MicroStockHub

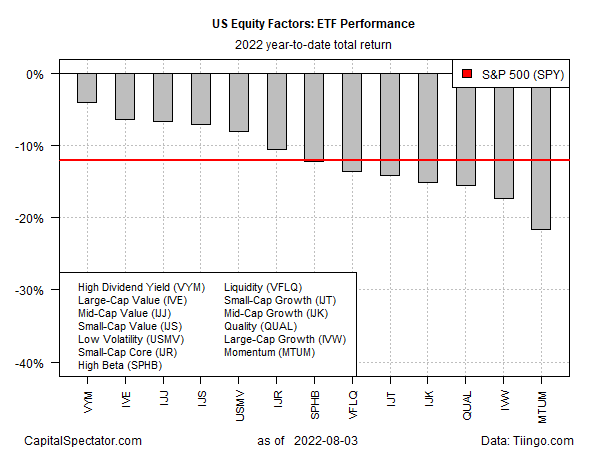

The stock market is showing some bounce lately, but on a year-to-date basis, red ink still dominates. Looking at equities through a factor lens, however, continues to show a wide variety of losses in 2022. Notably, the softest setbacks are (still) in high dividend and value strategies, based on a set of proxy ETFs through yesterday’s close (Aug. 3).

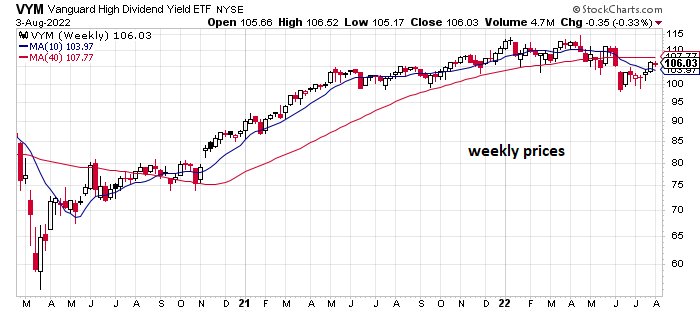

Vanguard High Dividend (VYM) is still leading the field with a relatively light year-to-date loss of 4.0%.

StockCharts

Several flavors of value are only slightly behind VYM. By comparison, a broad measure of the US stock market (SPY) is down a bit more than 12% this year while the biggest loss for our factor set is suffering with a hefty 21.6% loss, based on iShares MSCI USA Momentum Factor ETF (MTUM).

Author

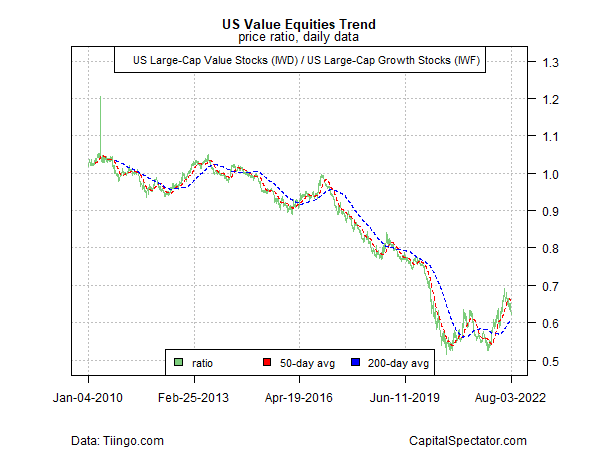

Advocates of value investing are quick to celebrate the relatively light declines for the strategy and point out that growth has taken a heavy hit this year. By some accounts, this is evidence that 2022 marks a turning point – the year when the long-suffering value factor returns to form and begins an extended run of outperforming growth.

Maybe, but skeptics continue to ask if macro changes over the past couple of decades have reordered the prospects for value’s historical outperformance. That’s a big discussion and we’ll sidestep it here. On a tactical basis, however, it’s clear that the value mojo has kicked in lately. But as the chart below shows, the factor’s leadership is waning again vs. growth, based on a comparison of two large-cap proxy ETFs. After a strong bounce this year, the relative strength of value vs. growth has reversed course rather sharply. This could be noise, of course. Let’s see if the second half of the year tells us otherwise.

Author

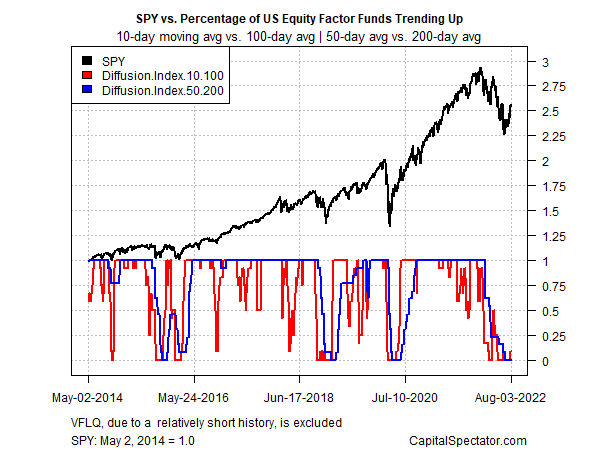

Meanwhile, there’s no doubt that factor strategies writ large have posted the weakest run in several years (see chart below). For contrarians, that’s notable since it suggests that the odds for a bounce look encouraging. The main risk to this forecast is that we’re in an extended bear market and so any bounce will be short-lived. Distinguishing between the two scenarios is the critical question. In the current macro climate, however, high-confidence answers for one scenario or the other are elusive, arguably more so than usual.

Author

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment