limpido /iStock via Getty Images

Introduction

The last couple of weeks of September were a rough period in the energy market if you were long oil or related equities. That’s probably the understatement of the year. Nearly every negative sentiment-recession, Fed tightening, dollar strength, China demand, inventory builds, or what amounts to the entire oil price Closet of Anxieties, came to pass during this period. Oil-WTI took a tumble below $80 for the first time since Jan 11th of this year, closing Friday, the 23rd below its 200 day moving average of $89.00. This move had WTI nearing an important psychological level in the lower $70s, past which producers might consider sharply curtail capex to raise prices.

The oil price began to rally as news of discussions of a substantial cut in OPEC+ output were heard. From a low on Sept. 26 of $76.72 WTI rallied to $86.52 on Oct. 4.

In this article we will discuss the key trends that should continue this rally into next year, creating investing opportunities in the companies that explore and produce oil and gas.

Trends are bullish for oil prices

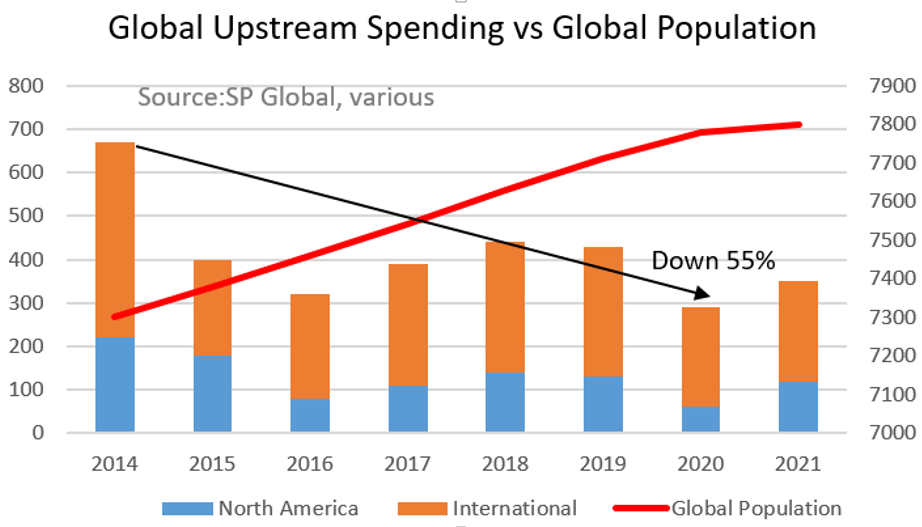

Longer term, we’re confident that oil prices will continue this rebound into the end of the year as the SPR releases that have put excess oil on the market come to a halt. The graph below, compiled from SP Global and Worldometer, tells a compelling story. This is a story of demand and under-investment.

Global Upstream Spending/Chart by author (SP Global)

Every year approximately 80 mm new people join the nearly 7.9 bn folks already here, all needing (but not always having) energy to power their lives. In six years from 2014 to 2020 spending on new upstream sources fell by 55%, while the world’s population rose by ~8%. The math doesn’t work.

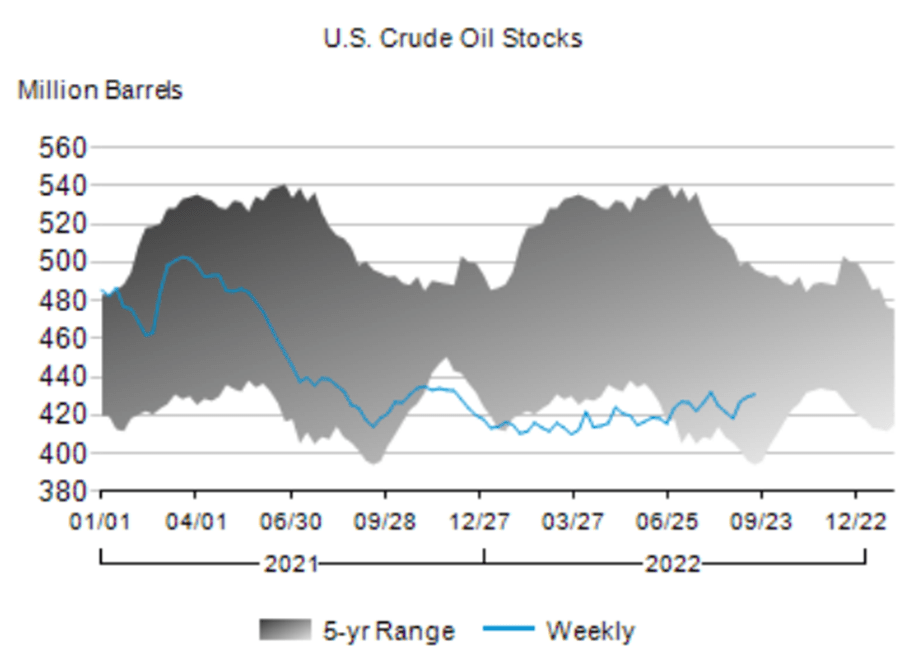

The oil market is undersupplied as the EIA graph below shows. Since March when the government announced the SPR releases to bring down domestic gas prices, inventories have risen about 15 mm barrels. If you back out the 172 mm barrels withdrawn from the SPR over this time, inventories would have shrunk to ~248 mm bbls. That may sound like a lot is left in storage, but in reality with our ~19 mm BOD habit, it’s a ~13-day supply. Less than two weeks.

EIA WPSR (EIA)

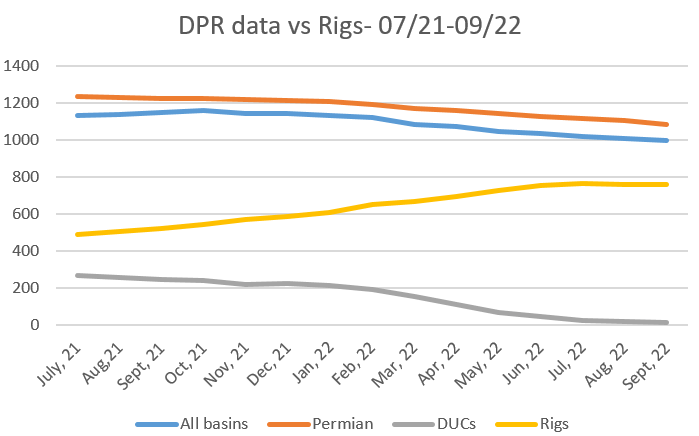

Not only are inventories being artificially inflated by SPR releases, the productivity of new wells as reported in the EIA-Drilling Productivity Report is on the decline. This is an admittedly simplistic measure as it just takes active rigs at a given point and divides into new well production as reported by various sources – usually state regulatory agencies. The fact the yardstick is done in fourth grade arithmetic without sophisticated modeling doesn’t mean it’s not instructive. It does reveal an undeniable trend in new well production. Across every key basin with the exception of the North Dakota and New Mexico basins, there’s a pronounced decline despite of steady growth in the rig count for most of this year.

EIA DPR/Chart by author (EIA DPR)

This is true regardless of the underlying reason, which I have postulated in the past could be due to exhaustion of premium drilling inventory. This has been documented several times recently in widely read publications that include the Wall Street Journal here and here.

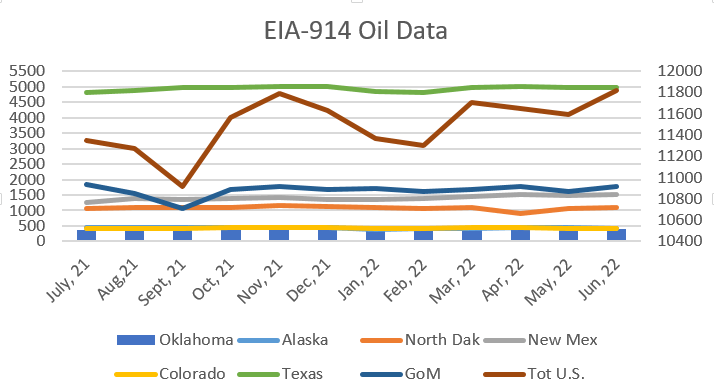

EIA-914/Chart by author (EIA)

The data from the DPR is confirmed by information compiled from the EIA 914-monthly report. Only in North Dakota and in the Gulf of Mexico-GoM do we see a gain from May to June. In the case of the GoM Murphy Oil’s, (NYSE:MUR) Kings Quay production contributed about 80K BOPD, and BP’s Herschel provided another 20K BOEPD, toward the 179K BOEPD shown for the month.

Higher drilling costs also are beginning to impact profitability as was noted in an even more recent WSJ article. What this means is that maintaining or increasing production will come under a sharper lens as margins compress and operator’s balance sheet priorities come into play. Almost without exception shale drillers have told us that their priorities are returning capital to shareholders through special dividends and share buybacks, paying down debt, and holding production to low single digit growth. If oil prices return to the $70s for any extended period, you can expect cuts in operating budgets which would show up in the rig count soon after.

The takeaway from this section is the likelihood that U.S. production is going to rise to 12.6 mm BOEPD in 2023 as the EIA suggests in this month’s edition of the STEO, is becoming increasingly remote. Current trends are heading in the other direction, and the catalysts for a reversal of course are just not present. The recent weakness in oil prices had producers sharpening their budgetary knives. Inflation is eating at their already tight budgets, and nature itself may intervene with poorer quality rock than was available in the past.

Is any help coming from OPEC+?

OPEC and its sometime collaborator when interests align (Russia) have fallen short of producing up to full quota levels by by a significant amount. Some reports have this shortfall at more than 3 mm BOPD at present. In fact the CEO of Aramco (ARMCO) made a widely read pronouncement earlier this month that the world was on the precipice of an energy shock of massive proportions.

“But when the global economy recovers, we can expect demand to rebound further, eliminating the little spare oil production capacity out there. And by the time the world wakes up to these blind spots, it may be too late to change course.”

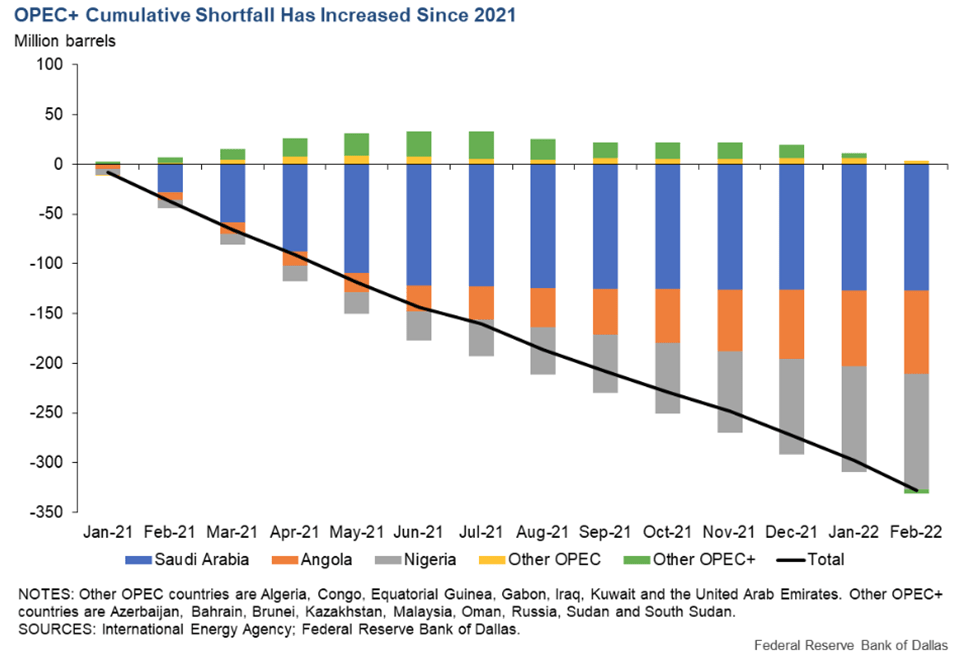

The Dallas Fed put out a report documenting the OPEC shortfall as well that points to key source of underperformance at the feet of none other than Saudi Arabia. It only runs through February of this year, but shows clearly the Kingdom of Saudi Arabia producing about 1.2 mm BOPD below quota.

Dallas Fed/Chart by author (Dallas Fed)

To put a cap on this discussion of whether the Kingdom can dig deep and come up with more oil when the world needs it, we have commentary from the defacto Saudi leader himself, Prince Mohammed bin Salmon, also known as MbS:

“The kingdom will do its part in this regard, as it announced an increase in its production capacity to 13 million barrels per day, after which the kingdom will not have any additional capacity to increase production,” he said in a wide-ranging speech.”

In his address the Prince noted that it would not be able to reach the 13 mm BOPD capacity level until 2027. This should knock on the head any notion that OPEC or its primary member, Saudi Arabia, can turn a valve and add significantly to world oil supplies any time soon.

Update from original article

In an update to this article, the cartel is meeting this week in Vienna with the expectation of announcing a production cut to support prices – and they did that … announcing a 2 million barrel a day cut. The notion of a million barrel a day reduction was previously making the rounds, or possibly a 2-mm BOPD cut, for reasons that include extending their inevitable decline. It may be more for show than substance, as we have noted they are already pumping over three million BOPD below their established quotas.

Your takeaway

We concluded there was nothing about the perfect storm of negative sentiments that impacted our base bullish case for oil, and were buying key companies during the period oil was crashing. We added to our large position in Devon Energy, (DVN), in the $55s, Marathon Oil, (MRO) in the $23s, APA Corp, (APA) in the $33s, and opened a new position in Suncor Energy, (SU) $28, on the operator side. In services we were buying Halliburton, (HAL) in the $25’s, Tetra Technologies, (TTI) at $3.50, Schlumberger, (SLB), at $35 and Liberty Energy, (LBRT) in the $12s. We would have bought others as well, but there is only so much money at any given moment. We are satisfied with what we were able to obtain.

We have recent articles on many of these companies.

Devon Energy: Big Game Hunting…

Tetra Technologies: There’s A SandStorm…

The OPEC led rally this week has us up 5% to 10% on these buys, and we think there’s more to come. The structural shortage that’s about to explode on the energy market is going to drive multiples for all of these companies higher as demands for energy increase around the world.

Investors also may wish to participate in oil futures directly through an ETF such as USO ETF (NYSEARCA:USO). This fund which tracks West Texas Intermediate-WTI, is still down ~25% from recent highs at $91.08, and should track higher with rising oil prices. It has ticked up modestly from the low $60s on Sept. 26 to its present level at $70.28. This is clearly tied to the OPEC+ rumors and will be confirmed or shot down (not something we expect) as early as today. Investors should read the prospectus on this fund prior to making an investment decisions.

The BNO ETF (NYSEARCA:BNO) tracks the performance of Brent, a grade produced in the North Sea, and is another way to play the anticipated rise in crude oil prices. At $29.32 it is still ~20% below recent highs of $36.38, providing some upside if the cartel follows through on its notion to curtail production with an eye to raising prices. Investors should read the prospectus on this fund before making any decisions about investing.

The hard truth is there just isn’t much more supply to be had for the reasons we have discussed. Some folks are just going to pay more for their energy needs. They may be the lucky ones. Some other folks are faced with doing without, and there is no easy cure for that condition.

What this means is that these companies and ETFs have further to run under the scenario that appears to be developing. Tight supplies domestically and production restraint abroad will push prices back above $100 per barrel, and we believe sustain them there well into next year. This is bullish for all the equities that derive their value from the price of WTI and Brent.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment