VioletaStoimenova

Investment Thesis

Hims & Hers (NYSE:HIMS) is a telehealth company. That’s what it describes itself as. In fact, what it does is sell pills online. Pills aimed at men. Erectile dysfunction (”ED”) and hair loss drugs.

Nonetheless, this company is growing at an impressive rate, particularly given the macro backdrop facing this small company.

But what I’m particularly interested in are two dynamics. Firstly, analysts are now upwardly revising their revenue estimates for HIMS. Secondly, the company is becoming increasingly profitable.

Analysts Buy Into the Story

As an investor, the best type of stock to buy is one where the valuation is bombed out, but the company is actually delivering positive results, and not getting rewarded by investors.

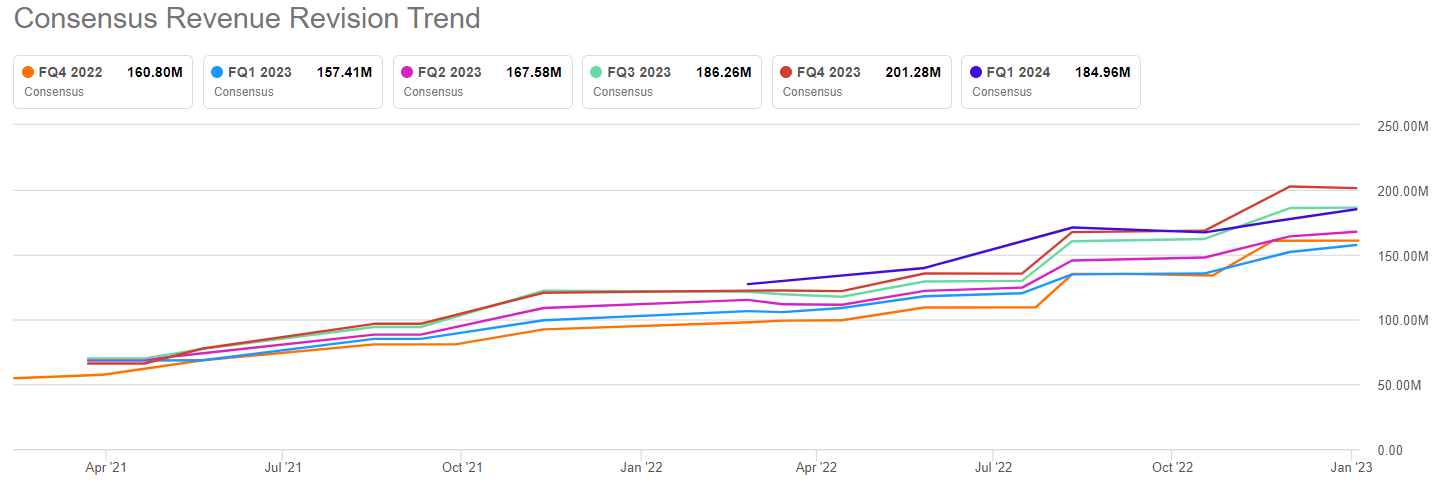

And that’s what you see below. Over the past several months, analysts have been consistently upwardly revising Hims’ revenue outlook.

HIMS revenue estimates

That’s a positive step up. Next, consider Hims’ subscriber growth.

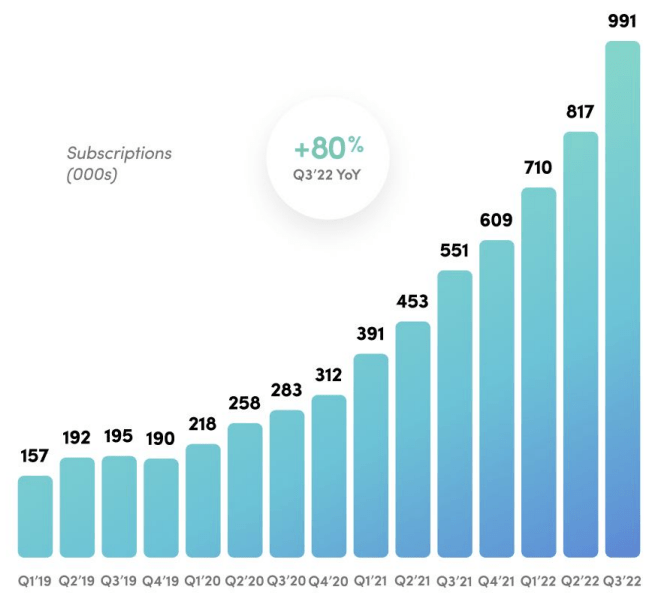

HIMS presentation

What you see here is that in Q3, net new subscriptions were up 80% y/y. We are well into the law of large numbers for this small outfit, and yet, subscriber growth remains astonishing. I believe you’ll agree with me.

Hims is a telehealth company. The way it works is that it attracts millennials online to subscribe to its products. But more concretely, Hims wants customers to subscribe to its products.

With that in mind, consider this comment from the earnings call,

Now at a time when others may be pulling back or fully hitting the brakes on new investments, we are taking advantage of marketplace opportunities to continue building long-term foundational elements throughout our business.

With this quote in mind, let’s move to the next section.

Q4 2022, In the Bag Already

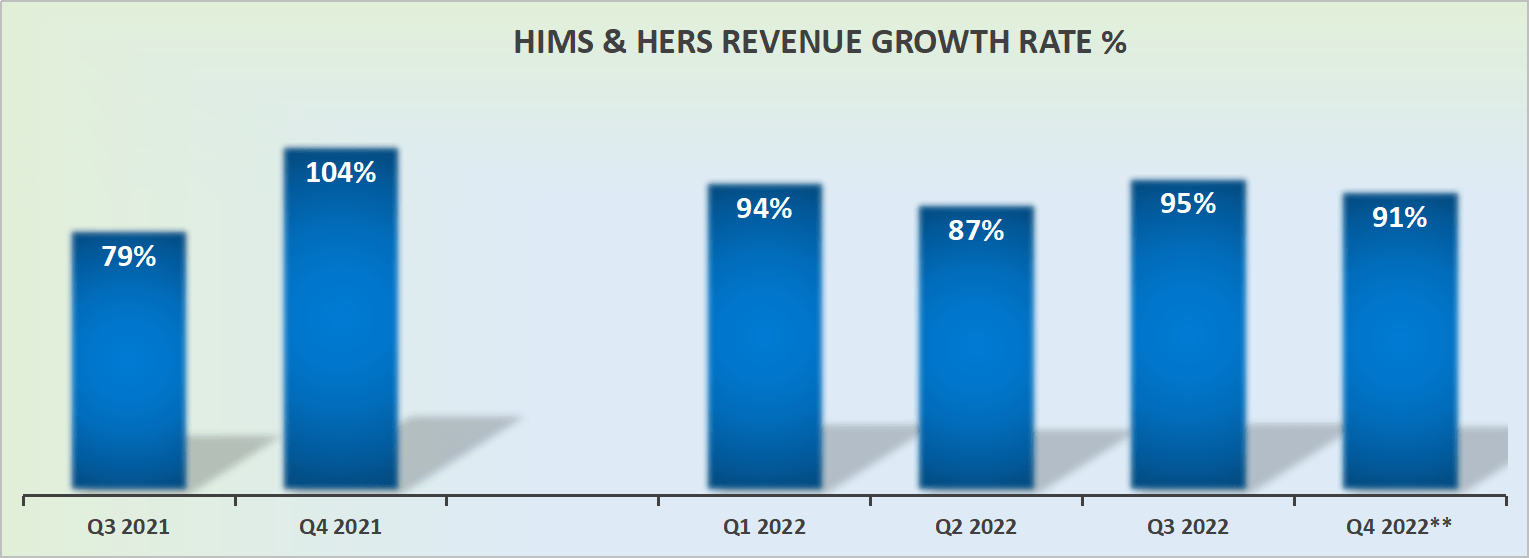

HIMS revenue growth rates

Think about the guidance for Q4 2022, and how it compares against the same period a year ago. Hims’ growth rates are showing no signs of fizzling out. This sort of CAGR is impressive.

OK, the numbers look good, now tell me more about its profits.

Profitability Profile Moving in the Right Direction

For last year’s Q4 2021, Hims’ adjusted EBITDA was negative 8%. Meanwhile, the guidance for Q4 of this year points to 0% EBITDA to a positive 1% EBITDA.

Think about how significant a change this is to the story? This is no longer a busted SPAC story.

Here’s a company that’s rapidly growing, cheaply valued, and going to be profitable in 2023!

HIMS Stock Valuation — For Now, Still at 2x Sales

If we presume that Hims grows its revenues by 60% y/y in 2023, that would put its revenues at $830 million. This leaves HIMS priced at less than 2x revenues.

And if the company can end up 2023 with approximately 2% of EBITDA this would put the stock at 94x EBITDA.

And now, you may say, 94x EBITDA is crazy. There are companies out there that are priced at 10x EPS, paying +90x EBITDA doesn’t make any sense.

But I urge you to see things from this perspective. The companies that are priced at less than 10x EPS are either cyclical companies, or they are companies that are growing at 2% to 4% CAGR.

Young companies growing at +50% should not be maximizing earnings at this stage in their business cycle. They should be maximizing reach and scale. Throwing things at the wall, to see what sticks. What works. What avenues to further invest in.

What Are Risks?

No investment is without risks. This is a very small company and that means that capital flows in the short term, anything less than six months, and Hims can be highly susceptible to investor sentiment.

Another significant consideration is that there is a plethora of competitors. Not only online, but offline too. So, Hims has to not only compete with unbranded products but also has to compete against much stronger brands, that customers are already familiar with.

Another significant risk is that as the company scales, it is going to face bigger challenges. For example, Hims has now acquired a large distribution facility in Arizona. Its ability to rapidly and cheaply distribute pharmaceutical products to a customer’s doorstep is quite different from acquiring customers online.

There’s no assurance that this transition will be successful.

The Bottom Line

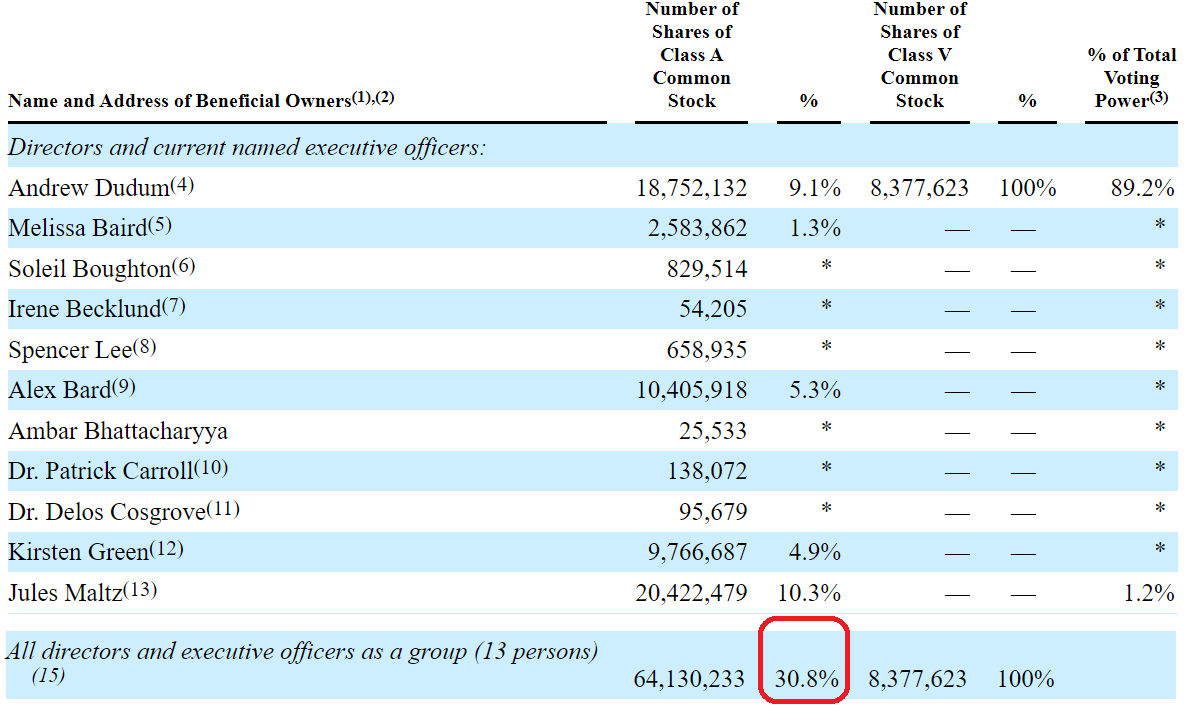

There’s really a lot to like about being a shareholder here. What’s more, management owns about 30% of the company. So, you can be sure that they are highly motivated to drive shareholder value, by being attentive to how investors value their company.

HIMS proxy statement

The stock is really cheap, even now.

Be the first to comment