Justin Sullivan

Homebuilder Hovnanian Enterprises, Inc. (NYSE:HOV) reported a decent earnings call for its fourth fiscal quarter of 2022, but with the seasonably slow period upon it and interest rate and mortgage rates expected to increase as it heads into its historically stronger period of seasonal sales, the coming year should be a tough one for the company.

The industry is already in a bear market and it looks like it’s going to get worse before it gets better. The question that has yet to be answered is concerning how long in duration will the downturn last, and how deep it’ll go.

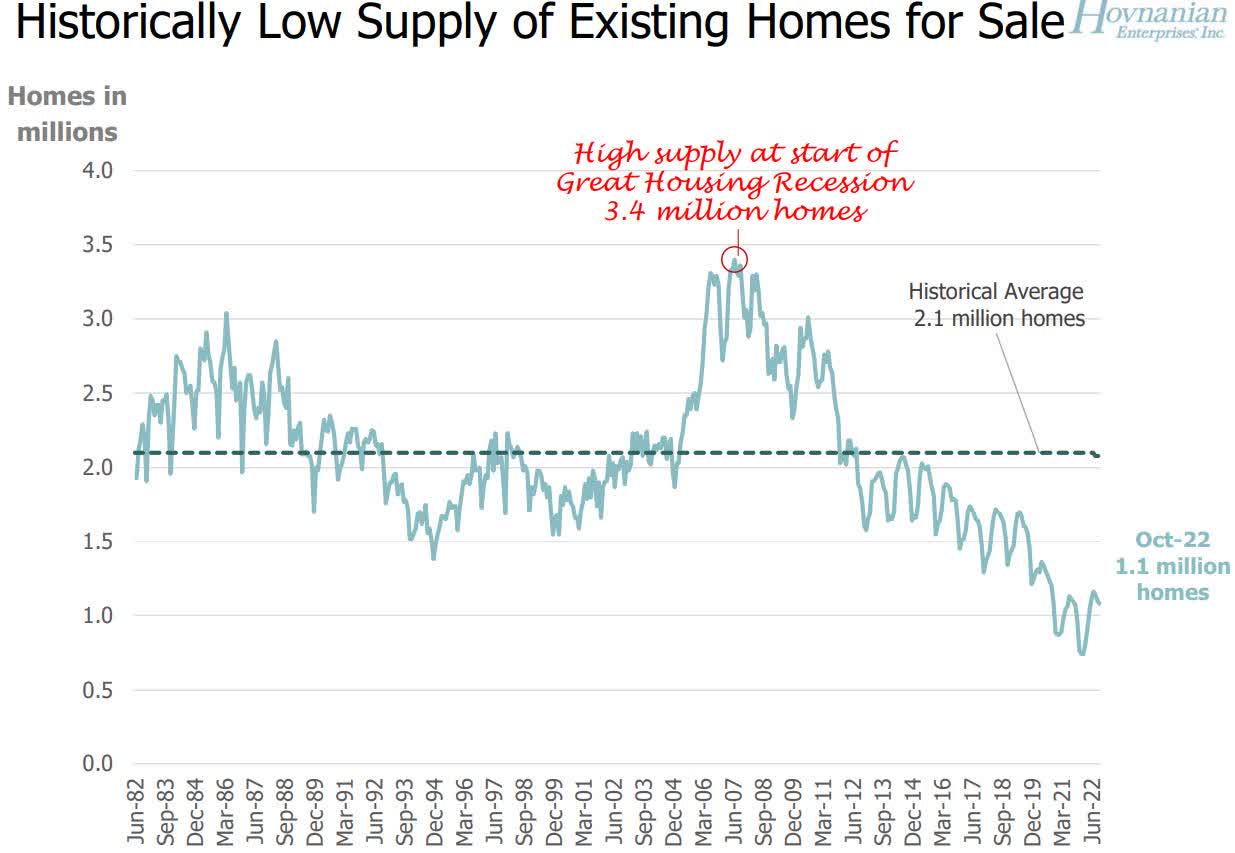

HOV management believes with the far lower number of homes for sale as measured against the Great Recession, that its impact on the homebuilding industry will not as pronounced as before.

Investor Presentation

In this article, we’ll look at why the last earnings numbers will be the best for a while, and the various factors associated with the homebuilding industry and HOV that will impact the company’s performance over the next year or so.

Some of the numbers

As mentioned above, I think the numbers from the last earnings report will be tough to match in 2023, as too many headwinds will overwhelm the homebuilding market in the next year, and possibly longer. With that in mind, the numbers below are highly unlikely to be repeated until the Federal Reserve stops raising interest rates, the economy turns around, and potential homebuyers feel comfortable enough with their financial situations to get back into the market.

Revenue in the fourth fiscal quarter was $887 million, up $73 million from the $814 million in revenue generated in the fourth fiscal quarter of 2021. Full-year revenue for fiscal 2022 was $2.92 billion, compared to $2.78 billion in fiscal 2021.

Adjusted gross margin in the quarter was $24.2 percent, up from the 22.8 percent in gross margin from last year in the same reporting period.

Adjusted EBITDA in the quarter was $144 million, up $23 million from the $121 million in adjusted EBITDA generated in the fourth fiscal quarter of 2021.

Net income in the reporting period was $56 million or $7.24 per share, compared to the $52.5 million in net income or $7.41 per share from the fourth fiscal quarter of 2021.

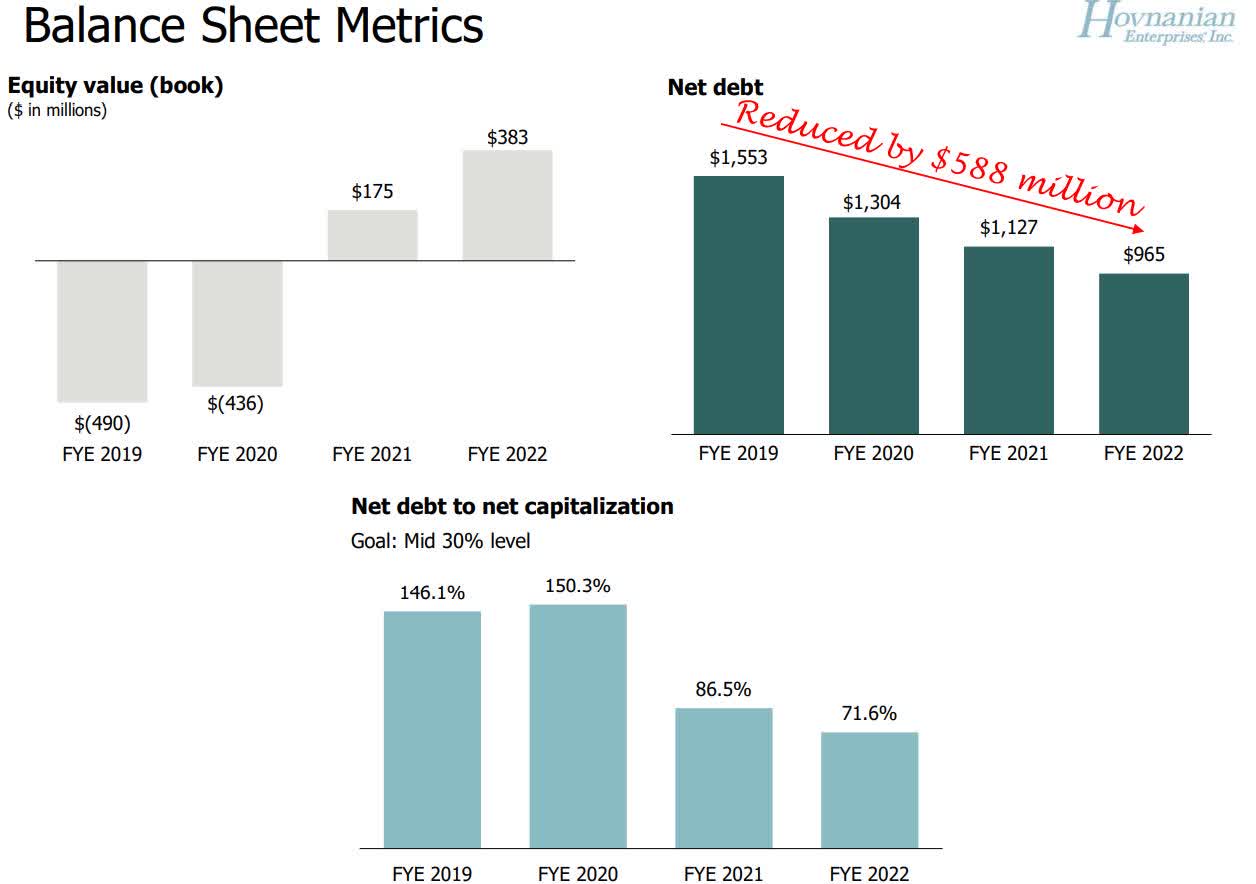

The company held cash and cash equivalents of $326 million, with total debt of $1.29 billion.

Investor Presentation

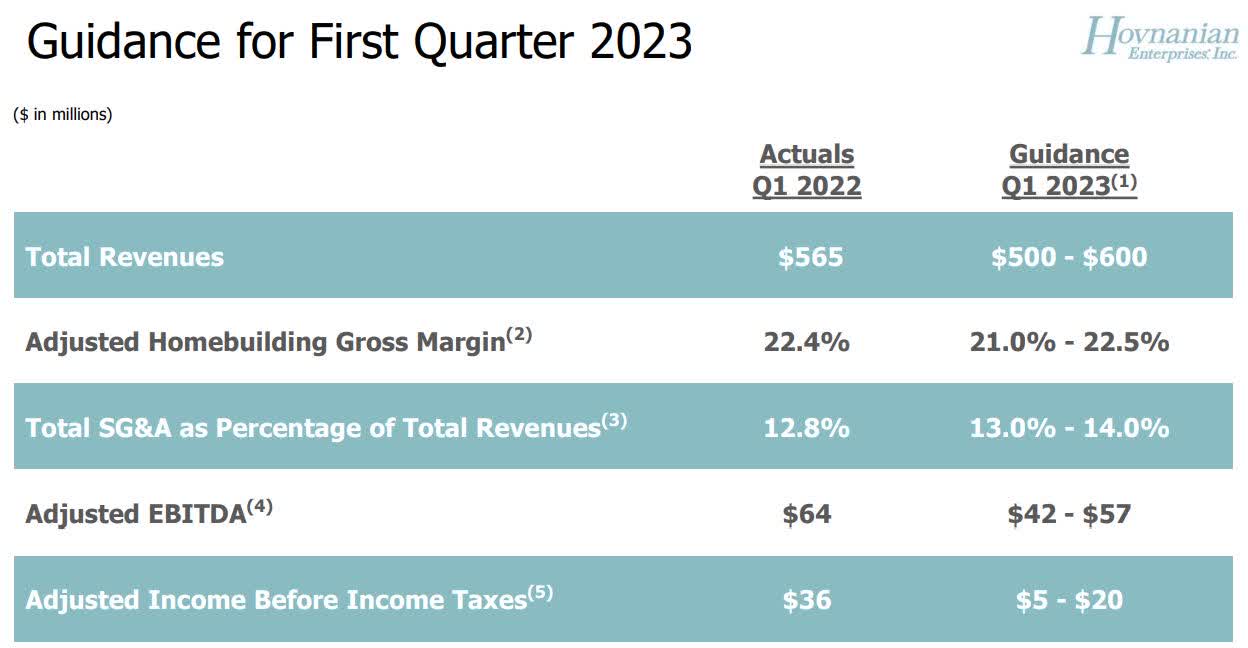

For the first fiscal quarter of 2023, the company guides for revenue to be in a range of $500 million to $600 million; gross margin of 21 percent to 22.5 percent; adjusted EBITDA of $42 million to $57 million; and SG&A as percentage of total revenues to be from 13 percent to 14 percent.

Investor Presentation

Headwinds

The share price of HOV has plunged by approximately $100 per share from the $145 per share it was trading at on May 31, 2021, to a little over $45 per share as I write. This was, of course, foreseen by the market because of the decision by the Federal Reserve to battle rising inflation by increasing interest rates, which in turn brought about much higher mortgage rates.

TradingView

Another headwind is the concern the recession will get worse before getting better in 2023, which has caused many potential homebuyers to hold off on committing to buy a home until they have more certainty concerning the labor market, as many businesses are lowering headcounts.

Not only have these been headwinds for some time concerning the homebuilder industry, but they are now getting worse, as the Federal Reserve will continue to raise rates, which means mortgage rates will rise in conjunction with the pace of interest rate increases.

In the Great Recession, the impact on the housing market was catastrophic, primarily because of the 3.4 million existing homes for sale at that time. HOV management believes it’s not going to have near the impact this time around because the number of homes for sale at this time is at a much more modest 1.1 million.

That said, it depends upon whether or not some of its competitors increase the number of homes for sale and at what level if they do. There has been a slight uptick in new homes for sale recently, but not enough, in my opinion, to make an already challenging situation worse.

HOV thinks the pain could be deep over the next year, but is probably not going to be as long as in the Great Recession.

With the major headwinds getting worse heading into 2023, HOV is being forced to respond to the conditions and is taking steps to mitigate the risk as best it can.

The company’s strategy for 2023

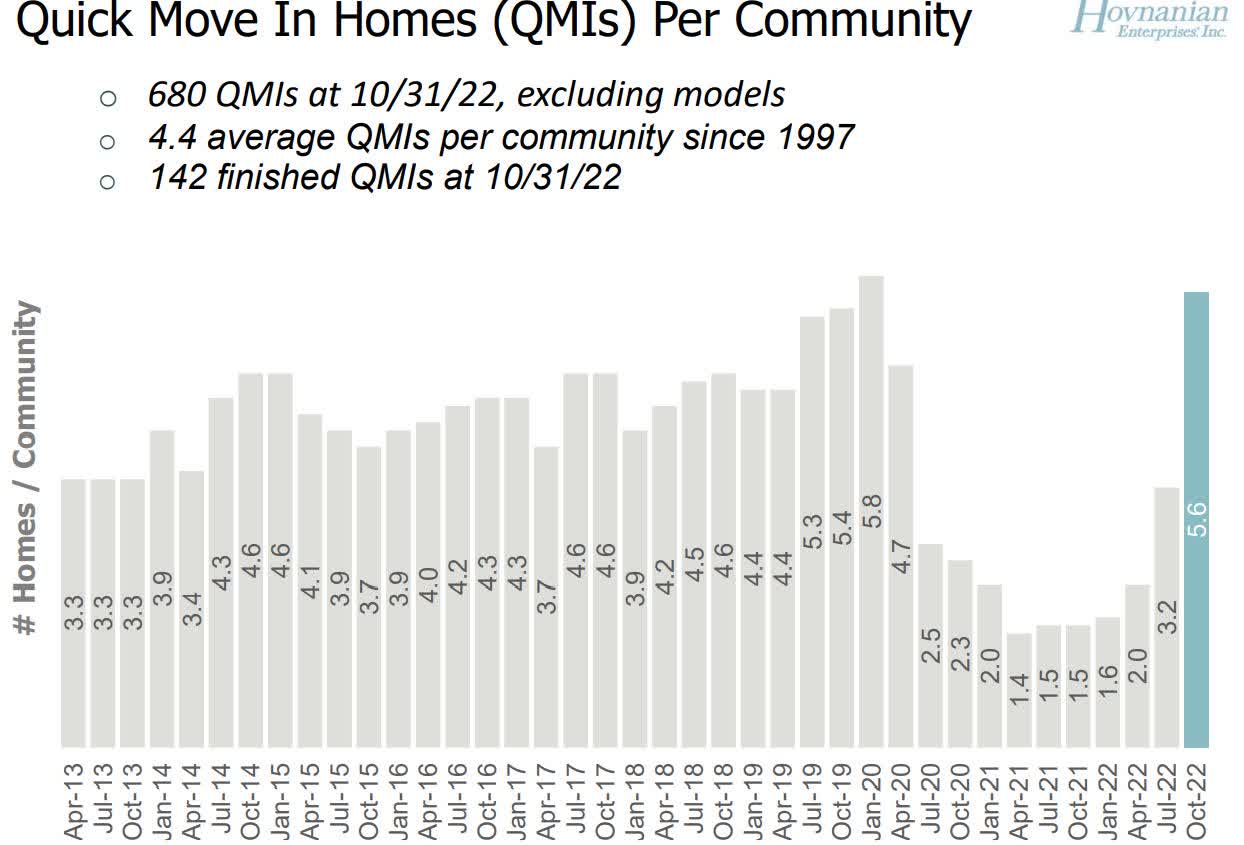

One of several responses of the company to the slowing housing market is to focus on selling quick move in homes (QMI) homes. The reason for that is it allows potential buyers to have more certainty concerning what the mortgage payment at the time of closing will be. As result of this pivot, the number of QMIs per community have risen from an average of 3.2 in the third fiscal quarter to 5.6 and the end of the fourth fiscal quarter. The percentage of sales from QMIs are now at 60 percent of total weekly sales, against the 40 percent in weekly sales QMIs have historically been at. The company has a goal of increasing the total QMIs per community to 7 on a temporary basis until macro-economic conditions improve. Management said this about the strategy:

Once that level is achieved, we will match our start schedules with our 2023 spring selling season pace. This approach will ensure that we do not start an excessive level of unsold homes. Furthermore, we’ll focus on selling these homes before completion.

Investor Presentation

After the completion of the fourth quarter the company got more aggressive in offering a variety of incentives or concessions customized for the different needs of its customers. This is not only being applied to new customers, but to customers already in its backlog in order to them to close on the deal.

Among the incentives are paying for below market mortgage rates, discounting the prices of some of the QMI homes for sale, paying closing costs, and offering other types of options and discounts to potential buyers. Consequently, incentives in the new contracts offered by the company are up from 3 percent in the first half of 2022 to approximately 9.5 percent as of early December 2022. With the incentives and concessions offered by the company, it maintains it should be able to maintain decent margins in the low 20 percent range.

There are a couple of reasons for that. One is because it’s selling more homes in the Northeast and Southeast, where sales prices and margins are stronger than in the West, where sales prices and margins aren’t as strong.

Along with that, a drop in lower prices has provided a more favorable margin environment for HOV.

It is also in negotiations with its suppliers and partners to help share in rising inflation by working with them to reduce costs, which should be a positive catalyst in relationship to margin support in 2023. Last, about 72 percent of the 31.5 thousand of the lots it owns or is under its control are put under contract before the end of October 2021, and 39 percent of lots were controlled before October 2020. The significance there is the lots were underwritten at prices lower than in today’s market.

The combination of these factors should help support margin while the company offers incentives and concessions to boost sales in a slower market.

I think this will help the company in 2023, but it depends on the condition of the economy as to what level it will be. It doesn’t help that the Federal Reserve will continue to raise interest rates heading into the strongest spring home selling period of the industry.

That means if new home sales fall more than expected, HOV will have to offer even more incentives to get people to get them to sign a contract. Even the incentives, under that scenario, will probably not be enough to match the company’s guidance. Last, concerning its strategy for next year, is it’s going to focus more on managing short-term debt while preserving liquidity, i.e., take a more defensive posture until the economic headwinds subside.

Conclusion

There’s no getting around it, 2023 is going to be a tough year for Hovnanian Enterprises, Inc., even with the steps it’s taking to reduce the impact on its performance over the next twelve months.

The current quarter may be an okay one based upon year-over-year comparisons, but the first and second quarters of calendar 2023 are the most important seasons for homebuilders, and with rising mortgage rates and increasing concerns over the economy, it’s going to be tough to maintain momentum in the first half of 2023. If the economy gets worse and the Fed raises rates beyond what the market now thinks it will, it’s going to get even tougher for HOV.

The point is there are limitations as to how effective incentives and concessions will be if mortgage rates continue to climb and the job market gets worse, which is a strong probability. Add to that the fact the company has decided to boost advertising spend in order to keep potential customers thinking about buying a new home from them. When combined with inflationary pressures on the company, this could not only result in lower revenue than expected, but also lower earnings, which would hit the company hard because it has strongly proffered the idea it can maintain margin under these current market conditions.

It’s a difficult call with Hovnanian Enterprises, Inc. in regard to how it’s going to perform in 2023 because of the offsetting positives and negatives. However, with the visibility we have today, I think Hovnanian Enterprises is going to struggle over the next year more than management thinks it will. If the economy gets worse, it’s going to continue to do so in 2024 as well.

Even with the big drop in share price over the last 18 months or so, I think under current market conditions Hovnanian Enterprises, Inc. could still be overvalued. More than likely, it’s going to fall further before it finds a bottom.

Be the first to comment