sankai

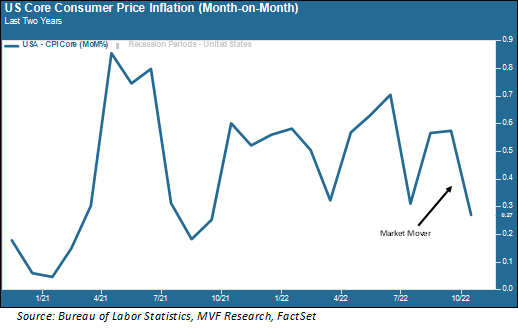

Did you ever wonder what it takes to send the Nasdaq Composite index higher by 7.4 percent in a single day? Here’s what it takes: a single data point showing that the core Consumer Price Index (i.e. the CPI excluding the volatile categories of food and energy items) rose by 0.27 percent from September to October. That’s it. Here’s the chart to put this momentous market mover in context.

As the chart shows, the September-October month-to-month move wasn’t even the biggest decline on record; the index fell even further from June to July. It was the expectations that mattered; economists expected that core inflation would rise by 0.5 percent, and it rose by less than that.

Voila, and out came the animal spirits. The S&P 500, which fell to a year-to-date low of minus 25 percent in the middle of October, built the magnitude of its recovery back by nearly ten percent, and is now down just 16 percent from January. Is this sustainable?

Impeccable Timing

Nobody knows what is or is not going to happen over the remaining seven-odd weeks of 2022, but we think the ingredients could be in place for a more substantial bounce than we have seen in some of the more effervescent relief rallies of late. A big part of this view has to do with the timing.

The final weeks of the year have a certain flavor in many years, a skew towards the positive. The holiday season puts the focus on retail and other consumer-facing sectors.

Money managers tend to “window dress” their portfolios by loading up on whatever looks hot, so as to avoid unpleasant conversations with their clients come January.

Forecasts for the year ahead are blasted from chief economists’ desks into the highways and byways of the financial media world. Most of those forecasts will wind up being egregiously wrong, but they almost always assume that prices will go up in the next twelve months. Good cheer abounds.

No News Is Good News

Of course, the “Santa Claus” rally, as Wall Street likes to call it, doesn’t come every year. Unpleasant surprises can happen in late November and December just as much as any other time of the year.

As we said earlier, anything can happen before the ball drops on New Year’s Eve. But we do not see much in the way of surprises ahead from the big directional stories of 2022: inflation, interest rates and corporate earnings.

On the inflation front, there is some evidence that supply chain bottlenecks are easing up: shorter wait times for cargo ships idling in ports, greater availability of critical industrial inputs and the like.

This may already be showing up in the inflation numbers; another benign CPI print in December would go at least some way in supporting the view that this week’s better inflation number was not just a one-off.

Interestingly, the CPI report in December will come out a day ahead of the Fed’s last meeting of the year. The Federal Open Market Committee will again, in nearly all likelihood, announce an increase in the Fed funds target rate, though it is not clear whether they will push for another 0.75 percent hike or decide that the time is at hand to dial back the magnitude of a single event to 0.5 percent.

It is unlikely that yesterday’s inflation report will by itself do anything to change minds at the FOMC, but another better-than-expected report could start to influence the thinking at the Eccles Building.

Even on the geopolitical front, where most of the news this year has been fairly grim, conditions seem relatively calm. Russia’s retreat from the strategically important city of Kherson this week could potentially open the door, if only ever so slightly, to talks aimed at ending the conflict.

Ahead of the forthcoming G20 meeting in Indonesia, President Biden will meet with his Chinese counterpart Xi Jinping, with a view towards easing the high level of hostility and distrust between the world’s two largest economies. And the US midterms this week, while still dragging on in the vote count to determine which party will control the House and Senate, served up nothing for markets to get antsy about.

There will be plenty of problems and challenges to address as 2023 comes into focus. For now, though, we think there is at least a reasonable case to make for more stable market conditions seeing us through to the end of the year.

Happy Veteran’s Day to all who are serving or have served our great country.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment