Thossaphol

The Investment Plan

Hess Midstream LP (NYSE:HESM) is a company in the United States operating in the natural gas and oil sector. Here they focus on developing, operating and acquiring midstream assets. Within the company they have three different segments, the first one being gathering. Besides that there is also Processing and storage and lastly terminaling and export. As they are in the middle of the processing line from raw material to something usable, they have a vast network of pipelines all across America. But they have also invested heavily into the storage part in order to hedge against times when the price of natural gas or oil might be unfavorable.

As the company is increasing the bottom line at a fast pace, the current valuation makes more sense. But as I am a value investor, I always look for favorable entry points. With Hess it’s a bit high and I think it’s better to just hold and wait for a potential drop in price.

Latest Earnings Report Highlights

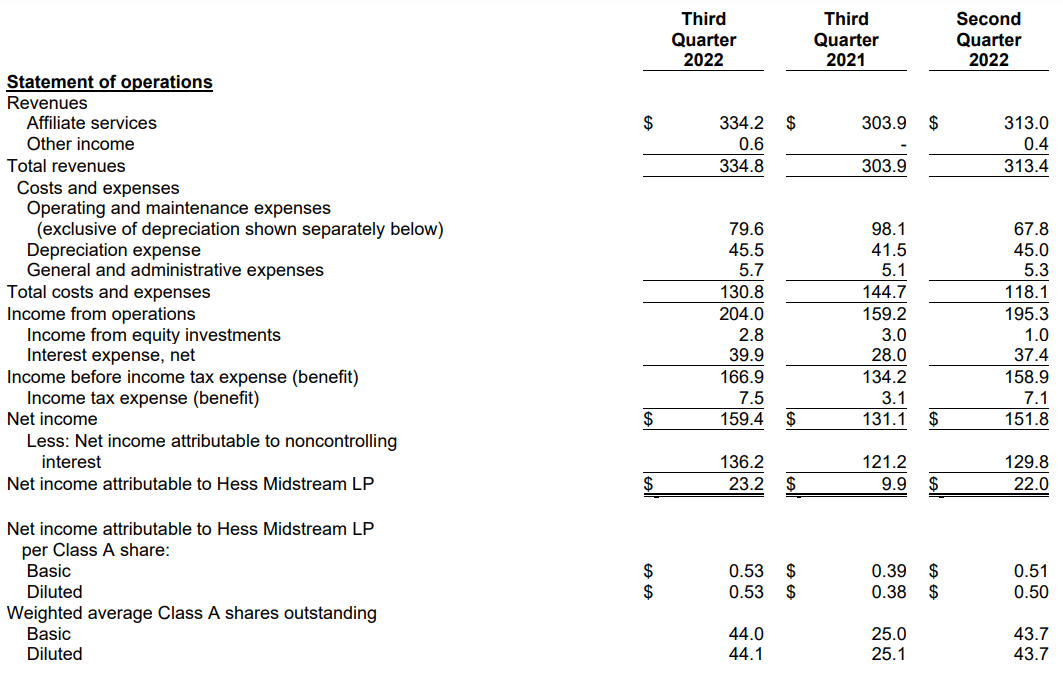

On October 26, 2022, Hess Midstream LP reported earnings for the third quarter of 2022. Looking at the top line they saw an increase of 10.2%. The revenues landed $334 million compared to $303 million the year before. A big reason for the company’s ability to generate higher revenues was primarily due to higher outputs of water and gas, but also slightly higher tariff rates. The costs and expenses saw a decline in the quarter compared to last year. Much because in 2021, one of the facilities saw a maintenance cost to it that drove the company’s quarter expenses higher.

Hess Midstream Income Statement (Hess Q3 Report)

Much thanks to this decrease in costs, the EPS for the quarter saw an increase of 35% YoY. This ended up making the EPS $0.53 compared to $0.39. With an increase in margins, the road ahead seems bright for Hess Midstream in my opinion.

As the company saw a strong quarter, they are also raising the guidance for the year of 2022, expecting to have net income around $630 million.

John Gatling of Hess can be quoted saying “We are raising our 2022 operational and financial guidance, reflecting our expectation for continued strong performance through the end of the year”. I think this is great news as sector tailwinds are ahead of them, and with the management prioritizing investors and shareholders, they seem to be doing everything right.

Sector Outlook

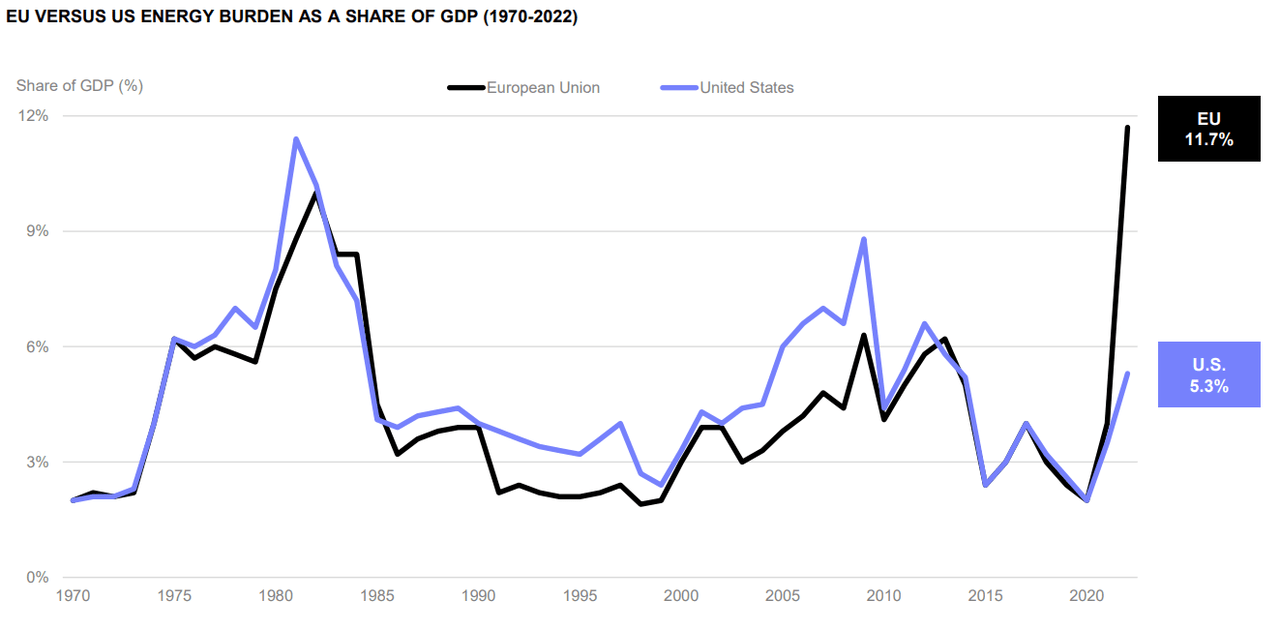

Looking at the entire energy sector there should be nothing but tailwinds ahead. As more and more demand is placed to keep up with expansion and innovation. I think that we need to look a bit closer, however, on the different industries within.

Hess Midstream being dependent on the natural gas and oil demand for their revenues, I think that there are clear headwinds for them, such as the IRA pushing for more renewable energy sources. But some investors might forget that complete adoption to these types of energies are far away. In the meantime, the demand for oil and natural gas remains high. With the ongoing war in Ukraine, it pushed oil prices to new highs in 2022. But the same goes for natural gas, as Europe is becoming a much bigger customer now.

The Sector Outlook (Gsam.com)

Looking at the midstream part specifically, I expect companies to start expanding more internationally. I think that strategic foreign acquisitions will play a big part for the company’s success of keeping up revenues and good cash flows. I also think that the revenues you can see from companies like Hess Midstream will be a bit all over the place in the coming 5 years at least. Much because commodity prices for oil and gas are going to be affected by macro events. But where there is volatility, there is opportunity and with a good management team they could capitalize heavily from this.

Competition

The energy sector has seen plenty of growth in the last few years. An increase in demand has made companies see much higher revenues. In the niche of natural gas and oil, these sources have become incredibly important as prices are soaring for them and the reliance on them is still high. Some companies have seen incredible but unsustainable growth, which creates risky investment situations.

But looking at some similar valued companies that also compete with Hess Midstream I see some interesting choices. Between EnLink Midstream (ENLC), Battalion Oil Corporation (BATL) and New Fortress Energy Corp. (NFE) they all share a similar growth pattern. NFE being perhaps the fastest growing of them all. They all have a massive TAM where they operate by finding and exploring new sites where natural gas and oil might be located.

From an investor’s point of view, Hess Midstream is in a good position. Like I have mentioned, they have steady growth outlooks and offer a very good dividend yield at around 7% right now. But if an investor wants something a bit more growth oriented then NFE seems like a good deal. Growing rapidly and taking more market share they are likely to become a bigger and bigger competitor to companies in the industry.

The Balance Sheet

With the balance sheet there are a few things I like to particularly look at. The cash they hold in relation to the debt that they have but also the ratio between total assets and the total liabilities. Seeing the increase of them both is good information to see how the company is able to leverage investment and expand. Looking at potential share dilution and the cash flow situation is also important to me.

Company Cash Position (Seeking Alpha)

Hess has been able to grow their cash position by around 18% YoY and in the latest earnings report they had $2.6 million in cash. With no current debt at least, the current cash position will make an unnoticeable dent in the long-term debt of $2.9 billion. This has me worried that the company might not be able to pay debt on time without major share dilutions.

Company Liabilities (Seeking Alpha)

On the assets the company holds a large portion of it as property, plant and equipment. Thankfully the total assets are right now outweighing the total liabilities by around 16%. A major part of their liabilities are held as long-term debt. I think that the focus for the management in the next years will be to pay this down more and gain a more favorable financial position.

Outstanding Shares (Seeking Alpha)

The shares for the company have seen a roller coaster in the last few years. But the current trend seems to imply that they will continue to dilute shares and decrease the value for shareholders. I believe this further increases risk with making an investment into the company.

Cash Flow History (Seeking Alpha)

What gives me a little confidence at least is that the cash flows for the company are positive. I think this should help the management lessen their reliance on diluting shares for raising capital. It will also greatly help paying down debt as they have $389 million in TTM free cash flow.

Valuing The Company

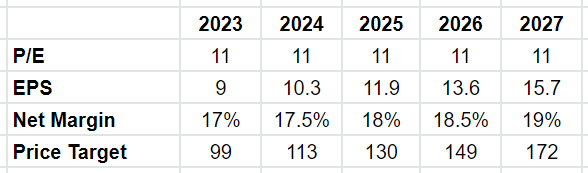

Hess Midstream is a steadily growing company, but has a quite rich valuation at a TTM of 23. This is a bit above the sector average of just 8. But looking at the forward estimates I have, this valuation seems to get less and less rich for each year as the company increases their bottom line by margin expansion.

Future Valuation (Author’s Own Calculations)

I think that the valuation needs to come down for Hess if there is an investment case to be made. I have a terminal p/e of 11 as I think the company is able to grow their net income around 15% CAGR. This valuation is also above the sector medium. I think that the margin increase will greatly help with this EPS increase YoY.

If my estimates are correct then this would yield an annual return of about 14.6%. A very healthy return and something that would beat the markets too.

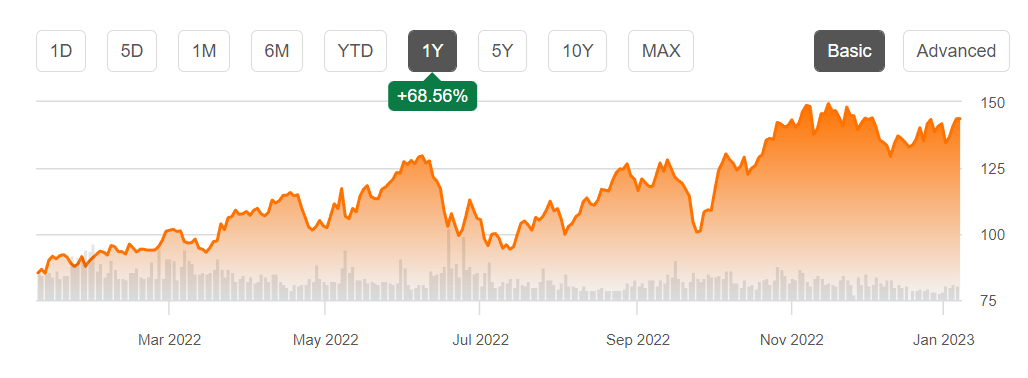

Price Chart (Seeking Alpha)

But in order for this to happen the share price would need to drop another 44%. This seems unlikely as investors are buying the company for the bright future it seems to have.

All this leads me to have a hold for the company. I think that there is a very good entry price to be had, but a drop to those levels seems unlikely. The valuation matters a lot and right now it’s far above the sector average.

Conclusion

Hess Midstream is seeing large demand as commodity prices soared in 2022. This has led them to have record quarters of growth and margin expansions too.

Out of some close competitors, Hess seems to have a relatively good valuation as they are growing faster than some of its peers even. A clear red flag, however, for investors would be the high amount of debt they have currently. $2.9 billion is a substantial amount that will take time to fully pay off. I think this will weigh on the company for the foreseeable future.

Like we said previously, evaluations are important and right now the share price for Hess is too high for my liking. I still think it’s worth holding on to any shares as they are expected to continue to grow. If the share prices sees a compression then I think that would be a great time to add more to a position though.

Be the first to comment