400tmax/iStock Unreleased via Getty Images

Investment Thesis

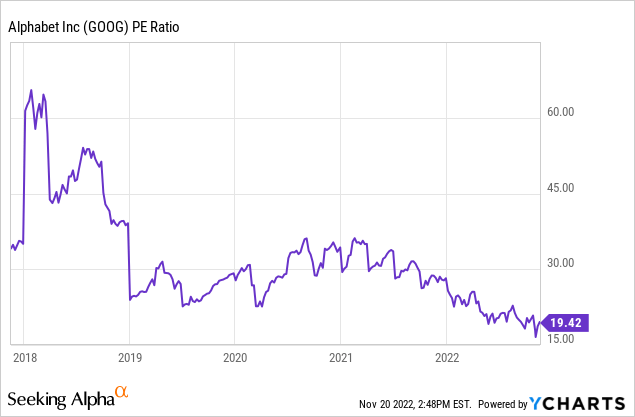

Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) has lost almost a third of its value YTD and the stock price keeps dipping. However, the fact that the company is trading at the cheapest valuation based on P/E since 2018 has made a lot of investors wonder if it is now time to start a position in the company.

Whenever investors hear about mega-cap companies like Microsoft (MSFT) or Google, for example, they tend to believe that it is impossible for these companies to yield 15%-20% on their investment. But what if in the case of Google it is?

Keep reading to find out how…

Google’s Secret Weapons

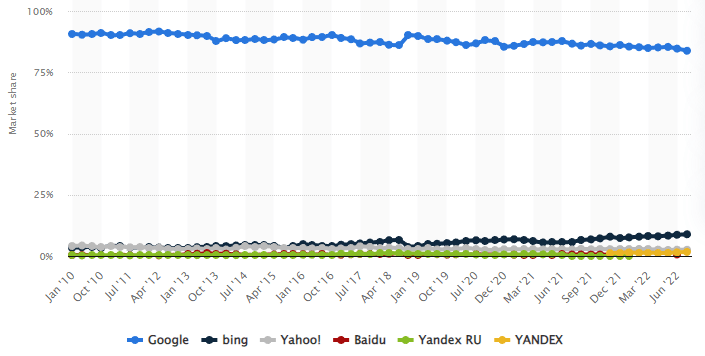

Google dominates the search engine market with a market share of more than 83%, and Bing is its closest rival with a market share of roughly 8%.

statista.com

Due to the fact that Google already holds a dominant position in this sector, there is little room for the company to grow and as a result, it will not be able to rapidly raise its revenue based just on the search engine. This implies that the business must find alternative strategies to maintain double-digit top-line revenue growth. Increasing the volume of individuals conducting online searches is one approach, but in major areas like America or Europe, Google has essentially reached every home, and in growing markets like India, the average revenue per user is extremely low. Consequently, this is not really a choice. So how will the company retain such a high growth rate?

Google Cloud

blog.google

Industry forecasts predict that the cloud sector will expand at a rate of over 16% through 2030. When the industry itself is growing at such a rapid pace, it is feasible for many individual players in this industry to grow their revenue by at least 40%. As a matter of fact, this is what is happening with Microsoft’s Azure and something similar is happening with Google Cloud as well. So, although Google Cloud only makes up less than 10% of the whole revenue, it contributes more as time passes. The only problem is that unlike Amazon’s (AMZN) AWS and Azure, this is not a profitable business. So although the overall revenue is growing at a decent pace, as businesses inside Google, like Google Cloud, are growing at 40%-50%; at the end of the day, when it comes to profitability, these businesses do not help with the margins as they are still losing money.

On the other hand, Google Cloud’s lack of profitability could be an opportunity for investors. Although this segment is currently unprofitable, as time goes on it comes closer to breaking even and it is projected to become profitable next year. Also, I believe that it is reasonable to expect that once Google Cloud achieves profitability, it can support operating margins of at least 10% as AWS has operating margins of 30%. This would drive the overall margins of the company higher leading to more profits and therefore higher valuations.

YouTube Premium

youtube.com![]()

YouTube Premium is a really underestimated growth area within Google. YouTube Premium is basically YouTube but without the ads, and the opportunity to download videos. Similar to Spotify (SPOT), YouTube Premium also includes YouTube Music Premium, which can be purchased separately. This feature enables users to listen to music without interruptions. The fascinating thing about YouTube Premium is that the service’s user base has been expanding quite quickly. Although there isn’t yet any detailed reporting of this in the annual report, the firm has been updating investors on this development in blog posts.

According to this, the service last year had 50 million subscribers and it now has 80 million. This astounding growth rate of 60% indicated by this increase in users is just the beginning, though. The reason that I believe this service could be big for the company is that it opens ways for the company to expand to new markets like the one that Spotify operates in and although competition is high there, I am sure that YouTube premium will manage to get a piece of the pie.

Concerns

Although Google is a great company that has proven its value throughout the years, there are some risks that come with buying this stock.

Monopoly

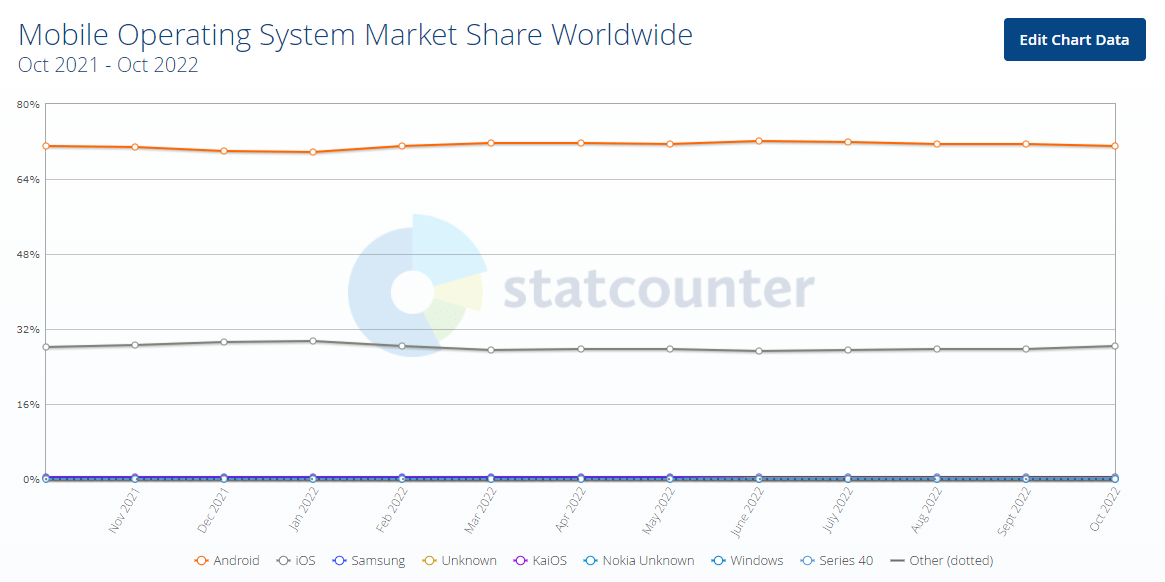

Given that it controls more than 83% of the search engine market, monopoly seems to be a clear problem for the business. The issue with Google is that it also owns Android, which, with more than 70% of the market share, is also very nearly a monopoly.

statcounter.com

The good news is that, according to what the corporation claims, nobody is compelled to use its search engine or YouTube. People have other options, but they deliberately choose Google and this helps to reduce the company’s reputation as a monopoly. However, the risk of monopoly still exists, and Google has received fines for exploiting monopoly multiple times in the past.

Capital Allocation

Google right now generates tons of free cash flow. The problem is that the companies are now generating billions of free cash flow and the reinvestment possibilities are limited. So what does Google do with that money?

I consider share buybacks to be a great choice as the company is currently undervalued and this way, the company does not only reward its investors by giving them a bigger portion of the company but also invests its money in undervalued assets.

By other bets, the company refers to acquisitions of smaller companies that it makes to buy its growth. The issue is that in this area, the company losses billions of dollars every single quarter, and when these losses are added to the overall operating income of the company, it goes down. There is however hope that this segment will someday become profitable because in recent quarters it has begun to become more efficient. Although it still burns cash, it does so at reduced rates. If this pattern continues, the company’s profitability will grow faster than its revenue since the losses from this section will be reduced.

Conclusion

Summing up, although some risks come with buying Google, I believe that they are more than factored in the price of the stock. If/when the investments that the company makes in the Google Cloud and YouTube premium finally pay off, and the other bets segment stops burning cash, the margins are most likely going to increase and therefore the profits are going to be higher, driving the company to new all-time high prices in my view.

Bearing in mind everything mentioned above, I consider the fact to buy such a fundamentally stable and high-growth company like Google at this valuation to be an opportunity of a lifetime and I rate the stock as a STRONG BUY.

Be the first to comment