pcess609

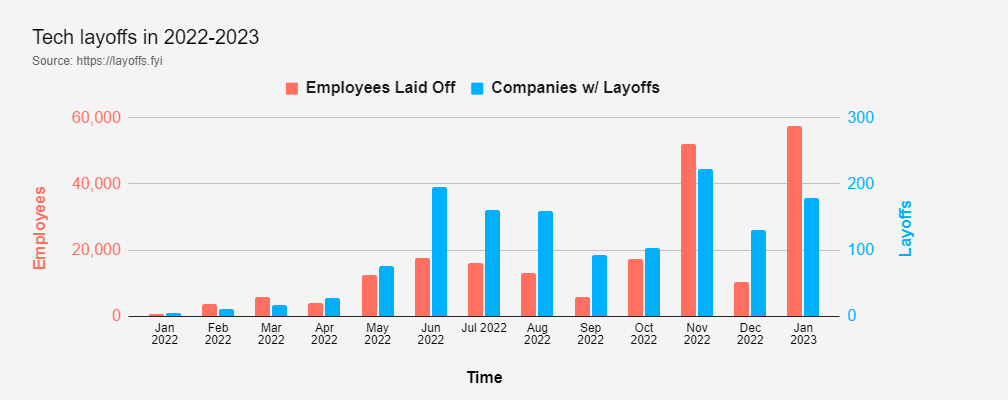

Tech layoffs have accelerated

Over the last months, layoffs in Tech companies have been on an uptrend. Now the big players are joining in and after just 24 days, January already saw record-breaking layoff numbers. According to Layoffs.fyi, the total amount of tech layoffs in 2022 was 158,951 people. Meanwhile, January already saw 56,570 layoffs, 1/3 of the entire 2022 layoffs.

Tech Layoffs are accelerating (Layoffs.fyi)

This is primarily due to the big tech companies:

- Meta Platforms (META) was the first to announce 11,000 job layoffs last November, about 13% of its workforce.

- It took a while until Amazon (AMZN) announced 18,000 job layoffs in January, followed by Microsoft (MSFT) with 10,000 layoffs, less than 5% of employees.

- Smaller companies like Spotify (SPOT) also joined with a 6% layoff.

- Now Google also joined last Friday with 12,000 layoffs representing 6% of staff.

TCI Fund Management is not done!

Last November, TCI Fund Management released an open activist letter to Google’s CEO Sundar Pichai. I covered the letter in detail in my article, but let me briefly summarize:

TCI is a value-oriented global fund with a long-term investment horizon and a concentrated portfolio of just 9/10 stocks (they own Alphabet A and C shares, so it’s up to interpretation how many stocks they own). Since Q2 2019, Alphabet accounted for more than 20% of the portfolio, showing a deep conviction in the company. The letter addresses three key points: Cost cutting, EBIT target and management compensation and increased buybacks.

Last Friday, the same day Alphabet laid off 12,000 people, TCI released a second letter. The new letter addressed the first two points. Let’s go over its details.

On Alphabet’s cost basis

In the letter, Christopher Hohn of TCI (their total investment in Alphabet is worth around $6 billion) mentions a recent dialogue concerning Alphabet’s cost base and that he’s encouraged to see the actions taken to right-size it. He is talking about the 12,000 people layoff mentioned above.

In the following paragraph, he said that it is not enough, though, with Alphabet’s headcount more than doubling over the last five years. In the first three quarters of 2022, the company added 30,000 employees, significantly more than the 12,000 people laid off. Hohn proposes increasing the layoffs to 20% to reduce the headcount to 150,000 employees. The last data point we have (Q3 22) shows 186,780 employees. Let’s take a look at what this means for the bottom line:

| Q3 reported headcount (186,780) | 12,000 layoffs | 20% layoffs (37,356) | |

|---|---|---|---|

| Cost in Million | $55,265 | $51,714 | $44,212 |

| Average Employee cost | $295,884 | $295,884 | $295,884 |

| Savings in Millions | $0 | $3,551 | $11,053 |

| Free Cash flow in Millions | $62,540 | $66,091 |

$73,593 |

| EV/FCF yield | 5,5% | 5,9% |

6,5% |

Of course, we must remember that layoffs always have an upfront cost component associated with them, so the Q1 earnings report should include a few billion in layoff-related costs. Alphabet pays its employees:

- Minimum 60 additional days of pay

- 16 weeks of salary + accelerated GSU vesting, plus two weeks for every year at Google

- 2022 Bonuses

- Six months of healthcare, job placement services and immigration support

From a human perspective, layoffs are always a sad event, especially at this scale, but Google grew its spending too recklessly, so it is an inevitable step. The proposed 20% cut seems high, but I believe it could be realistic, even though I don’t think Alphabet will pull through with it.

On Alphabet’s compensation structure

The second part of the letter addresses the general compensation structure, which was already discussed in the first letter. As mentioned above, Alphabet has an exceptionally high median compensation of $295,884 (this includes salaries and bonuses). This is significantly higher than the median compensation for the Top 20 technology companies, which stands at $117,055, representing a 150% higher cost base per employee. Even compared to Microsoft, it is 67% higher. In the past, Alphabet justified that it had to acquire and retain the best talent. TCI now argues that competition has fallen significantly in the technology industry for employees. This makes sense with interest rates rising and money becoming more expensive; many incumbents can’t afford anymore to pay excessive wages. Alphabet should leverage this and try to reduce its cost base. This is easily said but not easily done. Straight-up slashing salaries is probably hard to do, so the best way I see to do this is by reigning in stock-based compensation (SBC). In my opinion, Google is one of the worst offenders for stock-based compensation in the market, with total SBC growing from $7.9 billion in 2017 to $18.4 billion in the last 12 months. Let’s see how this could impact the cost base. For this, I’d assume that SBC accounts for 1/3 of the average compensation(Total SBC/Employee count leaves us at $98,511, around 1/3 of $295,884). Let’s now see how different reductions in SBC per employee change the bottom line (all calculations done with the proposed 20% headcount reduction).

| SBC -10% | SBC -25% | SBC -50% | |

|---|---|---|---|

| Average SBC/Employee | $98,511 | $98,511 | $98,511 |

| Average Employee cost | $295,884 | $295,884 | $295,884 |

| Total Costs in Millions | $42,740 | $40,532 |

$36,852 |

| Total Savings in Millions | $1,473 | $3,680 | $7,36 |

| Free Cash flow in Millions | $75,066 | $77,274 |

$80,954 |

| EV/FCF yield | 6,7% | 6,9% |

7,2% |

We can see that this would drive significantly, bringing the total amount of savings in the best-case scenario (20% layoffs + 50% SBC reduction) to $18.413 billion. Even if we cut the pay by that much, the median compensation at Alphabet would still be significantly over all competitors, so there is lots of fat to trim potentially. Remember that I did not adjust the FCF for SBC in these examples.

What does it mean for Google’s future?

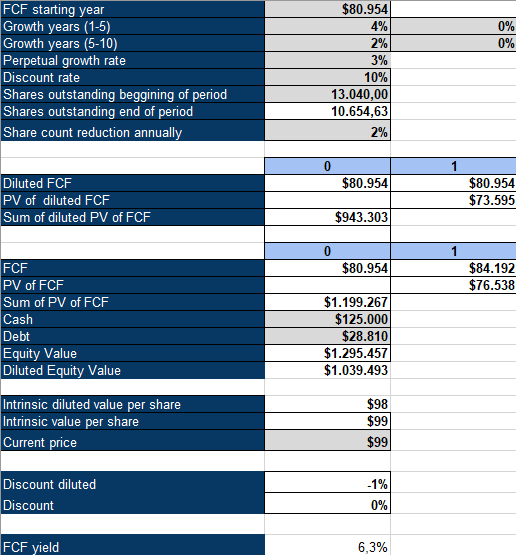

TCI does bring up some valid points in its second letter and although I don’t think it is realistic for Google to cut 20% of staff, I am sure the activist investor will drive further discipline. Below I adjusted my inverse DCF analysis and used the best-case scenario FCF of $80.95 billion. Under those assumptions and assuming that FCF is used for buybacks (2% annual shares outstanding reduction), the market would assume no growth for Alphabet to justify the current share price. Alphabet remains a buy.

Google Inverse DCF (Authors Model)

Be the first to comment