CloudVisual

(Note: This article was in the newsletter on January 6, 2023.)

Hess Corporation (NYSE:HES) recently gave a presentation to further clarify its growth and income objectives. That was followed by yet another corporate presentation maintaining that guidance. Management emphasized during that presentation that the Gulf of Mexico and the Bakken would return to pre-covid levels of production and then the company would shift to a maintenance mode to harvest that cash flow. Evidently, this cash flow is a source to be used for the very profitable Guyana partnership and the potentially profitable Suriname project. That makes Hess a growth story in an industry not known for growth stories.

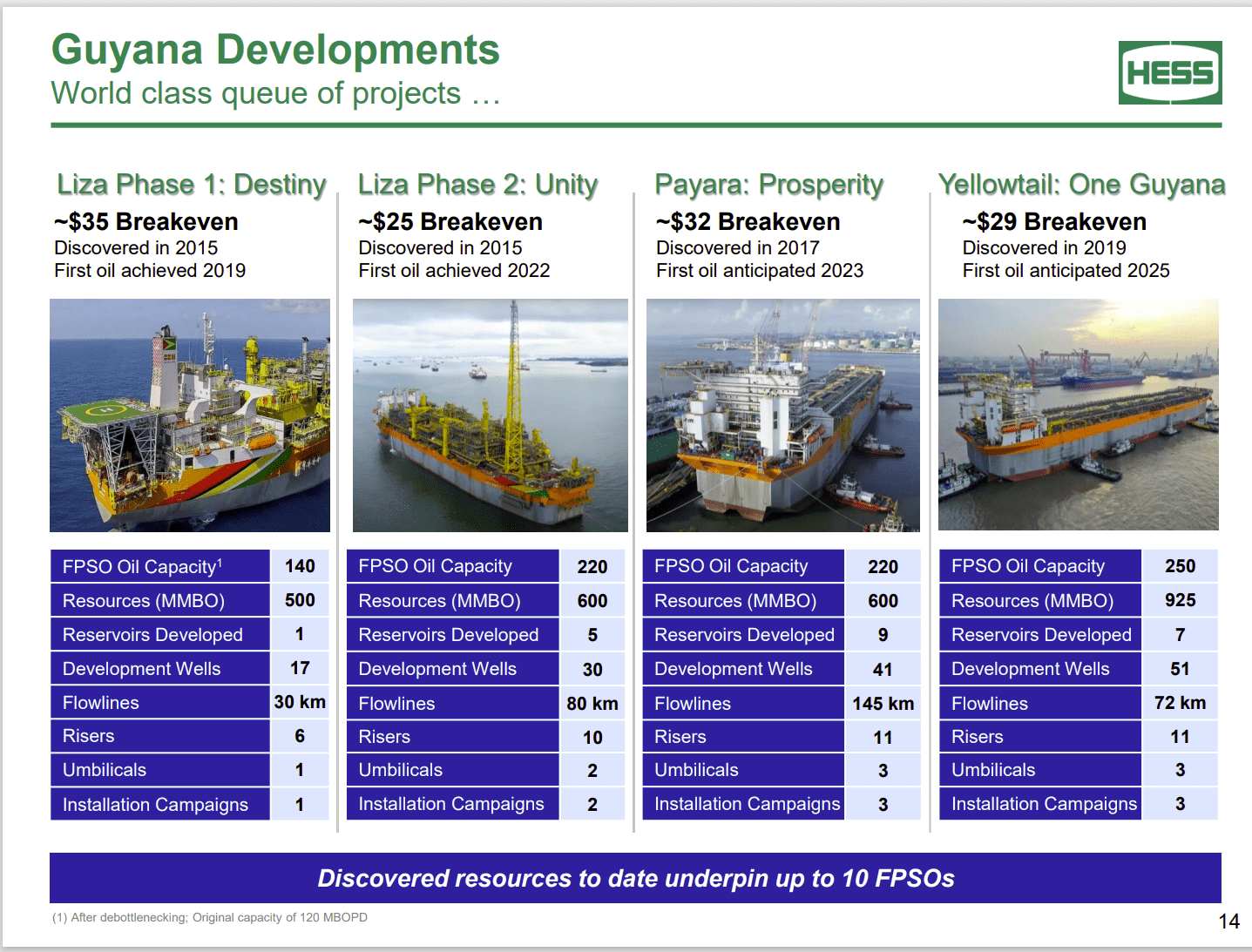

Furthermore, Hess noted that one discovery is large enough to potentially require its own FPSO. That has led to speculation about 7 FPSO’s by 2027. Exxon Mobil Corporation (XOM), the operator, has so far stuck to 6 FPSO’s and 850,000 BOPD by 2027. This gives investors a range of possibilities, as Hess implied 1,200,000 BOD for its numbers. The CEO of Hess strongly implied a rate of an FPSO a year, which is faster than the current pace. But it is also a likely pace, as production expands to provide more cash flow to expand the operations of this very large project.

Guyana The Present

The partnership has an FPSO that is 93% done. It does appear that prices on FPSO’s are going to climb. But the important part was that a lot of cash flow in the beginning due to strong commodity prices quickly pays back the cost of the beginning equipment. That creates a lot of free cash flow for expansion that might not have happened at lower commodity prices.

Hess Corporation Presentation Of Sanctioned FPSO’s (Hess Corporation February 2023, Investor Presentation)

John Hess, CEO, is a fair amount more optimistic in his projections than is the operator Exxon Mobil at the present time. He is projecting a seventh FPSO by 2027 just from the size of the Fangtooth discovery. That really “picks up the pace” of the current delivery of FPSOs at one every other year, and it does it soon.

One thing that underpins the development pace is that both partners have discoveries with other partnerships that may or may not prove significant. But the holdings of additional leases point to multiple projects developing production in the long term. Since Hess is the smallest partner of just about every group it is in, that means growth is unlikely to slow anytime soon.

My suspicion is that whether you agree with the timing or not, the project has discovered enough oil to justify a quicker development pace as soon as the cash flow from the project can handle it. So, it is more a timing issue than a “whether it can be done” type issue.

This also means that the partners need to agree to three more FPSO’s. Supposedly, there will be a final decision on the fifth one this year (probably in the first half of the year). Hess management has signaled that the breakeven for the next project is near the higher end of the range for the first four. But that is still a darn good number compared to many projects out there.

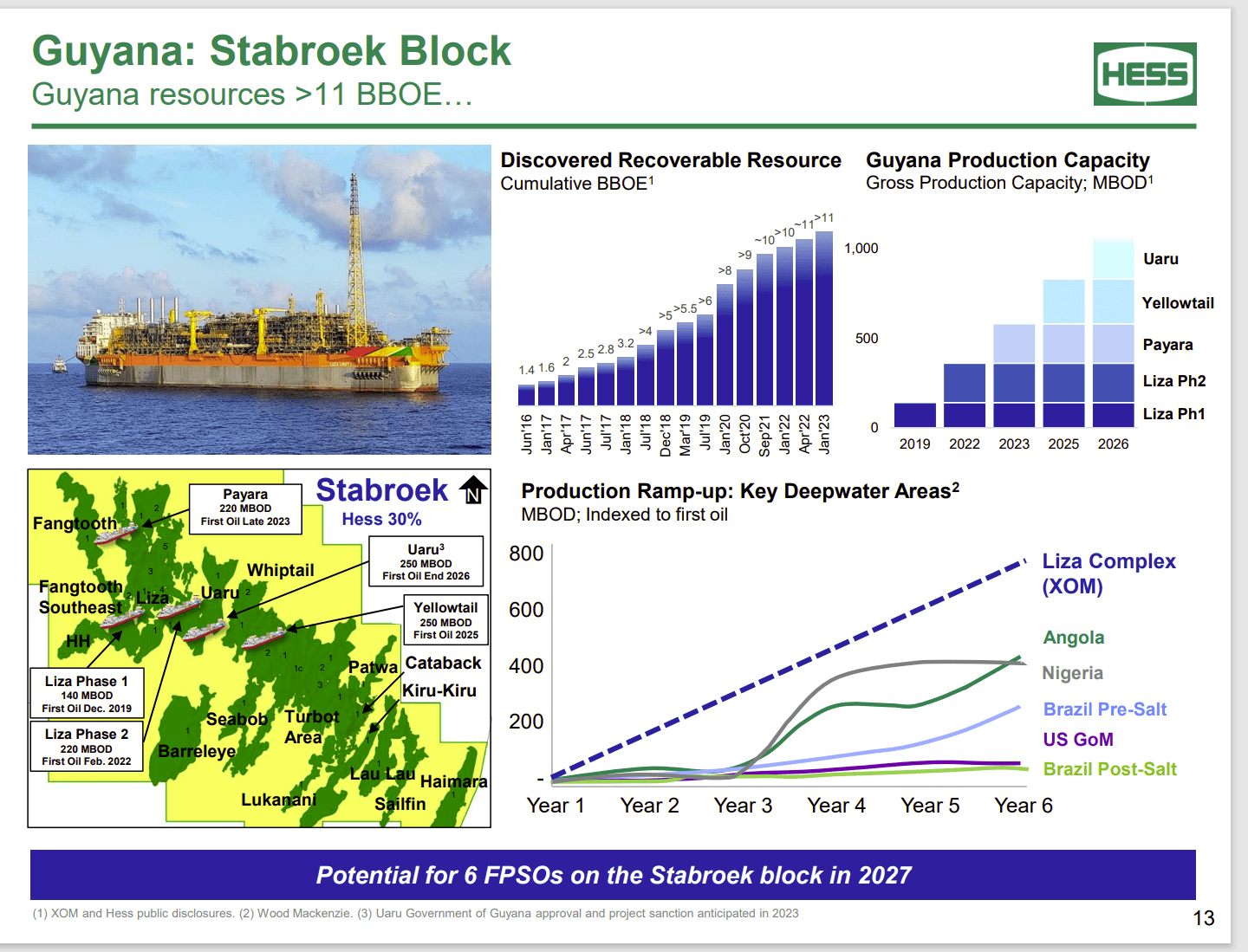

Hess Projection Of Production Increases For Guyana Partnership (Hess Corporation February 2023, Corporate Presentation)

The interesting thing about giant projects like this is that the pace will likely continue to pick up as the project grows. There is considerable upside here, as the partners in the project all have interests in other leases where there has been little to no exploration.

Similarly, discoveries are beginning to be announced in neighboring Suriname which have to be evaluated before any solid guidance can be projected. But should any of those discoveries amount to development potential, there would be still more upside potential for many of the companies already working in Guyana (because most have interests in Suriname as well).

This whole area represents a very large project for a company the size of Hess. As such, the current discoveries appear to give Hess the ability to very roughly triple its production by the end of the decade. Rarely does a company the size of Hess grow production at that rate.

The announcement of any material commercial discoveries would only add to that robust outlook. It would take a lot of dry holes (that really are not happening at this point) to dim future prospects.

The nice part is that Hess is a relatively cheap stock for the rate of growth. Most investors look for that rate of growth in technology. In that industry the same growth rate costs far more. But here, the cash flow will be apparent at Hess as production grows. There is an ability to pay a dividend, retire some stock all while growing very profitable production for the foreseeable future.

The best part is that Exxon Mobil is the operator of the project. So, all Hess has to do is approve low-cost expansions and cash the resulting checks. The experience of the operator handling world class projects lowers the risk of a misstep considerably while adding a lot of credibility to the projections about the future of the project.

The Backup Cash Flow Plan

Hess management is returning the Bakken and the Gulf Of Mexico production to pre-covid levels in case commodity prices were to sink low enough that additional cash flow is needed to keep the Guyana project expansion commitments. Hess also maintains an unused cash line “just in case.”

The low breakeven of the partnership in Guyana assures a rather robust cash flow under a wide variety of industry pricing projections. Current commodity prices have allowed the company to restore a lot of lost production while maintaining commitments to the Guyana partnership. Therefore, the company has a lot of liquidity options no matter what happens in the future.

Risks

Since Exxon Mobil is the operator, a lot of risks are extremely low because this is probably the best operator in the business. Expansion logistic challenges remain pretty low. Likewise, Exxon Mobil has a great record of not polluting, low injury rate, and cost control.

There may be some political risks not currently apparent as the project grows.

Pricing risks are low because of the very low breakeven

There is always the risk of a string of dry holes ending the upside potential at any time.

In short, this is a world-class project with some of the lowest costs in the industry and the one of the best operators one can have.

The Future

Hess provides a cash flow projection in the presentation for the reader. But this project is really just getting started. So, the parameters of the full project really have yet to be determined as long as discoveries roll in. If anything, the statement by John Hess about oil underlying the main reported discoveries so far at roughly 18,000 feet would imply a period of lower risk exploration ahead.

There are still several leases that really have not begun to be delineated, and the current lease where all the activity is still has a lot of acreage to be explored. So, this project could turn out to be a multi-decade project. Already it appears that Guyana will be a major oil producer for the foreseeable future.

As far as the value of the company goes, there are industry figures that oil is worth $5 per barrel in the ground. But it is really hard to put a figure on a discovery of this size until you know where the discovery ends. Right now, the operator, Exxon Mobil, has the happy task of extending the discoveries with more discoveries. Every quarter, there are more discoveries. So at least right now, the upside appears relatively unlimited until there are more dry holes reported.

When it comes to considering growth, there is a whole lot of growth potential here with Hess Corporation. The FPSO’s that management already feels are justified are enough to increase production from the Guyana field until the next decade. Every discovery announced each quarter adds to that.

What makes this even more intriguing is that the market no longer reacts to the news of a discovery as it did when I was a lot younger. Instead, the market waits for cash flow. So, unlike a lot of other growth companies, the pathway to more cash flow for at least a decade is well defined by the number of FPSO’s that the current situation justifies. Development drilling to and beginning production is one of the lowest risk functions of upstream.

Hess Corporation has a lot of well-defined growth ahead. Each quarter in effect adds to that growth potential as more discoveries are made. These projects have a lot of cash flow even at very low oil prices because most of the costs are borne up front to even begin production. So, like the thermal producers, these projects generate cash even during times when the project is losing money. But the low costs here assure that losses will not be something that happens often.

Be the first to comment