blackdovfx

Thesis

Guidewire Software, Inc. (NYSE:GWRE) is the leading provider of critical software systems to the P&C insurance market. GWRE has established one of the leading competitive positions, which allows it to lead the on-premise software integration and successfully transition into the leading provider of cloud solutions to the insurance carriers.

I like GWRE’s revenue mix shifting toward cloud (>50% annual recurring revenue or ARR) and estimate that GWRE could potentially more than double its existing revenue by migrating its existing customer base to the cloud. The process of GWRE becoming a successful cloud provider weighed on profitability in 2022 and will likely result in losses hitting a trough in 1H23E. The impact on profitability during the final stages of cloud platform formation makes current, and 2023E valuations look elevated compared to what I believe the long-term opportunity in this stock represents.

GWRE stock price YTD (Seeking Alpha)

Why am I bullish on GWRE?

Big and under-penetrated market

The P&C (Property & Casualty) segment of the insurance industry comprises c. 2,000 companies (20% of those insurance carriers control 80% of direct written premiums or DWP). The majority of core DWP opportunity remains untapped. A significant portion of the players in the industry is still running legacy mainframe systems that were put in place 30 or more years ago. These systems are now very costly to maintain, meaning that they very often inhibit topline growth and profitability.

Clear leader with proven scale

Guidewire, with its 520+ customers, is more than 2x the size of its closest competitor Duck Creek Technologies, Inc. (DCT), not only in terms of total revenue but also when comparing purely cloud-based ARR (annualized recurring revenue). GWRE is also the main provider being used by very large Tier 1 insurance carriers that account for almost half of P&C direct written premiums or DWP.

Demand coming down the pike

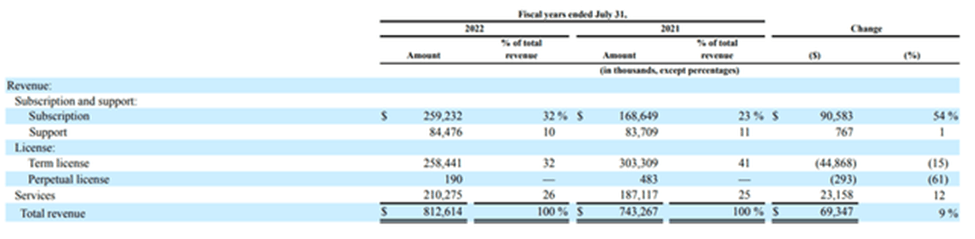

The biggest hurdle to the potential growth of insurance software vendors is the long cycles, as carriers still appear hesitant to switch away from systems that were installed more than 30 years ago (and have become core to operations) to completely new software solutions or cloud platforms. That said, I believe it will become increasingly easier to convince new and existing customers to move to the GWRE cloud platform now that they have 19 customers already completely moved over and 60 customers in the process of migration to the cloud platform. These increased traction activities are reflected in accelerating revenue growth of subscription revenue: 54% YoY growth in FY22A vs. 41% YoY growth in FY21A.

GWRE revenue breakdown (Company Filing)

Recurring revenues and high customer stickiness

Once customers move to the GWRE platform, they tend to remain on it for many years, if not decades (the average contract is signed for five years with multiple renewal options). This is especially relevant for Tier 1 carriers: for them, the systems are essential/core to the company, meaning that the required data migration, as well as the workflow changes necessary, make it prohibitive for carriers to initiate such changes on a regular basis. The high share of recurring revenue, as well as contracts that have already been signed by GWRE, give the company high visibility into a given fiscal year, translating into a highly solid and visible business model.

Financial Outlook and Valuation

Topline growth fueled by 30% Subscription CAGR

GWRE’s consolidated revenue is made up of three segments with distinct growth profiles: Subscription and Support (42% of F22 revenue), License (32%), and Services (26%). I believe most of GWRE’s legacy segments are likely to deliver low or negative growth over the midterm, while the Subscription and Support segment is likely to continue to expand at a high double-digit CAGR from FY2022-FY2025E. Subscription, which represents 75%+ of these revenues, has a hearty 30% three-year CAGR profile. The rest of the segment is Support, with a negative growth profile. The other two segments – License and Services – are likely to have low to negative growth profiles. I expect GWRE to prioritize its cloud SaaS operation, which is represented in the Subscription portion of the business, and thus the other businesses are likely to shrink as a portion of total revenues over time.

Improving GMs where it matters most

I forecast the gross margins of the Subscription and Support as well as Services businesses to increase between FY2022 and FY2025E. The Subscription operation should improve as more clients are successfully transitioned to Cloud. GWRE was relatively late to the party as far as SaaS solutions go, having signed its first customers only a few years ago. I think the gross margins should climb quickly in the coming years as the cloud operation continues to gain scale. I also believe that Services should return to profitable, mid-teens levels by the middle of FY2023E. As a result, I anticipate GM improvement from 2022 to 2025.

Valuation and Target Price

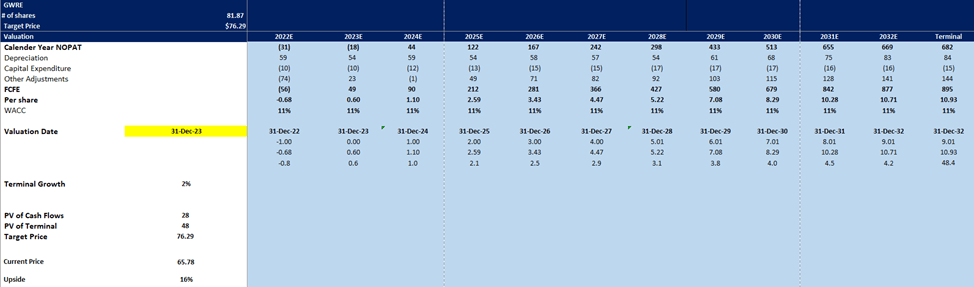

I do not foresee major changes to operating expenses as a percentage of revenue and expect R&D to remain around 25% of consolidated revenue, sales & marketing to float in the mid-teens, and G&A to fluctuate in the low teens. I have estimated a tremendous lift in the operating income margin from -5% to 10% (FY22-FY25). The lift is mostly due to the GPM rising from 49% to 60% over the same time period. My December 2023 price target of $76.29/share is based on my 10-year DCF analysis (applying c. 11% WACC and 2% terminal growth rate). I keep a buy rating on the shares since I forecast a 16% upside in the stock from current levels. Below is the screenshot of my DCF model for GWRE.

GWRE DCF model (my estimates)

Risk to Rating

Deployment execution

I see a hypothetical risk of GWRE potentially missing on executing and deploying client systems that could cause its customers financial harm. Such a scenario would likely elongate already very long sales cycles as customers would grow increasingly nervous about completely rebuilding core systems (that may not be perfect but at least still work). It is to be noted that GWRE’s deployment track record is one of the key reasons customers tend to choose Guidewire over other competitors.

Expensive transition to cloud

GWRE still has a lot of on-prem customers, meaning that with their focus on cloud, they have divided their insurance client base into “before” and “after.” Such a strategy is expensive, meaning the elevated investment levels (R&D going toward multiple solutions) could hit revenue growth, and the hit to profitability may persist longer than expected.

Conclusion

Insurance is a critical component of the world economy, and I see a huge opportunity for vendors providing software (transactional systems of record) to insurance enterprises, allowing them to administer policies and manage claims/billing. GWRE is exposed to the global P&C insurance, which is ubiquitous, in most cases mandatory, and therefore considered “recession-proof”. I favor GWRE in the space, given its more pronounced cloud market share gains, significant scale, and greater stock liquidity. Moreover, I like GWRE’s revenue mix shifting toward cloud (>50% annual recurring revenue or ARR), which should lead to rising top-line growth acceleration. My December target price of $76.29 implies an upside of 16% from current levels.

Be the first to comment