Dilok Klaisataporn

Earnings season can be a good opportunity to pick up quality names, as market jitters can lead to discounts on stocks one has been eyeing. This includes Honeywell International (NASDAQ:HON), which as shown below, has sold off by nearly 10% over the past couple of weeks, due perhaps to market fears of less than impressive earnings. In this article, I highlight why total return focused investors may want to considering layering into HON on the drop, so let’s get started.

HON Stock (Seeking Alpha)

Why HON?

Honeywell is a global technology company that has roots dating back to 1885, when it developed a predecessor to today’s thermostat. Today, it operates in multiple industries with strong market share in aerospace, building technologies, performance materials, and safety and productivity solutions. HON has a strong reputation for innovation, providing competitive advantages for its diverse portfolio of products.

In recent years, Honeywell has been investing in innovative technologies that put it in the forefront of process efficiencies for its customers. This includes many of its offerings being aligned to energy efficiency and decarbonization. This includes HON’s Automated Storage and Retrieval System, which leverages AI to allow warehouse operators to better keep up with high ecommerce growth, as well as building automation systems that help owners to better monitor and control energy usage.

Meanwhile, HON has demonstrated strong growth, especially in light of macroeconomic uncertainties. This is reflected by robust organic sales growth of 9% YoY during the third quarter, and 10% organic sales growth when excluding the wind down of operations in Russia. This was driven by impressive double-digit growth in building technologies, performance materials, and aerospace.

Looking forward, I see reasons to be optimistic, as management highlighted that its order backlog remains at all-time highs as of the end of November, providing impetus for volume growth as supply chains concerns continue to ease. During the same Credit Suisse (CS) Global Industrials Conference, management also reiterated strong Q4 guidance, with the expectation of 11.5% organic sales growth at the midpoint.

Also encouraging, management expects strong operating leverage in Q4, with operating margin expected to improve by 160 basis points at the midpoint and expected adjusted EPS growth of 20% and 8.5% YoY for Q4 and full year 2022, respectively.

Longer term, HON is set to benefit for continued need for supply chain automation, as many companies have realized the critical need for resilient supply chains over the past 3 years amidst disruptions and due to increasing demand from e-commerce. Plus, many of Honeywell’s automation solutions offer a meaningful return on investment with a short payback period. Plus, Morningstar believes HON’s growth is set to see meaningful growth in the coming years as noted in its recent analyst report:

We believe Honeywell is capable of meeting our assumed targets through a combination of portfolio refreshes, powerful new product introductions, breakthrough initiatives, and strategic partnerships in areas where the firm has domain expertise, a focus on high-growth regions that’ll help the firm grow faster than its core markets, continuous improvement initiatives centered on fixed cost reduction, on-time delivery and simplified design, supply chain automation, and an increasing shift toward software with a recurring revenue stream. In our view, Honeywell was wise to continue investing aggressively during the height of the pandemic, which we think will reward the firm with share gains.

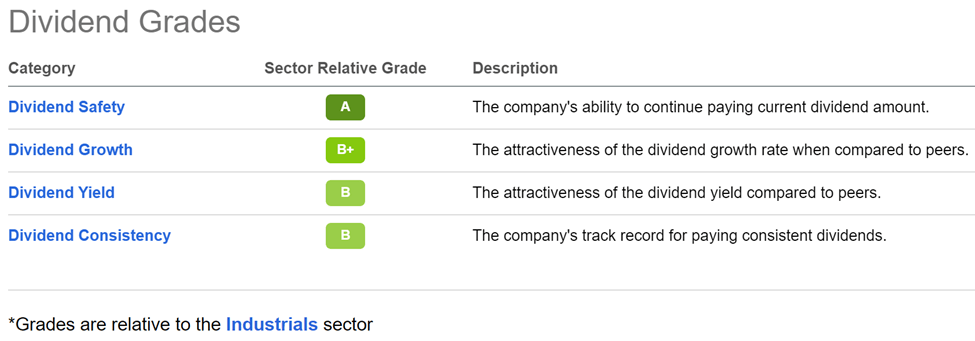

Importantly, Honeywell maintains a strong A rated balance sheet. While its 2% dividend yield isn’t particularly high, it’s well supported by a 47% payout ratio and comes with a 5-year dividend CAGR of 6.4%. As shown below, HON scores A and B grades for dividend safety, growth, yield, and consistency.

HON Dividend Grades (Seeking Alpha)

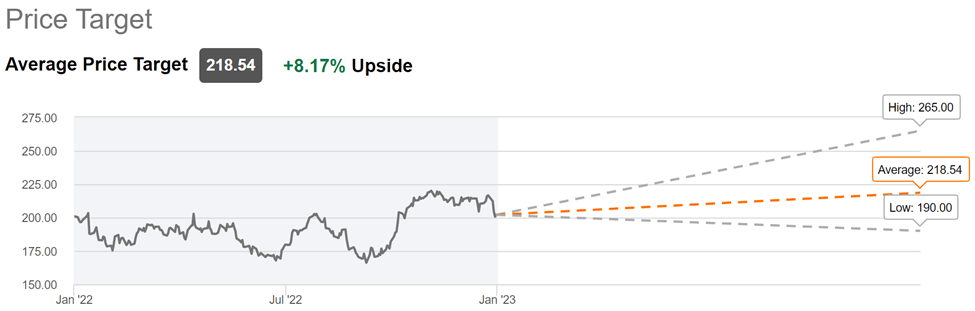

Admittedly, HON isn’t cheap at the current price of $202 with a forward PE of 23.4. However, I believe the valuation is reasonable considering the moat-worthy nature of the enterprise and the 12% EPS growth that analysts expect next year. Morningstar has a $226 fair value estimate, and analysts have a consensus Buy rating with an average price target of $219.

HON Price Target (Seeking Alpha)

Investor Takeaway

Honeywell is a moat-worthy industrial giant with strong operating fundamentals. It’s set to benefit from increased need for automation as businesses seek more resilient and efficient supply chains. It’s also focusing on areas such as energy efficiency and decarbonization, which are becoming increasingly important to corporate sustainability efforts. Despite its slightly elevated valuation, I believe HON is a solid long-term investment for potentially strong total returns.

Be the first to comment