Mizina/iStock via Getty Images

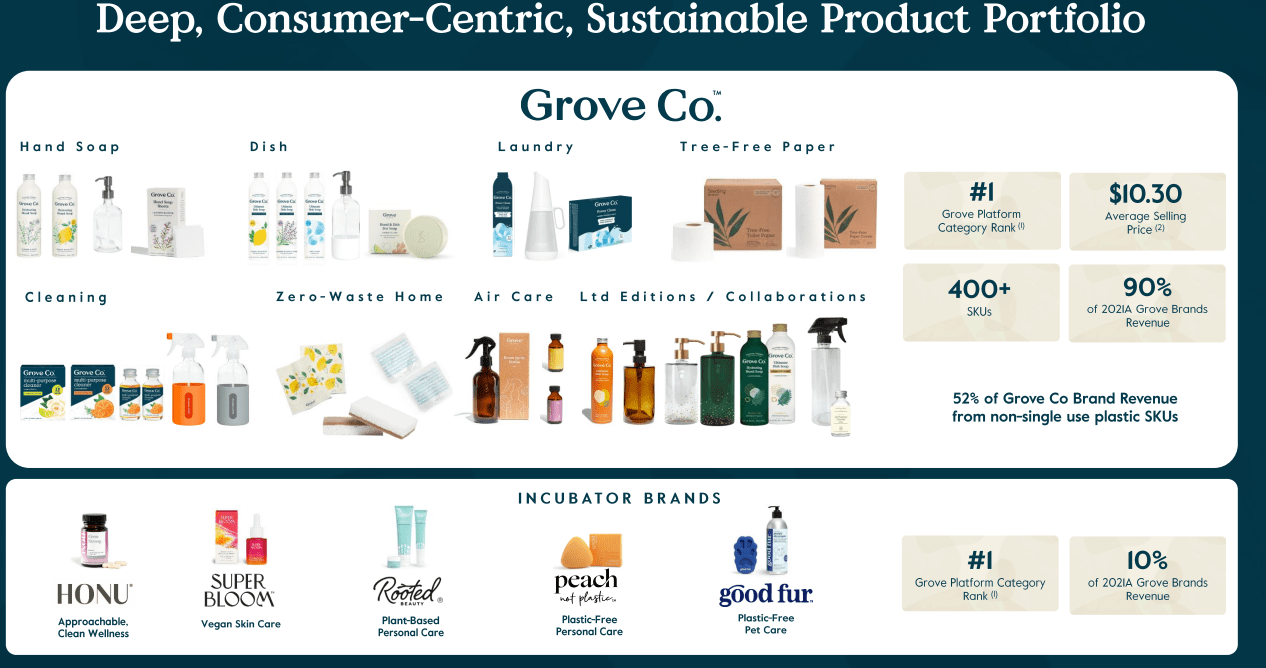

Grove Collaborative Holdings Inc (NYSE:GROV) is a consumer products company and online retailer focusing on environmentally sustainable, home and personal care (HPC) brands. If you’re looking for vegan and plastic-free hand soap, cleaning supplies, or even skin-care items; Grove offers over 400 SKUs through an omnichannel approach that includes partnerships with major retailers like Target Corp (TGT).

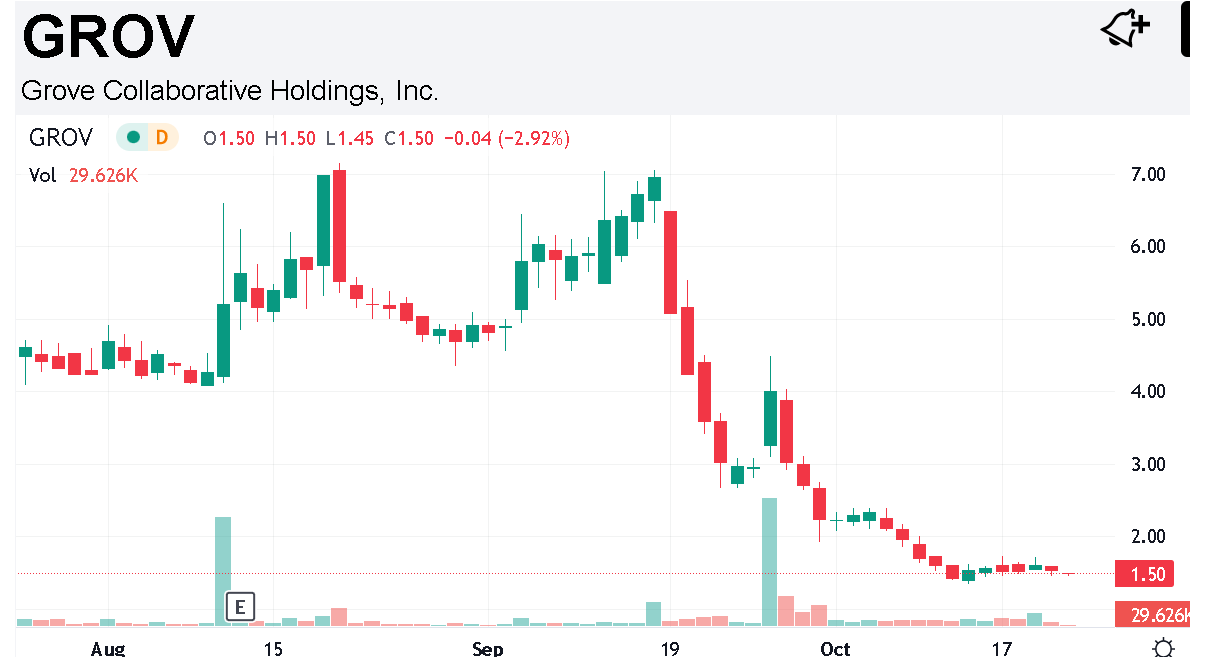

On the other hand, this segment is facing significant challenges considering macro headwinds like record inflation and rising interest rates pressuring consumer spending. Shares of GROV are down more than 60% just over the past month highlighting the extreme volatility and poor sentiment based on recurring losses and negative cash flows as it attempts to scale.

Still, there is a case to be made that the stock could represent a compelling turnaround opportunity with a view that the selloff is overextended. An ongoing retail expansion placing Grove products in front of more consumers is likely to drive a growth runway. GROV remains speculative, but has upside potential over the long run.

source: company IR

GROV Key Metrics

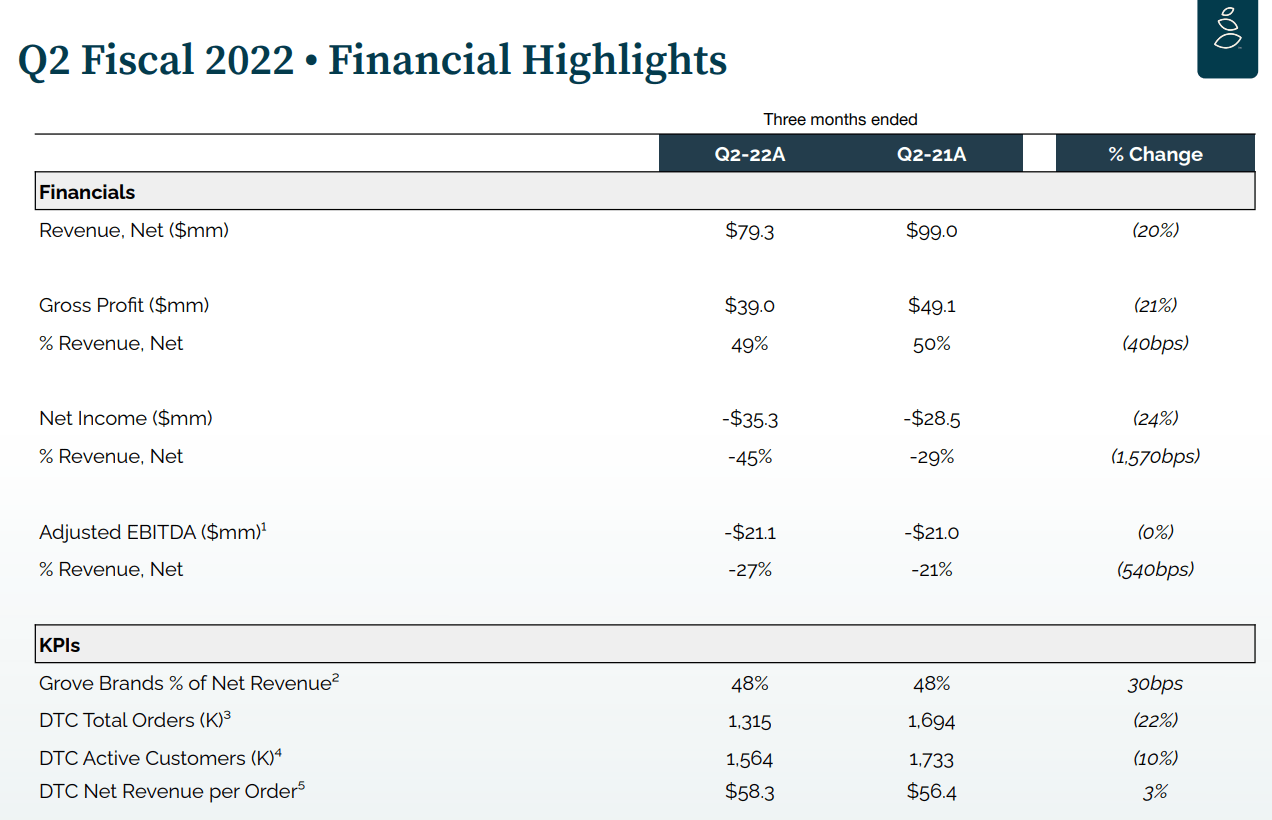

The company last reported its Q2 earnings back in August and the headline numbers weren’t pretty. Revenue of $79.3 million declined by -20% year-over-year while the gross margin also fell and the net loss at -$35.3 million widened from Q2 2021. Total orders and total active customers operating metrics are also down by double digits.

The context considers that the period last year was particularly strong for consumer spending leaving a tough comparable following the broader shift in e-commerce industry trends. Management explains that the company reduced advertising spending to acquire new customers which at least helped contain the adjusted EBITDA loss, flat at -$21 million from last year.

source: company IR

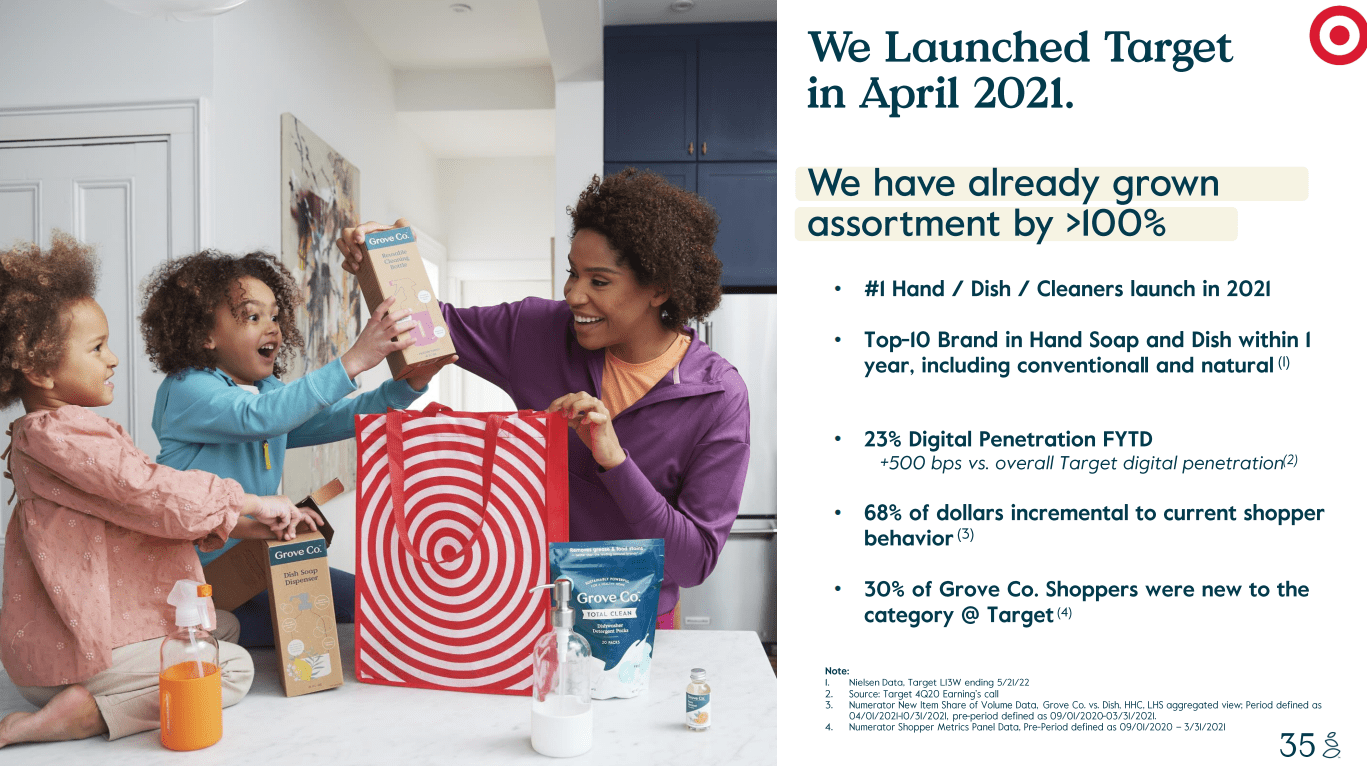

Recognizing otherwise few silver linings, one encouraging point has been the reception of Grove brands by consumers at other retailers. We mentioned Target where Grove launched in Q2 2021. The effort has helped raise awareness of the brand and line of products which is now the blueprint for the company going forward.

source: company IR

Developments in recent months include new announcements of an expansion into retailers like CVS Health Corp (CVS), and Kohl’s Corp (KSS) along with privately-held regional pharmacies and grocery chains like “Giant Eagle”, “Meijer”, “Harris Teeter”, and “H-E-B Stores”. The latest update is that Grove Brand products are now found in more than 4,000 retail stores.

An important point here is that the Grove website currently features products from other manufacturers representing approximately 52% of net revenue. The expectation is that Grove Brands’ composition climbs within its total net revenue over time which should support higher margins in line with a strategic priority of improving profitability.

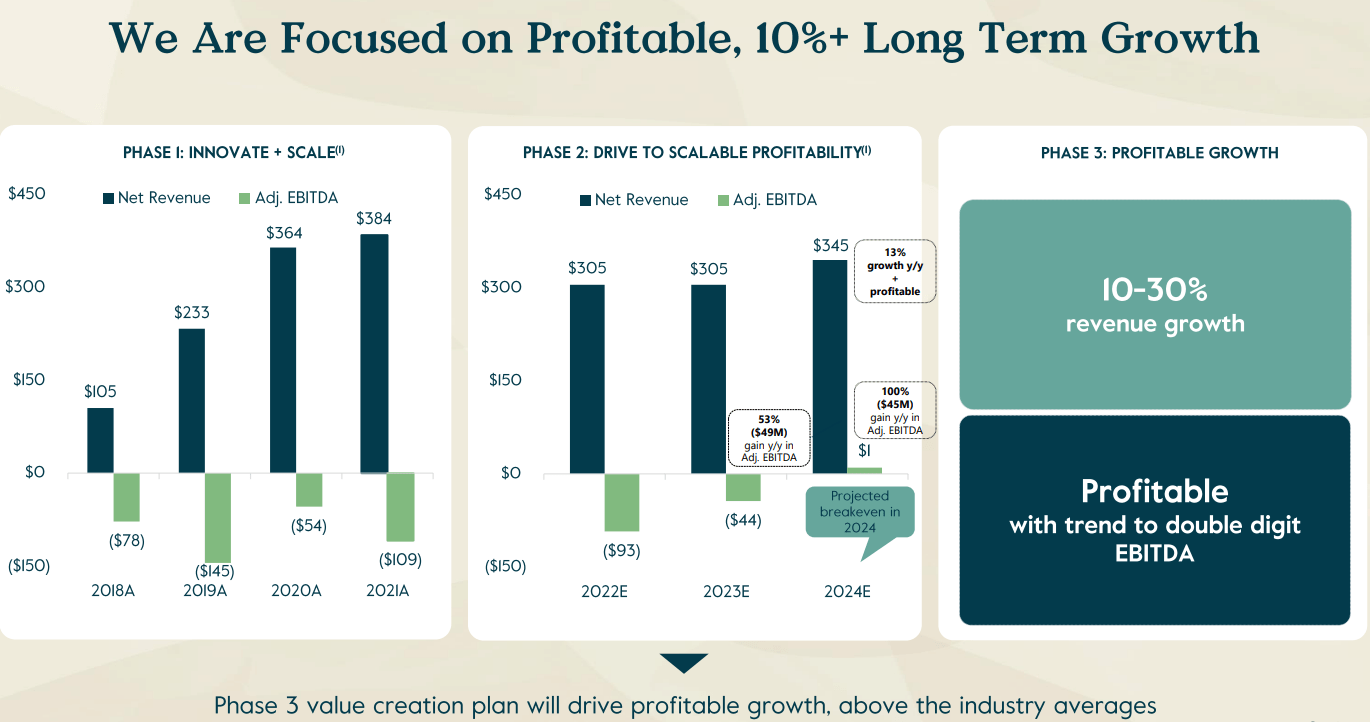

In terms of guidance, the expectation is for full-year 2022 net revenue in a range between $302.5 to $312.5 million which is notably up from a prior $305 million midpoint target. This compares to $233 million in 2019 as a pre-pandemic benchmark, although still down from a record $384 million in 2021.

Finally, the company ended the quarter with $133 million in cash against $44 million in long-term debt. Keep in mind that GROV became publicly traded in June following the completion of a SPAC merger. While liquidity appears stable over the near term, additional equity issuances will likely be required over the next few years considering its current cash bleed and negative earnings.

What’s next for GROV?

We sense that the company has largely been a victim of the poor macro backdrop that has not cooperated. The “premium” positioning of environmentally conscious and plastic-free products becomes a hard sell when consumers have seen their budgets squeezed in nearly every other spending category.

Seeking Alpha

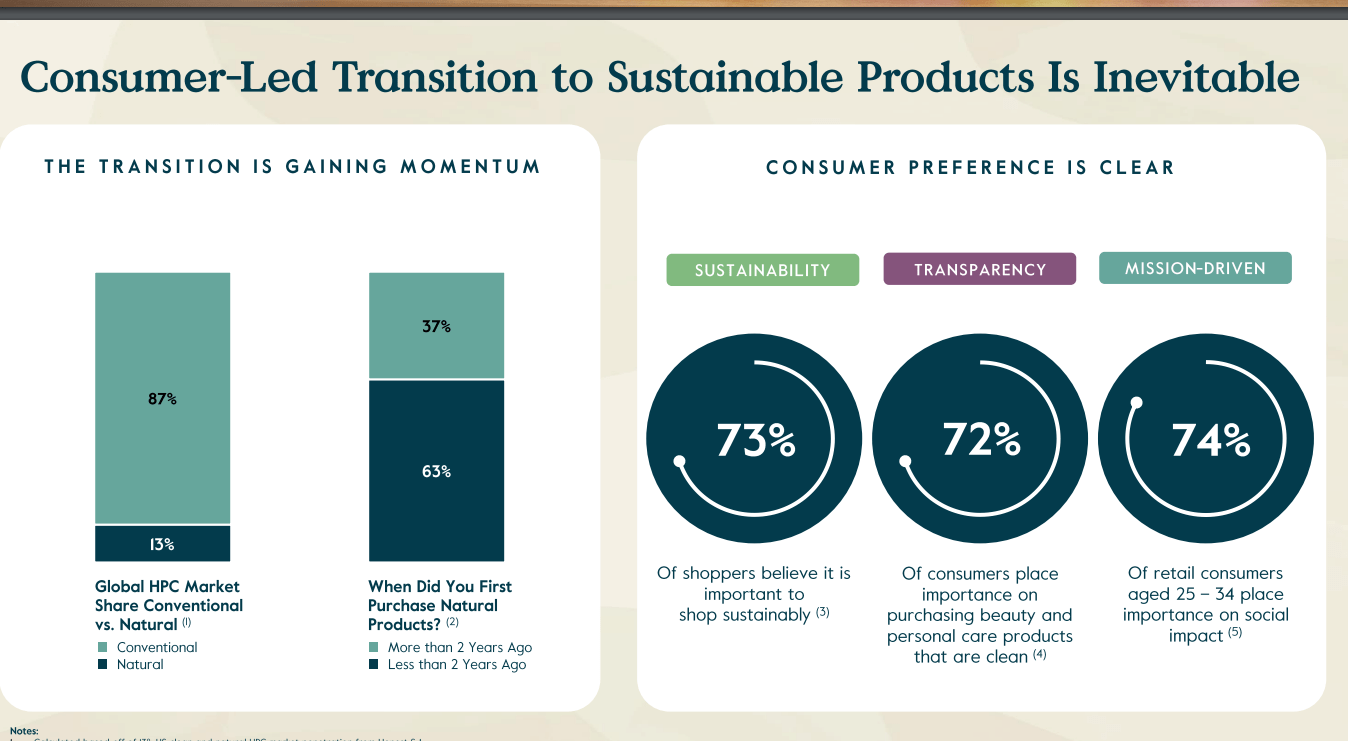

At the same time, the bullish case is simply that Grove Brand products have a long-term future and can gain market share against competitors. While most consumer staples giants offer a line of “natural” home and personal care items, the idea here is that Grove represents a pure play on the category. Data suggests, that this natural HPC has gained market share versus conventional products as more consumers seek potentially healthier choices.

source: company IR

As the products become available in more and more channels including through retail expansion, more consumers can be converted into lifetime customers. This goes back to the old business adage “if you build it, they will come”. In this case, Grove is getting its products out there and the sales will follow.

According to management, the outlook is for the revenue trends to stabilize by next year and return to 10% growth by 2024. Over the period, the goal is for adjusted EBITDA to turn positive and accelerate higher going forward. The trend can be driven by a declining level of SG&A as a percentage of revenue, while the advertising needs also slow. The shift of the company’s business towards company-owned brands in its online direct-to-consumer portal will add to margins. Ultimately, we believe the plan can work.

source: company IR

Final Thoughts

Grove Collaborative Holdings’ “show me” story where the first step will be for the company to provide some evidence that operating and financial trends are stabilizing. Getting into 2023, more favorable sales comps could allow the narrative to turn into a recovery that is building momentum.

Assuming revenue can reach that full-year 2024 forecast of $345 million, the possibility of positive EBITDA that year with double-digit top-line growth would make the stock appear cheap trading under 1x sales considering the current market cap of around $240 million.

We rate shares as a hold, implying a neutral view in the near term, but see risks tilted to the upside at least for a technical bounce. For existing shareholders underwater, it’s probably too late to sell and our call would be to add into the position on any sign of strength to lower the cost basis.

For now, the expectation is for shares to remain volatile with the upcoming Q3 earnings report as the next catalyst to watch. While a date has not yet been confirmed, the report will likely come in November with the sales trend and margin levels as a key monitoring point. In terms of risks, weaker-than-expected results, or a reset lower to forwarding guidance could open the door for more downside in shares.

Be the first to comment