tortoon

Introduction

When last discussing Holly Energy Partners (NYSE:HEP), there had been a number of their Master Limited Partnership peers acquired by parent companies but as my previous article discussed, there was no takeover coming but more excitingly, management flagged higher distributions. After another quarter of improving cash flow performance and new supportive capital expenditure guidance for 2023, it now appears the scene is set for higher distributions as we enter this new year.

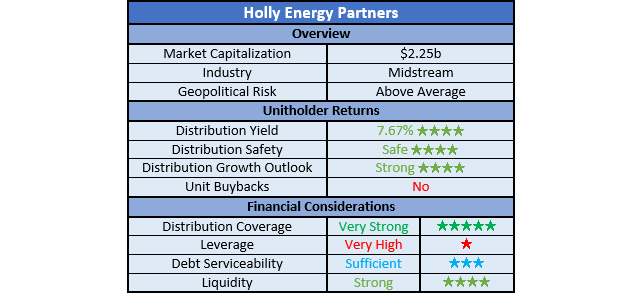

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

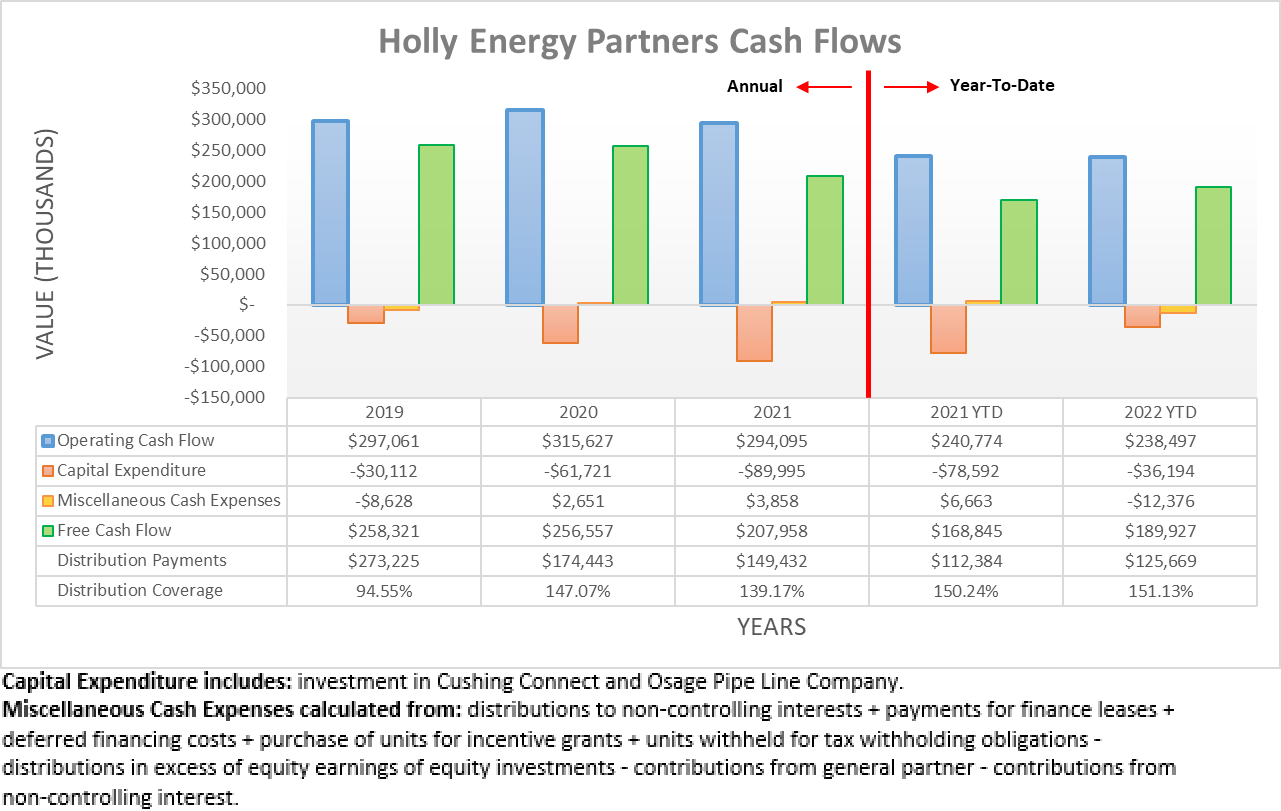

Due to higher turnaround expenditure, their cash flow performance saw a lackluster start to 2022 with their operating cash flow down circa 6% year-on-year during the first half, as my previous analysis discussed. Thankfully, this is now largely in the past and thus following the third quarter, their operating cash flow recovered most of the lost ground with their result for the first nine months landing at $238.5m, thereby almost matching their previous result of $240.8m for the first nine months of 2021.

Author

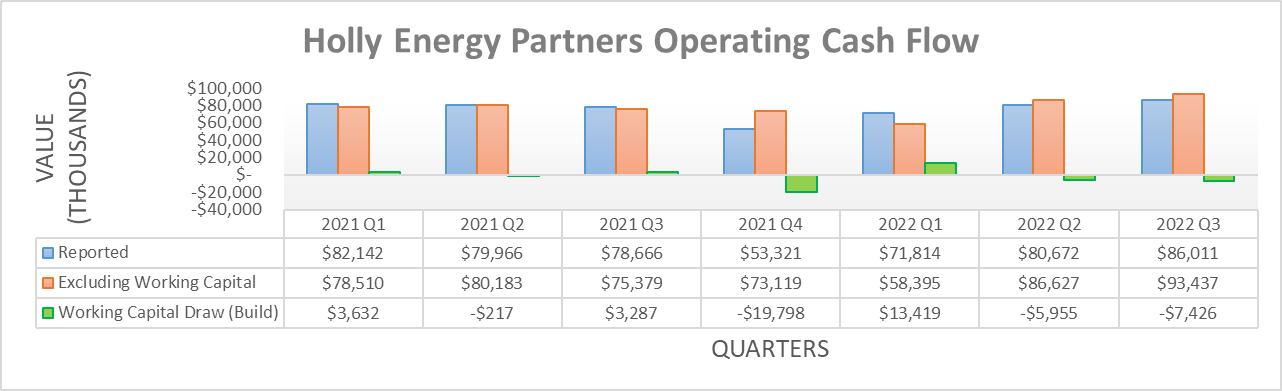

When zooming into a quarterly basis, their improving cash flow performance is more easily visible with their results for the third quarter higher across the board at both the reported and underlying levels. In the case of the former, the second quarter of 2022 already saw improvements flowing from their Sinclair acquisition with a result of $80.7m, although the third quarter saw their operating cash flow climb even further to $86m. Whereas in the case of the latter, if excluding their working capital movements, their underlying operating cash flow sees these two results at $86.6m and $93.4m respectively, thereby also making improvements.

Even though their distribution coverage was already a strong 151.13% across the first nine months of 2022, it actually stands to climb even higher during 2023. In part, this is due to the benefits of their Sinclair acquisition that were absent earlier in 2022 and lower turnaround expenditure, which means there is plenty more upside potential for their operating cash flow and thus, free cash flow. If annualizing their underlying operating cash flow of $93.4m from the third quarter, it equals $373.6m and thus would see a far higher annual result than any previous year, such as their result of $315.6m during 2020 that presently stands as their high-water mark.

Concurrently, their already low capital expenditure is also forecast to decrease even further during 2023, given their guidance for only $37.5m at the midpoint. Since the first nine months of 2022 already saw $36.2m of capital expenditure, which annualizes to $48.3m, this indicates they are winding down investments, which in turn, maximizes the free cash flow they generate from their Sinclair acquisition. If wrapped together with the aforementioned estimated operating cash flow, it places their estimated free cash flow at circa $335m during 2023, give or take a little depending upon working capital movements and future turnaround expenditure.

As it stands right now, their quarterly distributions of $0.35 per unit cost $177m per annum, given their latest outstanding unit count of 126,440,201. If my estimated free cash flow for 2023 comes to pass, which I presently see no reason to doubt, this would result in very strong distribution coverage of almost 200%. This marks a sizeable improvement over 2022 and naturally, it raises the prospects of finally seeing higher distributions, something they placed on the horizon when conducting the previous analysis following the second quarter, as per the commentary from management included below.

“Looking to ’23 to your question about distribution growth, at this point, I think we would urge to increasing the distribution itself. We will evaluate buybacks, as you know, HEP is not the most liquid stock. So it’s not necessarily that we want to reduce the float, it may not be in the best interest of HEP, but if that’s a better option we will go ahead and do it, but right now, I’d say it’s going to take the form of distribution increases.”

-Holly Energy Partners Q2 2022 Conference Call.

Author

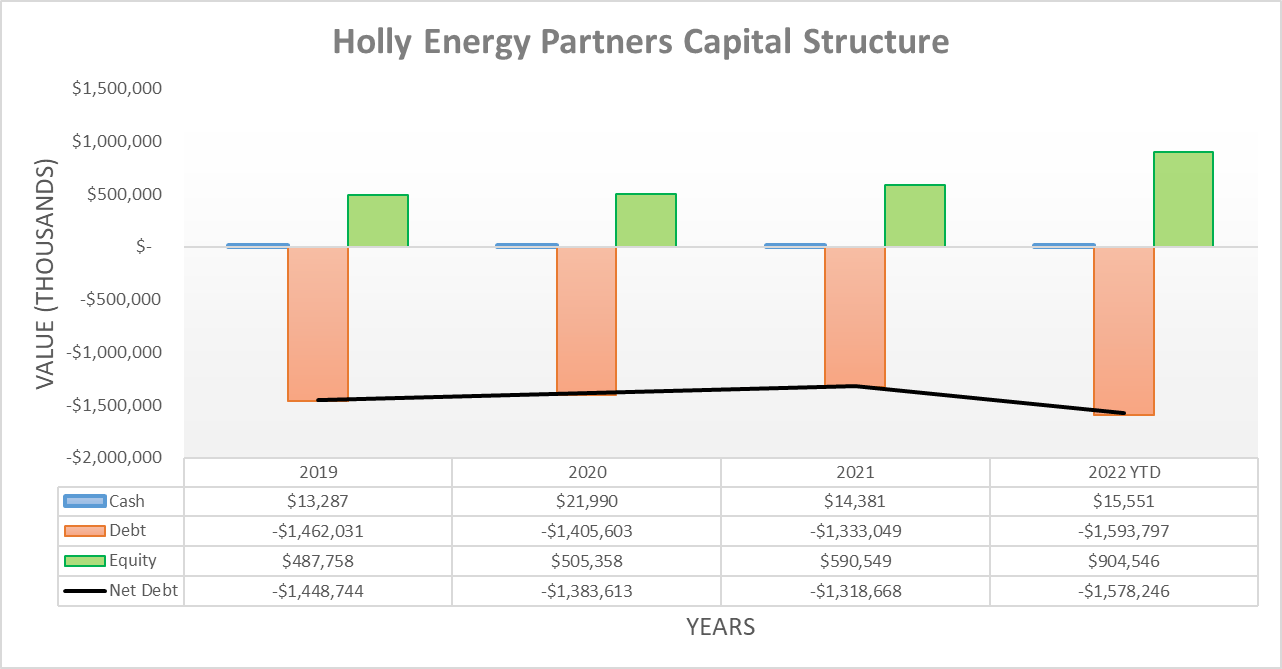

Following their net debt spiking during the first quarter of 2022, it began trending lower during the second quarter and given their improving cash flow performance, it subsequently continued during the third quarter. To this point, their net debt is now $1.578b versus its previous level of $1.594b following the second quarter and whilst this only represents another small decrease of circa 1%, it still compounds into a meaningful improvement as the quarters turn into years. Since my previous analysis covered their leverage in detail, it would redundant to reassess this attribute in detail once again given this small change, plus the outlook for 2023 and their progress integrating their Sinclair acquisition were the primary topics. Likewise, this same logic also applies to their debt serviceability and liquidity too, as neither of these would have seen a material change.

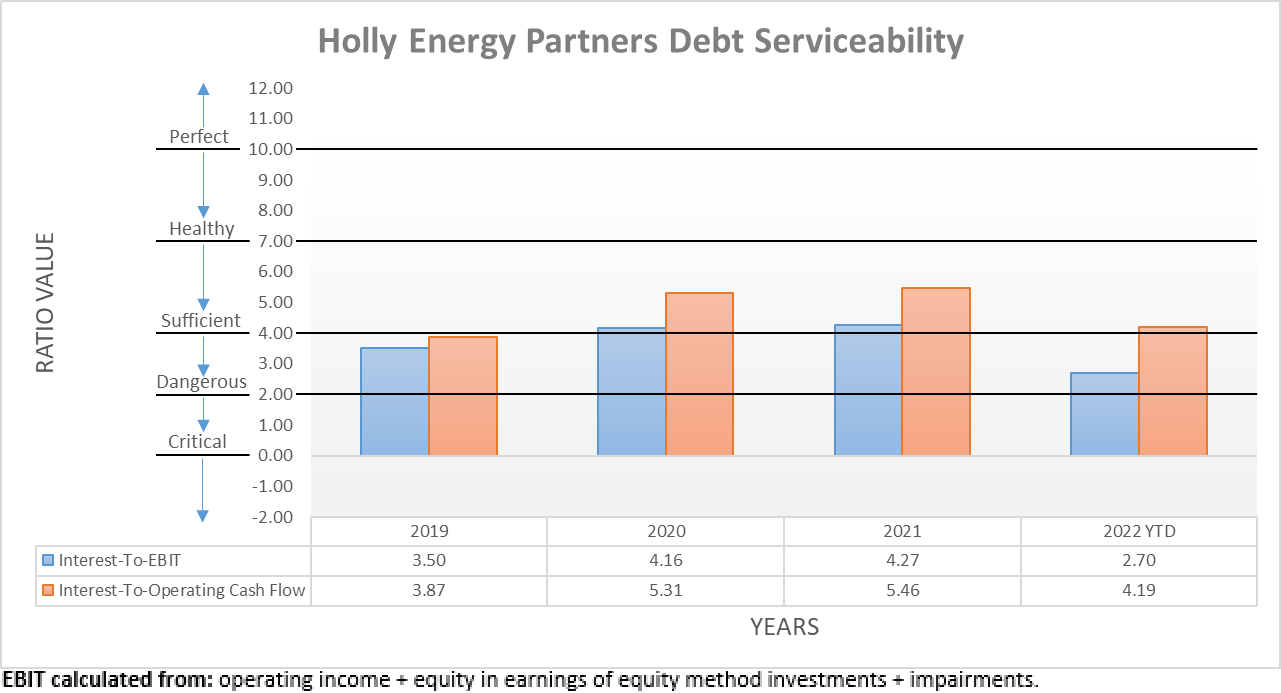

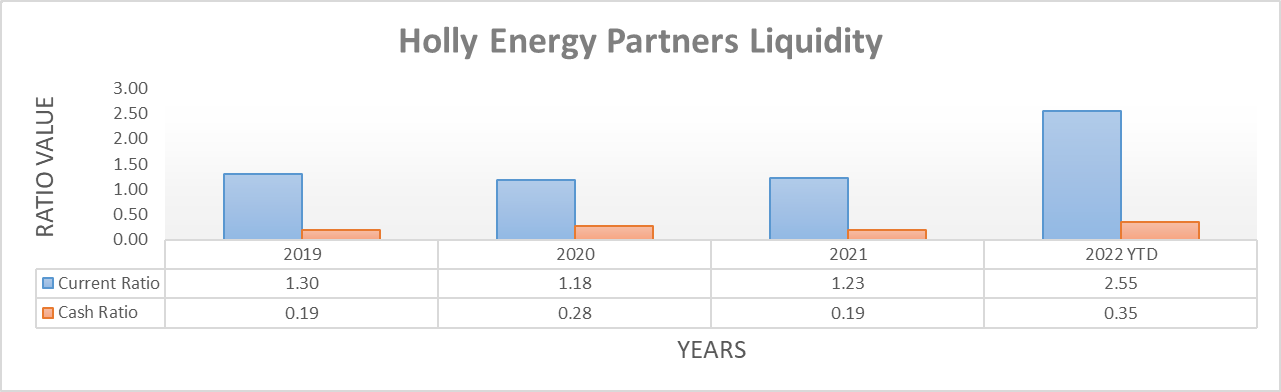

The three relevant graphs are still included below to provide context for any new readers, which shows their net debt-to-EBITDA is 5.19, whilst their net debt-to-operating cash flow is 4.96 and thus straddling both sides of the threshold of 5.01 for the very high territory. Even though their interest coverage is only 2.70 when compared against their EBIT, thankfully this remains sufficient and whilst a comparison against their operating cash flow sees healthy interest coverage of 4.19, I prefer to judge on the worse side. Meanwhile, their liquidity remains strong with a current ratio of 2.55 and a cash ratio of 0.35, which helps alleviate risks of their very high leverage in the foreseeable future whilst they reduce net debt. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

Conclusion

Even though their very high leverage is not ideal, it should fix itself as the benefits of their Sinclair acquisition continue flowing, not only through lifting their financial performance but also by keeping their net debt trending lower. It was positive to see improving cash flow performance during the third quarter of 2022 but that said, I was a little disappointed to see no further discussion of higher distributions. To be fair, they were put on the horizon only one quarter ago and they made no contrary commentary this time. When combined with their outlook for even lower capital expenditure during 2023, it seems the scene is set for higher distributions, which unsurprisingly means that I believe maintaining my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Holly Energy Partners’ SEC filings, all calculated figures were performed by the author.

Be the first to comment