jetcityimage/iStock Editorial via Getty Images

Honda Motor Co., Ltd. (NYSE:HMC) is one of the world’s leading automakers; the average American is familiar with its brands and encounters the company’s products on a daily basis. Honda has a reputation for delivering excellent value at a cheap price, and that’s exactly what the company’s stock offers value-conscious investors. Consistently profitable and trading at <6x trailing FCF, Honda’s stock is deeply undervalued compared to its fundamentals and compared to its competitors in the auto industry. The company further trades at a discount to tangible book value, meaning that tomorrow’s profits are a freebie for today’s investors.

Operations

Honda Motor Co. is a globally recognized Japanese automaker. Its automobiles are known for their reliability, affordability, value retention, and safety, affording the company tremendous brand value and public goodwill. Honda was founded in 1948 as a manufacturer of auxiliary engines for bicycles, but quickly pivoted to producing motorcycles. Honda has been the largest global producer of motorcycles since 1959, the same year it expanded into North America. In 1963, Honda made its first foray into the car market with the manufacture of the T360 mini-truck. The company has since grown into one of the top 10 automakers in the world by revenue and unit sales. In addition to its core Honda brand, the company has also operated the Acura luxury brand since 1986.

Substantially all of Honda’s revenue is derived from the sale of automobiles and motorcycles, with the remainder attributable to power products, small-boat motors, light planes, and aircraft engines. Honda’s two main markets are Asia, where it predominantly sells motorcycles and generates a majority of its revenue, and North America, consisting mostly of car sales and accounting for about a third of the business.

While many automakers have taken decisive (and expensive) steps to pivot to full electrification of their vehicles, Honda’s moves have been more measured. Rather than focusing on the production of battery-electric vehicles (BEVs), the company has instead transitioned into one of the world’s foremost producers of hybrid vehicles utilizing hydrogen technology (fuel-cell electric vehicles, or FCEVs). In 2023, Honda sold over 1,000,000 hybrid vehicles globally and the Honda CR-V hybrid was the best-selling hybrid model in the United States. While there are many naysayers vocally critical of the company’s electrification approach, the hybrid-dominated strategy is unquestionably demonstrating success at the present juncture. The jury is still out on the long-term outlook for Honda’s EV plans, with the company rolling out its first mass-market fully electric vehicles in North America (the Honda Prologue and Acura ZDX) in 2024. Management is targeting 100% electrified vehicle sales by 2040, though some critics feel this target date should be earlier.

Honda is also working on automation technology in the form of both driver-assistance features and self-driving vehicles. Honda received approval of its Level 3 automated driving technology from Japanese authorities in 2020, the same year that it was first allowed. Several months later, Honda began leasing a version of its Honda Legend EX equipped with “Honda SENSING Elite,” the company’s Level 3 automated driving software, in Japan. Vehicles with Honda SENSING Elite are capable of driving themselves, with the caveats that the tech can only be relied upon in low-speed traffic and that a driver must be available to take control if needed – similar to the most advanced self-driving technologies currently approved for the consumer market anywhere in the world.

While the introduction of Honda SENSING Elite to the North American and European markets appears to be a ways off, the company has developed the technological prowess to make this a reality at the appropriate time. Honda continues to develop its autonomous driving capabilities, announcing in October 2023 that it was entering into a joint venture with General Motors’ AV subsidiary Cruise (in which Honda became an investor in 2018) to put driverless taxis on the streets of Tokyo starting in 2026.

Performance

Honda’s high-water mark of the recent past was FY2018 (ended March ’18), with total revenue of $145B and net income of $10B. Revenue fell off to $119B by FY2021 and $120B in FY2022, and net income dropped to a low of $4.9B in FY2023. In calendar year 2023, revenue was $137B and net income was $6.7B. U.S. sales were up 33% YOY from a low base in 2022, which management had attributed to industry-wide supply chain and logistics issues. The company forecasts 10-15% American sales growth in 2024 and recently reported North American sales of over 110,000 units in February, a 32% YOY increase (following 10.3% annual growth in January).

Honda’s hybrid business is leading the charge in North America, with hybrid sales growing more than threefold in 2023. Contrary to the expectations of the bearish pundits who predicted that Honda’s focus on fuel-cell technology would leave the company lagging behind its BEV-focused peers, at present Honda’s focus on hybrids is sparing the company from the unprofitable race to the bottom occurring in the EV industry. To this point, Ford recently announced that it is scaling back its EV plans and increasing its production of hybrids – and General Motors is expected to potentially make similar moves. As mentioned, Honda is rolling out its first BEVs this year, but its cautious and deliberate approach has insulated the company from current headwinds in the EV sector. While the long-term wisdom of the hybrid-driven strategy is still subject to doubt, the ongoing boom of hybrid adoption and BEV price wars position Honda very favorably as compared to many industry peers.

EV Strategy

Honda’s overarching EV strategy is to take its time steadily building a fully-electric BEV lineup, while relying much more heavily on FCEV hybrids in the medium term. In North America, the company aims to achieve 80% electrified sales (including both BEVs and hybrids) by 2035 and 100% by 2040. It thus follows that Honda expects some demand for new internal combustion engine ((ICE)) cars to persist until 2040 and demand for FCEVs to persist beyond then. Some observers view this timeline as naively prolonged, though the current market environment (in which BEV production is stalling and FCEV production accelerating) seems to be vindicating Honda’s strategy – for now, at least.

Valuation

The Honda value thesis is as simple as they come. The automaker is highly profitable and growing, trades at a significant discount to tangible book value, features low earnings multiples, and comes attached to one of the world’s most powerful brands.

Discount to Book Value

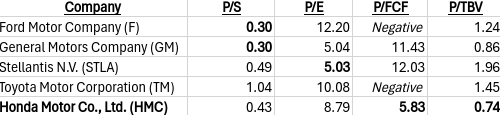

The most eyebrow-raising aspect of Honda’s market valuation is that it is comfortably exceeded by the company’s tangible book value. Honda features a TBV of $78.9B, with assets including $31.7B in cash, $52.6B of outstanding auto loans funded by the company’s vehicle financing division, $16.6B in inventory, $21.7B of net PPE, and $14.3B in long-term investments. The company’s market cap is $58.5B, awarding the company a stunning P/TBV ratio of 0.74. With the stock trading at a significant discount to the business’s tangible liquidation value, it’s difficult to envision a realistic negative outcome for long-term investors who buy at present prices.

Brand Value

Moreover, Honda’s TBV does not even account for the tremendous intellectual property value associated with the Honda brand. According to Brand Finance’s 2024 Global 500 brand rankings, Honda is the 74th most valuable global brand with a brand value of $25.9B. In combination with the $20.4B of tangible book value unaccounted for by the company’s market cap, Honda’s estimated brand value pushes the discount to book value into the $45B+ range.

Price Multiples

Honda trades at a P/S ratio of 0.43, P/E ratio of 8.79, and a P/FCF ratio of just 5.83. These ratios would border on ludicrous even if Honda’s book value were slashed in half; they are all the more astonishing considering that net assets already vastly exceed the market cap. Even within the low-multiple (traditional) auto industry, Honda stands out for its steep discount to TBV and extraordinary free cash flow yield.

Author’s Calculations (Based On TTM Financials)

Future Profits Are Free

Honda is consistently profitable and FCF-positive, and there is little reason to believe that’s about to change. With the company trading below its net asset value, Honda’s current and future profits are a free windfall for investors. With its trailing FCF equating to a free cash flow yield of 17.48%, Honda’s stock is cheap any way you look at it. Barring the unlikely event that Honda manages to lose tens of billions of dollars of shareholder equity in the years ahead, there is little way for long-term investors to lose.

Buybacks & Dividends

In late 2017, Honda began buying back its shares on the open market. Between November 2017 and April 2023, the company spent over $3B on share repurchases, reducing its share count by ~143M. (Following a 3-for-1 stock split of the Tokyo shares in 2023, this equates to ~429M ordinary shares.) In February of this year, the company announced a new 50 billion yen ($330 million) buyback program to repurchase up to 34M ordinary shares (11.3M ADRs) through April 30, 2024. Last week, the company reported that it had repurchased ~20.9M ordinary shares under the new authorization for ~37.5B yen. Honda’s (extremely value-accretive) buybacks have resulted in a ~9% reduction in its share count since 2017.

Additionally, Honda has paid a regular dividend for decades. The company currently makes dividend distributions semi-annually and aims for a payout ratio of ~30%, a conservative figure that leaves the company on extremely stable financial footing. Despite the low payout ratio, the company features a respectable dividend yield of ~3%.

Risks

Acceleration of BEV Adoption

One of the most oft-articulated criticisms of Honda is that its focus on FCEVs dooms it to eventual obsolescence as BEVs increasingly penetrate the new car market. Just a few months ago, it was a lot easier to argue that Honda was hopelessly behind the times, investing in FCEV development and production at a time when much of the industry was skipping ahead to BEVs. Now, with BEV prices falling and automakers cutting back on their BEV production plans, Honda’s approach looks a lot wiser.

For all the flak Honda has received over its slow transition to BEVs, the hybrid strategy is thus far paying significant dividends during a period which management describes as a time of “evolution” from ICE vehicles to fully electric BEVs. Per management, “already, it’s a 50-50 sort of a split between the ICE petrol-based cars and hybrids.” As mentioned, Honda’s North American hybrid sales tripled in 2023. Whatever the critics may say about the long-term wisdom of the company’s approach, it is currently working.

There is undoubtedly some risk that ICE sales could be phased out sooner than 2040. There is further risk that hybrids may not be an important part of the new car sales mix 10-15 years from now. Either of those outcomes would be contrary to Honda’s present expectations, potentially leaving the company flat-footed in the face of industry disruption, as the bears anticipate. Even in the worst-case scenario where BEV adoption accelerates too fast for Honda to keep up with (which, to reiterate, looks a lot less likely today than it did in the recent past), the company’s balance sheet provides an important margin of safety from which investors could recoup their invested capital plus a decent return.

Recalls

Unfortunately, recalls have been a persistent occurrence for Honda vehicles over the past couple of years. In December 2023, Honda recalled 4.5 million vehicles globally due to a fuel pump issue, following a number of more minor recalls throughout the year. All told, Honda was the most-recalled brand in the U.S. in 2023, narrowly beating out Ford for the dubious distinction. In February of this year, Honda recalled a further 750,000 vehicles due to an airbag deployment issue originating with one of its suppliers.

These recalls present the risk that Honda’s reputation for safety and reliability may be under threat. That said, the company’s extreme 2023 recall numbers were an historical aberration which is not likely to soon be repeated. Consumers understand that occasional recalls are par for the course in the automotive industry, and that the statistical likelihood of being personally affected by any of these production flaws is quite low. Assuming that Honda does not continue to exhibit an outsized recall footprint as it did last year, I expect these issues to have no substantial impact on the company’s long-term performance or reputation.

Japanese Stagnancy

I suspect many investors may share my general hesitancy to invest in Japanese firms. While the Nikkei 225 (at long last) recently surpassed the highs it last set 35 years ago, the country’s economy has famously been stagnant for decades, with little economic growth and steadily increasing central bank intervention to prop up the economy. The Bank of Japan is widely considered the most activist central bank in the world, currently owning about 7% of the Japanese stock market. As a skeptic of (the centralized application of) Keynesian economics, I view Japan’s long-term economic stagnation as the inevitable bedfellow of its authorities’ aggressive market intervention – feeding a destructive “the chicken or the egg” cycle whereby any sign of economic weakness precipitates further central bank intervention, further weakening the long-term fundamentals of the nation’s economy.

As a Japanese company, Honda could be adversely affected by the economic stagnancy of its home market, especially if and when the country’s artificially loose monetary policies eventually blow up in the face of its policymakers. It must be noted, however, that Honda generates the vast majority of its revenues abroad and has little need for outside financing. Accordingly, it is mostly insulated from the potential negative effects of its home country’s long-term stagnation.

Conclusion

Honda is a rather boring company selling a century-old product, which likely contributes to the lack of investor enthusiasm surrounding its stock. The company has caught criticism for its slow pace of EV development and its present focus on hybrids, but to date, the available evidence indicates that Honda’s strategy is far more astute than the predictions of its critics. In the interim, Honda is cautiously rolling out its first BEVs this year and is quietly developing autonomous capabilities to drive its future success.

Even if the company’s growth initiatives fail spectacularly and Honda goes the way of the horse-and-buggy once ICE and hybrid vehicles disappear from dealer lots, investors are still protected by $20B in unencumbered tangible assets in addition to Honda’s tremendous brand value. As of now, the company continues to churn out massive profits and cash flows year after year. If we apply Occam’s Razor and assume that Honda is not about to start losing billions annually for the duration of its life cycle, the stock is an obvious buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment