DNY59

Earnings of Horizon Bancorp, Inc. (NASDAQ:HBNC) will most probably continue to increase this year on the back of extraordinary loan growth. Further, the margin will expand slightly as a result of the significant surge in interest rates, which will support the bottom line. Overall, I’m expecting Horizon Bancorp to report earnings of $2.27 per share for 2022, up 14% year-over-year. Compared to my last report on the company, I’ve tweaked upwards my earnings estimate because I’ve revised upwards the loan balance estimate. For 2023, I’m expecting earnings to grow by a further 8% to $2.44 per share. The year-end target price suggests a high upside from the current market price. Therefore, I’m maintaining a buy rating on Horizon Bancorp.

Strong Loan Growth Momentum Likely to Continue

Horizon Bancorp’s loan portfolio surged by 6.2% during the second quarter of 2022, or 24.7% annualized. Thanks to the second quarter’s performance, the loan book is now on track for double-digit loan growth for the year. The management is targeting a 50/50 mix of organic and acquired growth, as mentioned in the earnings presentation. Considering the plans for acquisitions, loan growth can easily reach the mid-teen range.

The management mentioned in the latest conference call that the pipelines for consumer and commercial loans were comparable to the same period last year when the portfolio actually grew by 4% (16% annualized). Therefore, loan growth will most probably remain strong in the third quarter of 2022.

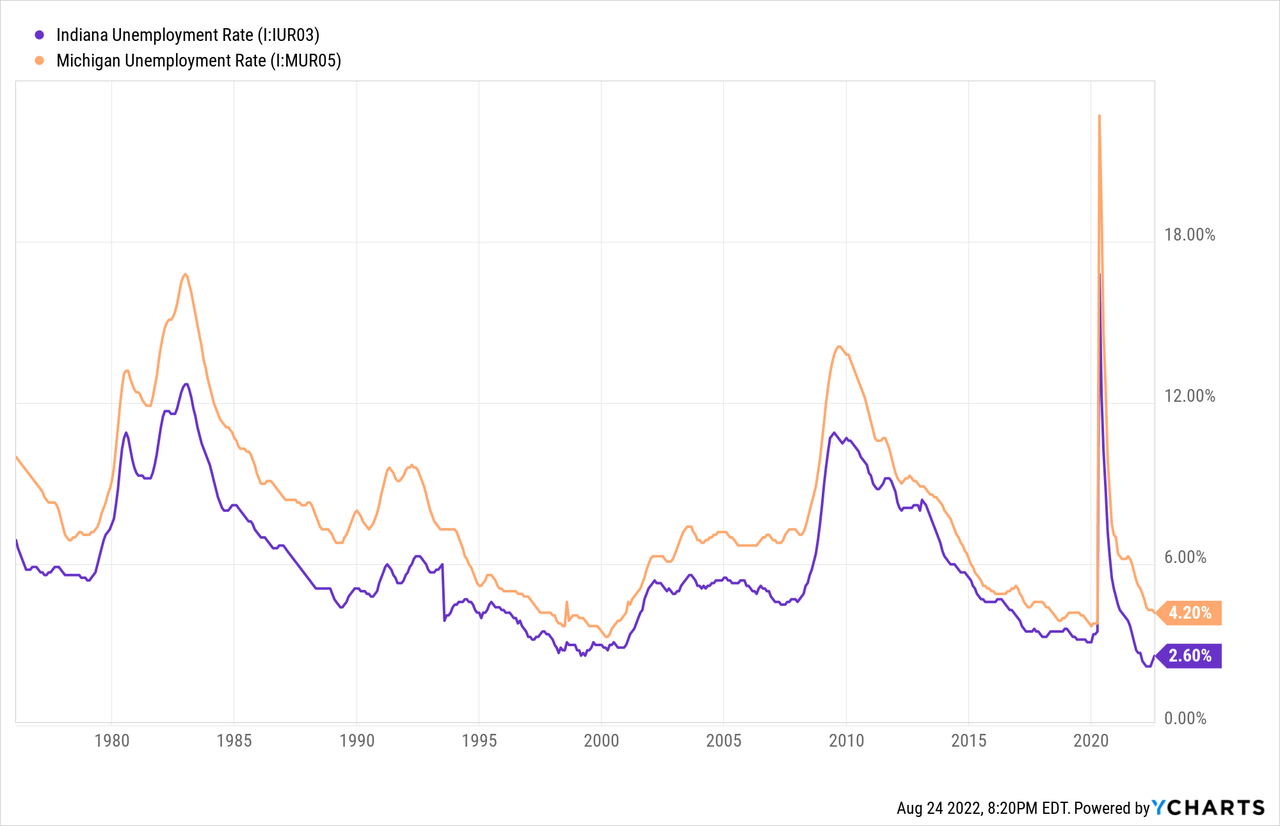

The management especially appeared optimistic about consumer loan demand in the conference call due to low unemployment in Horizon’s markets. Horizon Bancorp mostly operates in Indiana and Michigan. The unemployment rates for both states are currently near the lowest level in decades.

Considering these factors, I’m expecting the loan portfolio to grow by 6% in the second half of 2022, leading to full-year loan growth of 16%. In my last report on Horizon, I estimated loan growth of 9.3% for this year. I’ve revised upwards my loan estimate because of the second quarter’s performance as well as an improvement in the overall outlook. For 2023, I’m expecting loan growth to return to a more normal level of around 8%.

Equity Book Value to Continue to Slip

The large balance of available-for-sale securities on Horizon Bancorp’s books will hurt the equity book value in a rising-rate environment. An increase in interest rates will lower the market value of these securities, which will build up unrealized losses. These losses will bypass the income statement to flow directly into the equity account through other comprehensive income.

The book value per share has already dropped to $15.10 at the end of June 2022 from $15.55 at the end of December 2021, as mentioned in the 10-Q Filing. I’m expecting further erosion of equity book value in the third quarter because of the 75 basis points hike in the Fed funds rate in July. Moreover, I’m expecting a further 75 basis point hike in the remainder of the year.

On the other hand, retained earnings (discussed below) will lift the equity book value. The following table shows my balance sheet estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Financial Position | ||||||||||

| Net Loans | 2,996 | 3,619 | 3,810 | 3,553 | 4,122 | 4,461 | ||||

| Growth of Net Loans | 6.3% | 20.8% | 5.3% | (6.7)% | 16.0% | 8.2% | ||||

| Other Earning Assets | 827 | 1,078 | 1,325 | 2,731 | 3,163 | 3,291 | ||||

| Deposits | 3,139 | 3,931 | 4,531 | 5,803 | 6,082 | 6,455 | ||||

| Borrowings and Sub-Debt | 588 | 606 | 590 | 791 | 1,097 | 1,141 | ||||

| Common equity | 492 | 656 | 692 | 723 | 695 | 772 | ||||

| Book Value Per Share ($) | 12.8 | 15.1 | 15.7 | 16.5 | 15.9 | 17.7 | ||||

| Tangible BVPS ($) | 9.4 | 11.0 | 11.7 | 12.5 | 11.9 | 13.7 | ||||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

||||||||||

Large Securities Portfolio and Balance of Fixed-Rate Loans to Limit Asset Sensitivity

As can be gleaned from the earnings presentation, around 63% of the loan portfolio is based on fixed rates, while only 37% is based on variable rates. Therefore, the loan portfolio’s average yield will have low sensitivity to rate changes this year.

Further, Horizon Bancorp has a large balance of investment securities with fixed rates which will also make the average earning-asset yield upward sticky in a rising rate environment. Available-for-sale securities made up 15% of earning assets and held-to-maturity securities made up 29% of earning assets at the end of June 2022. As mentioned in the earnings presentation, the effective duration of the portfolio is quite long at 6.9 years. Therefore, it can be safely assumed that most of the portfolio will not mature this year. The portfolio carried a yield of only 2.26%; hence, it will continue to drag interest income.

Moreover, interest-bearing deposits, excluding certificates of deposits, made up a sizable 64% of total deposits at the end of June 2022. These deposits will re-price soon after every rate hike and thus keep the deposit beta elevated.

The results of the management’s interest-rate sensitivity analysis given in the presentation showed that a 200-basis points hike in interest rates could boost the net income by only around 6% over twelve months. Please note that this model used a deposit beta of 35%, while the actual deposit beta in the second quarter was just 3%, as mentioned in the conference call. The management successfully kept the sensitivity subdued during the quarter due to time lag. As a result, in my opinion, the deposit beta will get closer to 35% in the second half of this year as deposit costs will catch up to market interest rates.

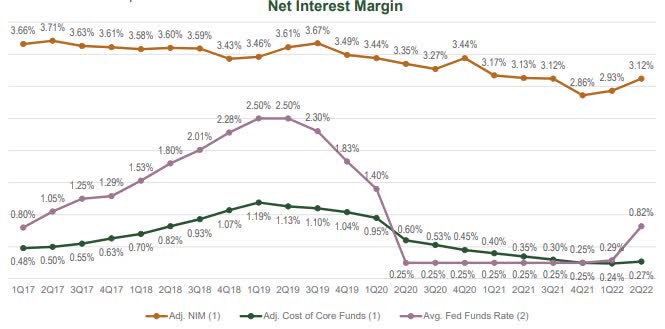

Historically as well, the net interest margin hasn’t been too closely related to interest rate movement.

2Q 2022 Earnings Presentation

Considering these factors, I’m expecting the margin to grow by six basis points in the second half of 2022 and remain unchanged in 2023.

Higher-than-Normal Provision Expense Likely for the Second Half of 2023

Non-performing loans made up 0.51% of total loans, while allowances made up 1.33% of total loans at the end of June 2022. This provisioning cover appears a bit tight considering borrowers are likely to face financial stress soon due to heightened inflation. High interest rates will further add to the misery of those borrowers who are on variable rates. Further, the possibility of a recession will encourage banks to maintain a large buffer for anticipated losses.

Therefore, I’m expecting provisioning to be slightly higher than the historical mean for the second half of 2022. However, due to the large reserve release in the first quarter of 2022, the average provisioning for this year will likely remain below the historical average. For 2023, I’m expecting provisioning to revert to the historical mean.

Expecting Earnings to Grow by 14%

The anticipated surge in the loan book and slight margin expansion will likely drive earnings this year. On the other hand, slightly higher provision expenses will likely restrict earnings growth. Overall, I’m expecting Horizon Bancorp to report earnings of $2.27 per share for 2022, up 14% year-over-year. For 2023, I’m expecting earnings to grow by a further 8% to $2.44 per share. The following table shows my income statement estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Income Statement | ||||||||||

| Net interest income | 135 | 161 | 171 | 182 | 214 | 236 | ||||

| Provision for loan losses | 3 | 2 | 21 | (2) | 1 | 4 | ||||

| Non-interest income | 34 | 43 | 60 | 58 | 52 | 50 | ||||

| Non-interest expense | 103 | 122 | 131 | 139 | 149 | 157 | ||||

| Net income – Common Sh. | 53 | 67 | 68 | 87 | 99 | 107 | ||||

| EPS – Diluted ($) | 1.38 | 1.53 | 1.55 | 1.98 | 2.27 | 2.44 | ||||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

||||||||||

In my last report on Horizon Bancorp, I estimated earnings of $2.15 per share for 2022. I’ve tweaked upwards my earnings estimate mostly because I’ve revised upwards my loan balance estimate.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

High Total Expected Return Warrants a Buy Rating

Given the earnings outlook, I’m expecting Horizon Bancorp to increase its dividend by $0.02 per share in the third quarter of 2022, which will take the full-year dividend to $0.68 per share for 2023. My dividend and earnings estimates suggest a payout ratio of 28%, which is close to the last five-year average of 31%. Further, my dividend estimate suggests a dividend yield of 3.5%.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value Horizon Bancorp. The stock has traded at an average P/TB ratio of 1.60 in the past, as shown below.

| FY17 | FY18 | FY19 | FY20 | FY21 | Average | |

| T. Book Value per Share ($) | 9.3 | 9.4 | 11.0 | 11.7 | 12.5 | |

| Average Market Price ($) | 17.7 | 19.4 | 17.0 | 12.4 | 18.2 | |

| Historical P/TB | 1.90x | 2.07x | 1.54x | 1.06x | 1.46x | 1.60x |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $11.9 gives a target price of $19.1 for the end of 2022. This price target implies a 2.4% downside from the August 24 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.40x | 1.50x | 1.60x | 1.70x | 1.80x |

| TBVPS – Dec 2022 ($) | 11.9 | 11.9 | 11.9 | 11.9 | 11.9 |

| Target Price ($) | 16.7 | 17.9 | 19.1 | 20.3 | 21.5 |

| Market Price ($) | 19.6 | 19.6 | 19.6 | 19.6 | 19.6 |

| Upside/(Downside) | (14.6)% | (8.5)% | (2.4)% | 3.7% | 9.8% |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 12.2x in the past, as shown below.

| FY17 | FY18 | FY19 | FY20 | FY21 | Average | |

| Earnings per Share ($) | 0.95 | 1.38 | 1.53 | 1.55 | 1.98 | |

| Average Market Price ($) | 17.7 | 19.4 | 17.0 | 12.4 | 18.2 | |

| Historical P/E | 18.6x | 14.1x | 11.1x | 8.0x | 9.2x | 12.2x |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $2.27 gives a target price of $27.7 for the end of 2022. This price target implies a 41.1% upside from the August 24 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 10.2x | 11.2x | 12.2x | 13.2x | 14.2x |

| EPS 2022 ($) | 2.27 | 2.27 | 2.27 | 2.27 | 2.27 |

| Target Price ($) | 23.1 | 25.4 | 27.7 | 29.9 | 32.2 |

| Market Price ($) | 19.6 | 19.6 | 19.6 | 19.6 | 19.6 |

| Upside/(Downside) | 18.0% | 29.6% | 41.1% | 52.7% | 64.3% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $23.4, which implies a 19.4% upside from the current market price. Adding the forward dividend yield gives a total expected return of 22.8%. Hence, I’m maintaining a buy rating on Horizon Bancorp.

Be the first to comment