ipopba

Investment Thesis

Ames National Bank ( ATLO) is the parent company for six small community banks in Iowa. Since its incorporation in 1975, it has assumed the role of the acquirer in a consolidating industry, amalgamating its six subsidy banks throughout the years, with the latest being Iowa State Savings Bank in 2019.

ATLO) is the parent company for six small community banks in Iowa. Since its incorporation in 1975, it has assumed the role of the acquirer in a consolidating industry, amalgamating its six subsidy banks throughout the years, with the latest being Iowa State Savings Bank in 2019.

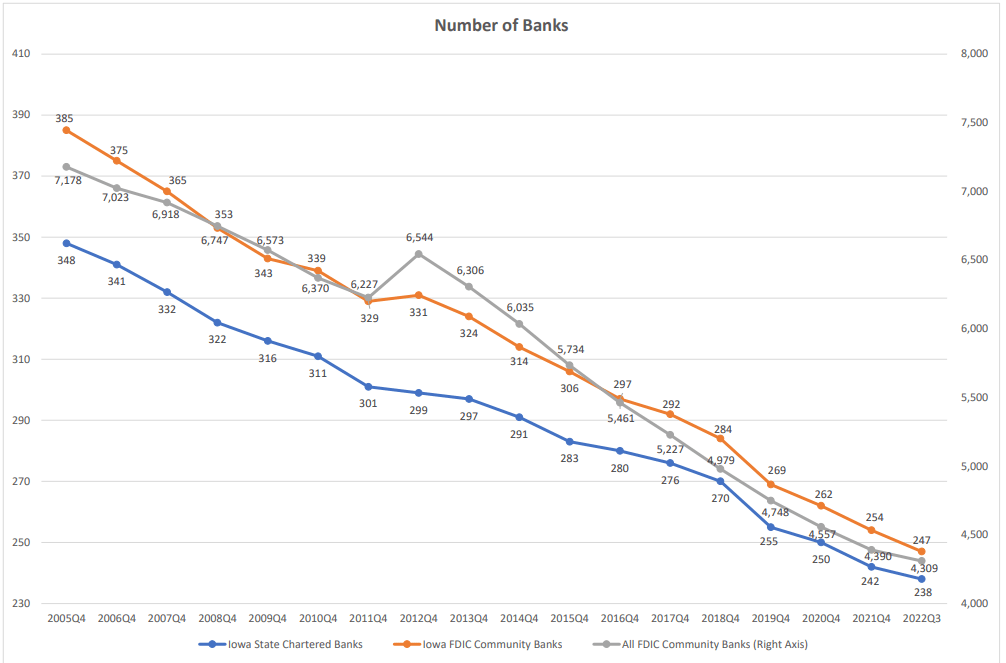

Number of Banks (Iowa Division Of Banking)

The decline in the number of Banking institutions in the corn belt state shows that the consolidation phase of the industry’s life cycle is in full swing. What does that mean to ATLO and its shareholders? It indicates that the organic growth phase has passed, which is why ATLO and the entire community banking industry are often overlooked. From the pace of consolidation, one can also conclude the existence of some form of synergies and economies of scale. But if that is true, why do community banks still exist? Community banks leverage their small size to forge personalized customer service experiences with simplified banking services that meet their client base needs, who are primarily small and medium enterprises. This gives it an edge over big banks with a more complex (and sometimes confusing) product mix. In its mission statement, ATLO states:

One major goal in developing the Banks’ product mix is to keep the product offerings as simple as possible, both in terms of the number of products and the features and benefits of the individual services. ATLO 2021 Annual Report

This simple service offering means less hassle for already busy small and medium business enterprise “SME” owners. Beyond the absence of hidden banking fees, annoying cross-selling sales calls, and complex product offerings, community banks compete on convenience, with branches close to the communities they serve. This allowed ATLO to hold a leading market position in two out of the eight counties it operates in, Story and Hancock, winning against 53 other banking institutions. Below is a table showing ATLO’s subsidy banks’ market share as a percentage of total deposits in Iowa, according to official data from the Summary of Deposits Survey by the FDIC.

| Deposits ($ 000s) | Market Share | |

| First National Bank, Ames, Iowa | $ 978,988 | 0.81% |

| Reliance State Bank | $ 254,500 | 0.21% |

| Iowa State Savings Bank | $ 234,496 | 0.19% |

| State Bank & Trust Co. | $ 204,975 | 0.17% |

| United Bank and Trust Company | $ 193,917 | 0.16% |

| Boone Bank & Trust Co | $ 145,968 | 0.12% |

| Ames National Corp | $ 2,012,844 | 1.66% |

ATLO has a very simple business model that is geared toward generating high returns on equity and consistently profitable operations. The company is easy to understand, making it ideal for retail investors, but more importantly, this makes its results more predictable and less volatile than larger peers, especially those exposed to the capital markets. One example of these dynamics is the fact that ATLO was able to maintain its profitability throughout the Great Recession while receiving no support from the government. This is in stark contrast to other banking firms in the country that were struggling to survive because of losses incurred through toxic securities and other complex financial instruments.

The downside to this conservative banking approach is slow organic growth and limited opportunities for above-average capital returns. Nonetheless, its stable operations, solid balance sheet, and dividend yield make it an ideal stock for retirees and income investors seeking both an adequate income stream and capital preservation.

Revenue trends

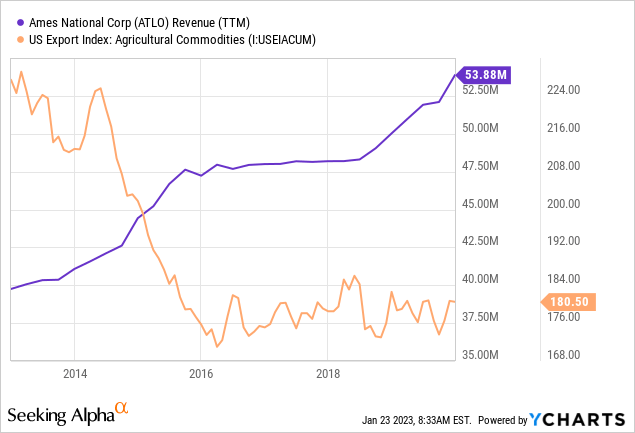

Iowa is known for its fertile grounds that fostered a thriving agriculture industry that remain a key driver of the local economy. However, it is a mistake to limit one’s view of the economy to just farm products since manufacturing accounts for nearly a third of the state’s gross domestic product. I started with these facts to highlight a common misconception tying ATLO’s economic success with agricultural commodity prices.

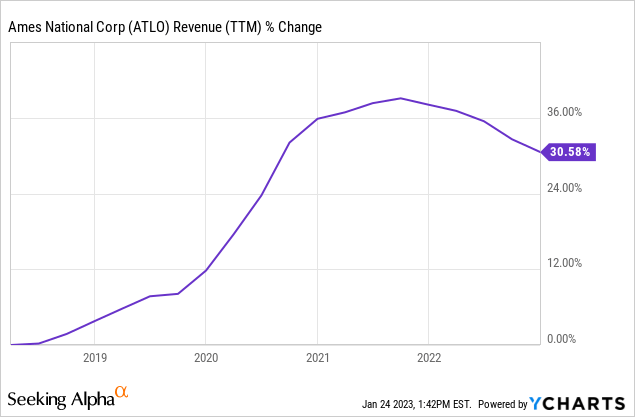

The above chart shows that ATLO’s revenue has a limited direct correlation with commodity prices. Revenue growth between 2013 – 2015 was primarily attributed to a number of acquisitions, including three branches of First Bank, adding $45 million and $81 million to loan and deposit balances, respectively.

On the other hand, the central theme impacting revenue in recent quarters was the Paycheck Protection Program “PPP” revenue loss. ATLO collected origination fees of up to 5% on these loans and other revenue for its service as an administrator of the PPP loans. The program ended in May 2021, distorting the YoY comparison. For example, Q3 2022 fees collected were a mere $2000 compared to $1.7 million a year before.

The rise in interest rates wasn’t enough to offset the negative impact of PPP on the top-line figure because of the maturity mix of its loan portfolio. Most of the company’s assets are tied to loans with maturity between 1 – 15 years. ATLO’s liabilities are more sensitive to interest rates than its assets. Thus, while its depositors saw an immediate benefit from rising interest rates, ATLO had to wait until its loans matured to reinvest in assets at a higher interest rate to realize the full benefit of higher yields. The maturity profile of banks isn’t built for abrupt changes in interest rates, and it wasn’t until the fourth quarter of 2022 that the benefits of rising rates on net interest income began to be realized by the company.

Balance sheet

I’ve come across reports warning investors about the risks of investing in financial companies because of the negative impact of rising interest rates on fair value calculations of bonds, particularly those marketed to the market, such as government bonds, which often carry fixed interest rates. Approximately half of ATLO’s assets are tied to fixed-rate bonds, and higher interest rates mean lower bond prices, decreasing the net asset value of banks’ holdings. I think this argument is overblown. ATLO indeed holds a significant amount of its assets in the form of marked-to-market assets. However, as a bank, ATLO holds its assets until maturity and will likely recover all its capital, thanks to its tried and tested underwriting processes. Moreover, most of ATLO’s $50 million (25%) decline in equity balance is, in my view, accounting noise with limited impact on cash flows.

However, it does have a more substantiated effect on capitalization ratios. Regulatory agencies require banks to maintain certain minimum levels of capital to act as a buffer against the risk of adverse events that may threaten the safety and soundness of the bank. In 2022 ATLO’s capitalization ratio declined significantly from 9.7% to 7% in the three months ended December 2022, as its government bond portfolio values declined. Nonetheless, according to the latest management comments earlier last week, the company is still Well capitalized as defined by regulatory agencies.

Summary

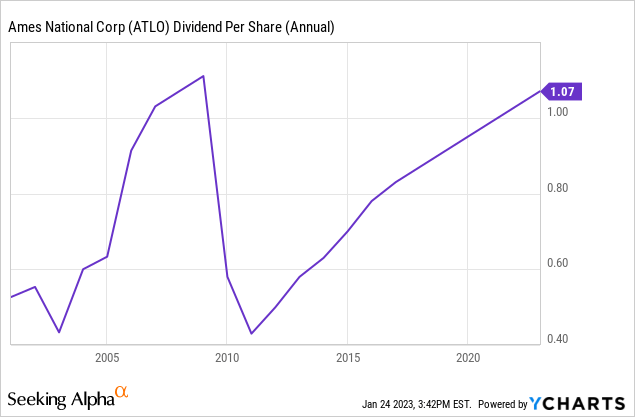

At current prices, ATLO has a dividend yield of 4.5 percent, which is enticing, considering that this is a financial institution with a successful track record and excellent fundamentals. Although I do not believe that ATLO, or community banks for that matter, will outperform the market, I am convinced that the company can provide a reliable source of dividend income to retirees and/or income-oriented investors who are looking for a high rate of return on their savings while minimizing the possibility of a loss in their principal investment. Admittingly, ATLO might withhold or cut the dividend to maintain regulatory capitalization ratios at times of economic distress. However, in the long-term, management seems committed to returning capital to shareholders, as mirrored in its historical dividend distribution and the fact that it increased dividend per share payments annually for the past ten years. Below is a chart showing ATLO’s dividend per share distribution since 2000.

Be the first to comment