jessicahyde/iStock via Getty Images

Thesis

The Direxion Daily S&P 500 High Beta Bull 3X Shares (NYSEARCA:HIBL) is an exchange-traded fund. The vehicle seeks daily investment results, before fees and expenses, 300% of the performance of the S&P 500 High Beta Index. The S&P 500 High Beta Index measures the performance of the 100 constituents in the S&P 500 that are most sensitive to changes in market returns.

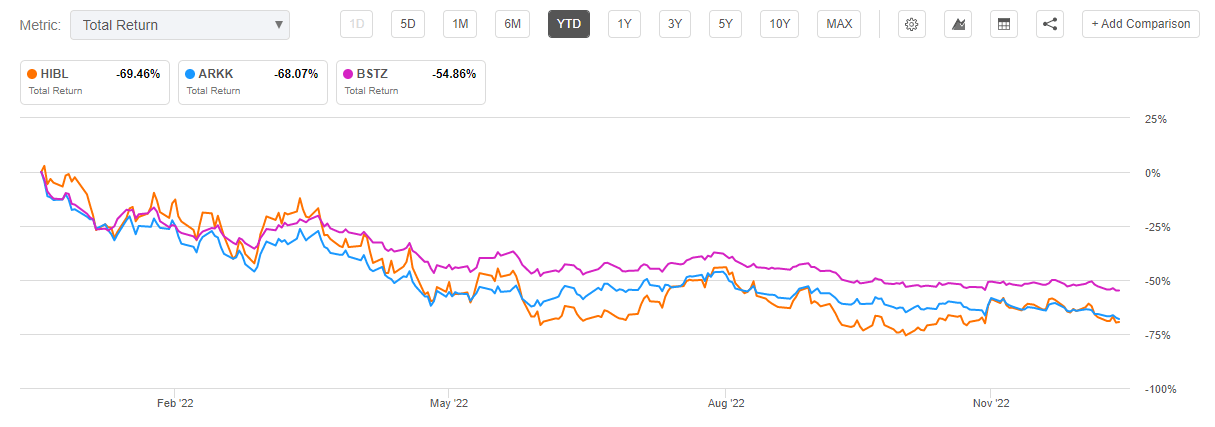

Please note that leveraged products are fundamentally not buy and hold investments, and come with specific risks as identified by FINRA. What is surprising though is that FINRA does not hold the likes of ARK Innovation ETF (ARKK) to the same standard, although their return profiles year to date are almost identical. Leverage magnifies returns, both on the way up, as well on the way down. We were expecting HIBL to be down since it represents a leveraged take on the most volatile names in the S&P 500. However, the fact that HIBL’s return profile is identical to ARKK’s speaks volumes of the embedded leverage in the ARKK structure that a retail investor is not aware of. Take a step back and think about that for a second – at the end of the day ARKK is a 3x leveraged play on the most volatile names in the S&P 500! Fairly shocking, and it comes without a disclosure label.

Beta is a fundamental concept in portfolio management and specifically market risk management. Beta measures a stock’s move relative to the overall market. A beta greater than 1.0 indicates that a stock is generally more volatile than the overall market, while a beta lower than 1 references stocks that tend to move less than the market. For example, a stock with a beta of 2 will move twice the value of the overall market. So if the S&P 500 experiences a 10% correction, a stock with a beta of 2 will have a 20% correction.

HIBL is very transparent regarding what it is – a 3x play on high beta names in the S&P 500. As a leveraged product this falls in the speculative bucket of investments, not a true buy and hold name. HIBL is well suited for bull markets, for risk-on environments, not for today’s market. There is more weakness to come in the equity space as we have clearly outlined here, and HIBL will be dragged down even more.

What is shocking to us is that highly leveraged, high beta names such as ARKK or BSTZ for that matter, are hidden in plain sight without proper labeling. You can have leverage outright as HIBL does, or hidden via the fundamental structure of the underlying companies (an enterprise which does not produce an operating profit and exists only on promises of future returns is intrinsically leveraged) as present in ARKK or BSTZ. Higher rates have wacked high beta, high leverage names. And the move is not over. However, many investors fail to realize that what inflated the underlying companies in the first place via leverage were low rates, and rates are going to be higher for longer. As an asset manager it seems that it is easier to trumpet good returns in an up-market by simply hiding the leverage factor, while in a down-market a “V-shaped” recovery is marketed to retail investors.

We like HIBL because it does not hide what it is – a 3x play on high beta names in the S&P 500. However there is still another -20% to go in this ETF before the bear market is over. Unfortunately investors in other highly leveraged but well disguised vehicles are going to be very late in realizing what the complex structure they bought is truly hiding.

HIBL Performance

The fund has a total return performance and slope in 2022 almost identical to the one exposed by ARKK:

YTD Total Return (Seeking Alpha)

Another disguised high-beta fund, namely BSTZ is also down significantly, albeit with an ‘outperformance’ of 10%.

HIBL Holdings

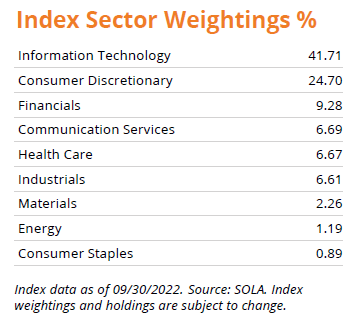

The fund is mostly exposed to technology names from the S&P 500:

Index Composition (Fund Fact Sheet)

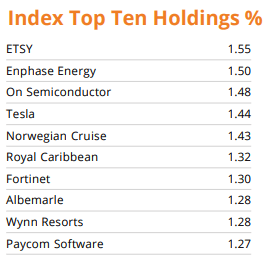

The top names are a mix:

Top Holdings (Fund Fact Sheet)

Among technology names we can find semiconductor companies and cruise line operators in the top ten holdings.

Conclusion

The Direxion Daily S&P 500 High Beta Bull 3X Shares is a leveraged vehicle. The fund aims to offer 3x the return of the top 100 constituents in the S&P 500 that are most sensitive to changes in market returns. As a leveraged product the fund is not suitable for true buy and hold investors. Its performance this year (down -69%) has exemplified its speculative nature. What is interesting to note however, is that HIBL’s return profile in 2022 has been almost identical to ARKK’s. While the fund has a 40% weighting to technology stocks, it does not chase innovation, but purely magnifies leverage in the highest beta name components for the S&P 500. There are a number of vehicles in the investment space such as ARKK, which in fact represent highly leveraged plays on certain market themes. HIBL is transparent about what it is and what it does, and the likes of FINRA have made sure outright leveraged products have been getting the proper label and disclosures. The bottom is not in for HIBL, the same way the bottom is not in for the wider equity markets. Expect another substantial leg down here that will bring the fund’s performance over -80% on a year to date basis, being emblematic of what leverage can do to a retail investor on the way down. We are hopeful that other products that disguise leverage via their holdings might be getting a closer look from regulators in the future as well, so that investors can better grasp the concept of magnified returns, both on the way up when everybody is cheering, as well as on the way down.

Be the first to comment