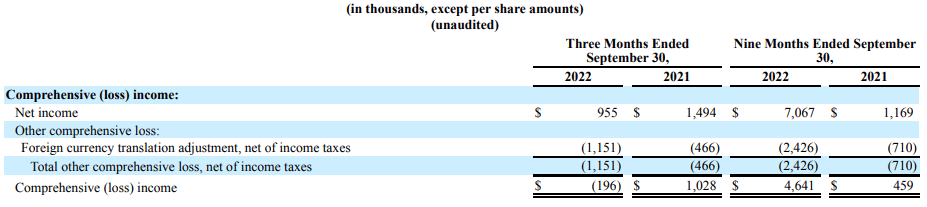

Also, the strong U.S. dollar was a headwind for the company’s financial performance as foreign currency exchange losses pushed the comprehensive income into negative territory. Free cash flow was -$0.4 million in Q3 2022 while cash flow from operations was -$0.1 million.

Hudson Global

Demand for RPO recruiting and contracting services largely depends on macroeconomic conditions as well as labor market strength, and I find the quarterly results of Hudson Global to be underwhelming considering Q2 and Q3 are usually its strongest quarters of the year. Market conditions in Q3 2022 were challenging due to high inflation and interest rates as well as low demand for labor in certain markets. While Hudson Global said during its earnings call that activity at most of its clients remains robust and that its sales pipeline is heavily focused on the health care sector, market conditions are expected to be challenging into the first months of 2023, especially in the tech sector.

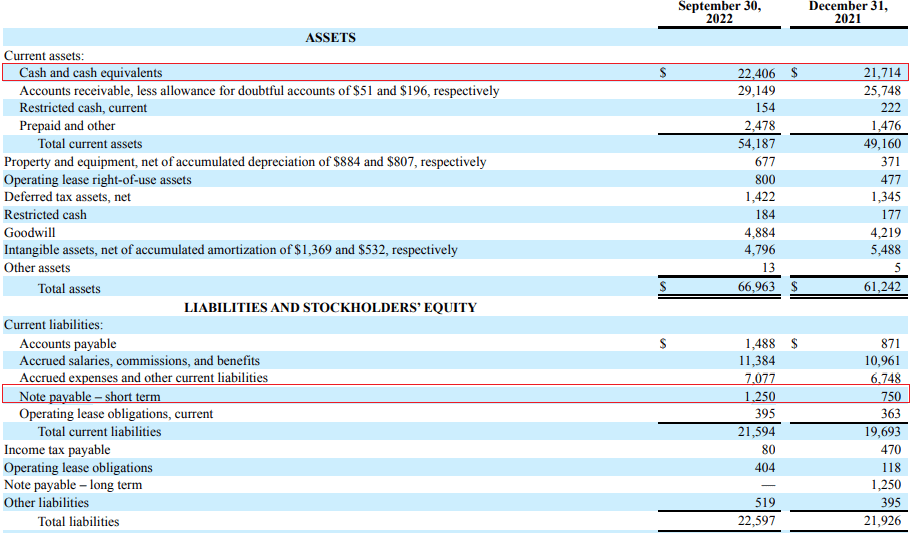

Turning our attention to the balance sheet, Hudson Global seems well-positioned to weather a potential global recession as its net cash position stood at $21.2 million despite the company spending about $1.13 million on share buybacks between July and September. However, it’s concerning that days sales outstanding were 50 at the end of September 2022, compared to 39 days a year earlier.

Hudson Global

Since the beginning of 2019, Hudson Global has reduced its share count by 13% thanks to share buybacks, but there was less than $0.6 million remaining on the company’s share repurchase program as of September 2022. That’s one catalyst for the share price that is likely to play a smaller role in the future. And with net income shrinking, the company can’t take much advantage of its $340 million net operating loss (NOL) carry forward in the USA.

Investor takeaway

Hudson Global was among the companies that benefited from a tight labor market following the end of COVID-19 lockdowns across the world. However, the company is now facing several headwinds and things could get worse in 2023 if we get a long global recession. I was wrong that the acquisition of Hunt & Badge would provide a boost for Q3 revenues as its contribution was just $18,000.

The balance sheet of Hudson Global is strong, but it seems that the slowdown in hiring activity in the technology sector is likely to last at least several more months. And with little remaining under the share repurchase program, there don’t seem to be any significant catalysts for the share price. I think that it could be best for risk-averse investors to avoid this stock.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment