imaginima

Hess Corporation (NYSE:HES) management made a presentation and guided to a production triple in Guyana by fiscal year 2027 when they expect to have 6 FPSOs producing oil. Management then spent a fair amount of the conference talking about adding significantly more known reserves in their presentation simply by going to 18,000 feet because they “know” the oil is there.

Many of the discoveries posted are at the 15,000-foot level. The reason for this strategy (to drill deeper) is that once you “know” something in this industry, like the oil is there, then usually the exploration is far less risky than normal. Of course, there is the risk that the oil is less than imagined or not there at all. There is also the potential for even more upside.

Suriname

There is also the news that both partners in different partnerships have an oil discovery in Suriname. One of the things that both Exxon Mobil (XOM) and Hess have discovered is that discoveries themselves generate very little additional interest in the stock prices. The market waits for cash flow as a result of those discoveries.

This means that a discovery could prove to be not commercial for any number of reasons. Even if the discovery is commercial, it takes about 5 to 7 years for that discovery to begin producing. The most optimistic assessments I have seen assume that the first oil will happen in 2025. Hess stock actually did not “take off” until (approximately) the second platform was about to be delivered and begin production. There is not a whole lot of reason to believe that Suriname will prove much different for investors.

Suriname, like Guyana, has no industry before the current industry interest. Therefore, infrastructure and supporting industries all have to be built and established from ground zero. As a result, it takes quite a bit of oil for a discovery to be commercial because of everything else that has to be established before that oil can be produced.

That is very different from the United States Gulf of Mexico, where there is an established industry. In the United States, it takes far less oil for a commercial discovery because of all the supporting things in place.

Guyana

Probably the biggest deal here is that Exxon Mobil is the operator. It would be hard to find a better operator for such a large project than Exxon Mobil.

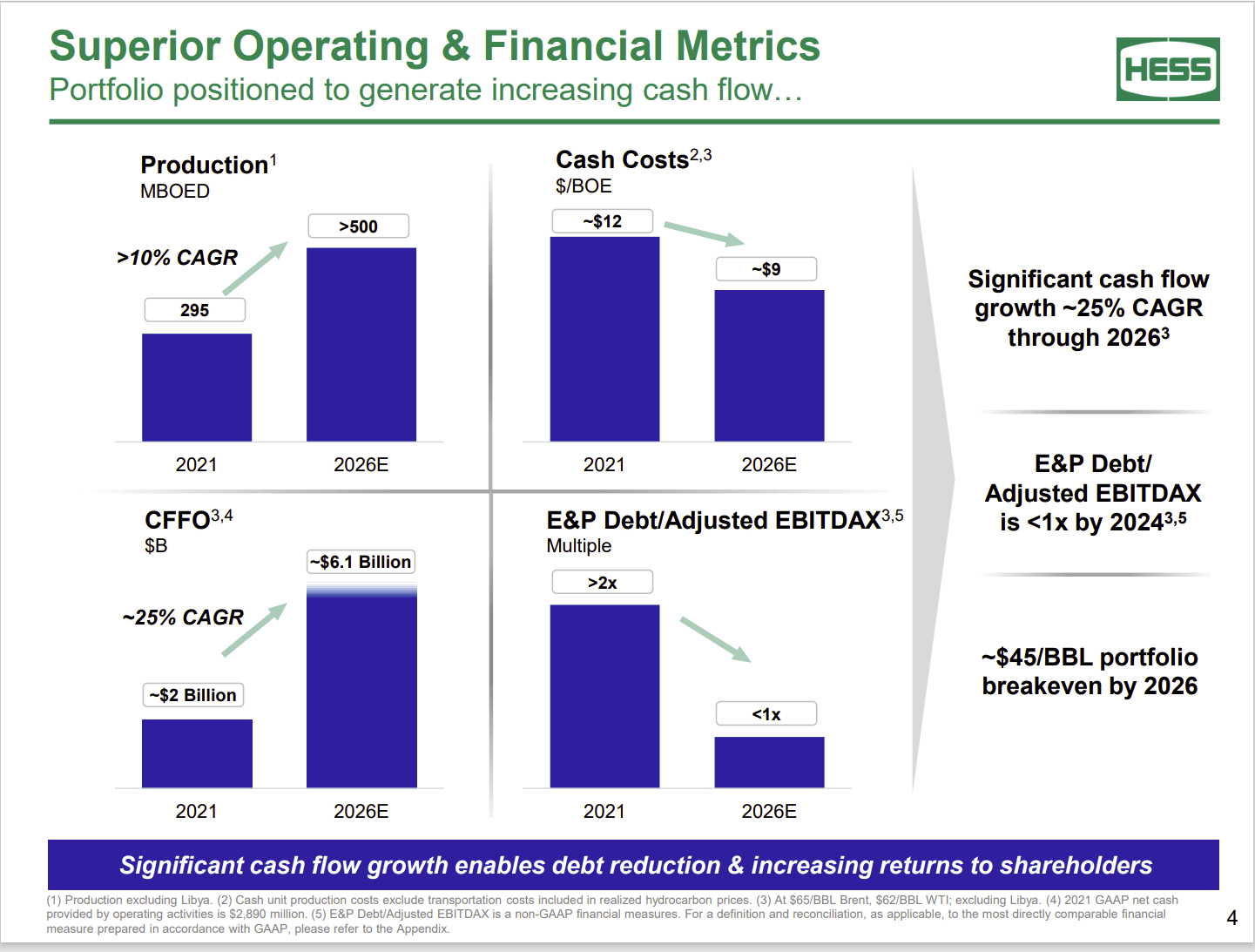

Hess Guidance On Key Financial And Operating Results For A Five Year Period (Hess Presentation At Bank Of America Global Energy Conference November 2022)

The first thing to note is that this guidance assumes nothing from the current discovery in Suriname. That is because the discovery has not been completely evaluated. Even when it has been evaluated, more discoveries will be needed to justify production.

The second thing to note is that the forecast assumes a Brent price of $65. Therefore, cash flow may not triple from the levels noted because the price of Brent is currently higher than the assumptions used. On the other hand, if prices remain higher for five years, the company could easily beat that guidance. Tripling cash flow in roughly 5 years is a 25% compounded rate of return.

Because Guyana production should at roughly triple in the time period noted, Hess production in total will at least double. (It depends on how you count the production rate for this current fiscal year as an FPSO began producing this year.) The other number that makes an appearance throughout the press is that the 6 FPSOs at that time should produce 1.2 million barrels of oil per day. Hess has a 30% share of the partnership production. That tells you how conservative the guidance above is.

At some point, there will be enough established production to add more than one FPSO every 18 months or so. Then I think you will see future guidance accelerate.

The same goes with the Suriname discovery. Should that discovery prove large enough, then that operator will be developing it for production, which will only add to the upside potential here.

Exxon Mobil has mentioned in the conference call that they intend to spend the capital money where it gets the “most bang for the buck”. At the same time, they mention how profitable Guyana and potentially Suriname currently are. Therefore, it is likely that one can conclude that Exxon Mobil is pursuing this project first because it has world-class breakeven points that rival the best projects in the world.

This is the kind of project that is already significant for a company the size of Hess and will likely become very significant for a company the size of Exxon Mobil. Not many projects in the world have the potential to be that large.

Hess Implications

Hess is a relatively small company for the size of projects it has on its plate. That usually means, at some point, one of the larger partners in one of the partnerships will likely make an offer to take over the company. It is actually a cost-saving move with considerable synergies, should it happen.

It is less likely that a decent size company that wants Guyana exposure would make an offer for Hess.

No matter the future, there is an excellent chance that a relatively small company like Hess will receive an offer “down the road”. In the meantime, investors will enjoy a period of production growth that is seldom seen for a company the size of Hess.

The Future

Hess already has a very bright future just from the established Guyana production and upside potential. There are now some lower-risk exploration opportunities combined with the usual high-risk upside opportunities. That implies an accelerating growth curve for this project as it is nothing close to the mature phase.

The production mix will change from mostly unconventional to mostly offshore as Guyana production climbs. That will lead to a lower operating expense because the offshore projects have a high initial capital investment combined with lower actual production costs.

The key is that Hess costs do not have to decline in order for that favorable mix to bring average costs across the corporation down (even though that is likely to happen as well).

There is now the additional upside potential of a large Surname production in the future. The first discovery is being evaluated, but the additional discoveries in the area lend credence to a viable Surname business in the future that is a material addition.

The result of this is that Hess stock is likely to be far more valuable five years from now, even if oil prices are materially lower. The prices used in the guidance assumptions are lower, and cash flow still grows quite a bit from current actual levels. That is what a large, very profitable project can do.

This is one of the few growth stories in a cyclical industry. As a result, the stock is likely to more than double even under conservative assumptions. Should Guyana become a hot spot for investors or a market favorite, then there is no telling how high the stock could go as the market often goes overboard in a situation like this. The downside based upon the discoveries made is very limited if it even exists at all.

Be the first to comment