Andrii Yalanskyi/iStock via Getty Images

The following segment was excerpted from this fund letter.

Griffon Corp. (NYSE:GFF)

GFF remains an outsized long position at ~20% of the Fund.

Their consumer and professional products (tools) segment, CPP, continues to disappoint this year as retailers became over inventoried, there was generally poor weather for the peak gardening season, and input cost went through the roof. We assume only a ~$950M valuation for CPP in a sale – a 50% discount to the cumulative combined values paid for the various businesses since 2010.

More importantly, GFF’s more valuable garage door segment continues to surprise to the upside in a major way. It is still growing 47% and 2022’s full year EBITDA came in >100% higher than expectations at the start of the year. There has been no demand collapse.

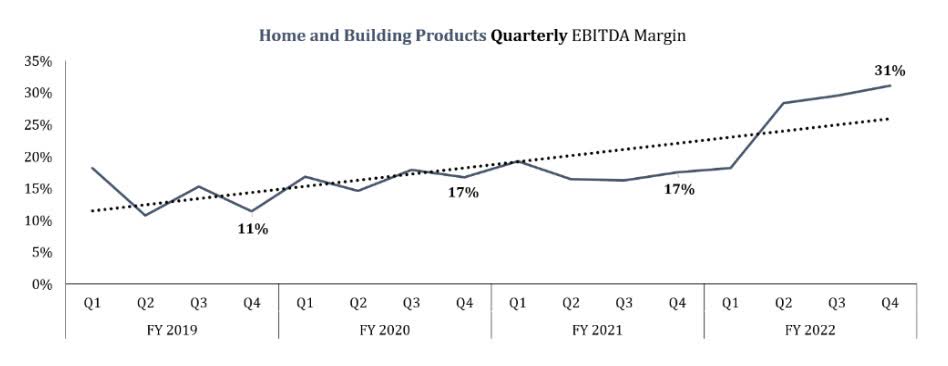

And contrary to intense skepticism and pushback that we heard all year long, at 31%, HBP’s EBITDA margins continue to tick higher—and that is before the benefits of lower steel prices are felt. With their initial guidance for 2023 for a “modest EBITDA decline” implying recent HBP EBITDA gains are relatively sustainable, we believe potential acquirers’ fears should be assuaged, thus significantly raising the probability of a favorable valuation in a buyout.

In conjunction with its ongoing strategic review, the company pushed its director nomination window back by a month. The new director nomination deadline is now December 30th, a date we are highly cognizant of as the year winds down and we eagerly monitor developments at Griffon.

With the company continuing to forego earnings calls and now calling out executive retention bonuses for 2023, we believe many signs point to GFF remaining on track to sell both operating segments separately within a matter of weeks.

Our Base Case price target is in the range of $50 in a break-up scenario, which is derived from using 11-12x EBITDA for HBP ($370M of 2023 EBITDA) and 6-7x depressed CPP EBITDA of $130M.

Thanks to the strong 2023 guidance and a hefty mid-teens FCF yield at the current stock price, we believe the fundamental downside is limited even assuming there is no imminent sale.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment