filadendron

PagSeguro (NYSE:PAGS) is a Brazilian payments processor and digital bank. It is now the 2nd largest digital bank in Brazil and has 11% market share when it comes to payments processing.

Brazil is somewhat underpenetrated when it comes to cards (credit and debit) and banking, and its banking sector is highly concentrated. This leads to a market where there was (and is) an opportunity for new entrants to grow in, potentially very profitably.

PagSeguro has managed to grow a lot in the past, though some growth concerns emerged recently. Also, payment processors like PagSeguro have to finance a lot of float (since they typically pay merchants early). Even becoming a bank and taking on deposits isn’t a panacea, since they also have to remunerate deposits – though potentially at slightly lower interest rates.

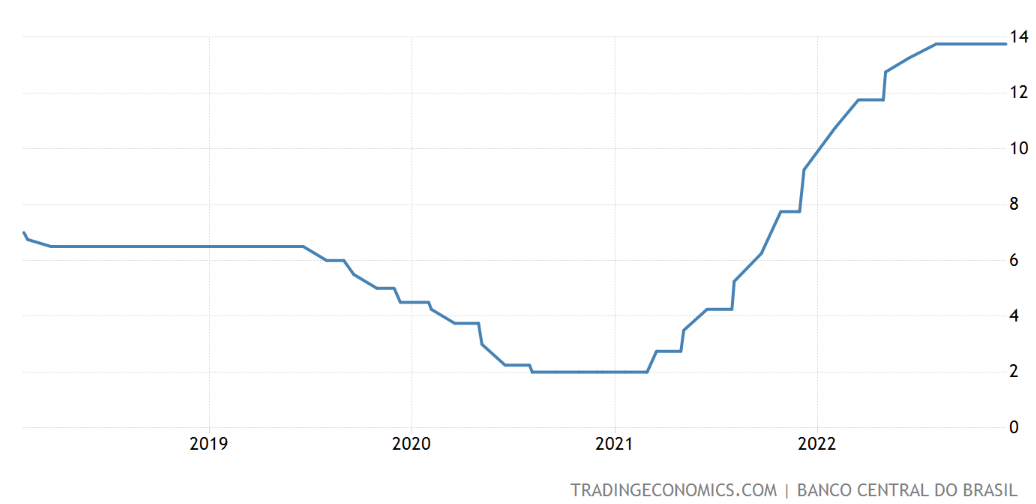

This large float requiring financing has meant that in the last 2 years, as Brazil’s Central Bank fought inflation by raising interest rates, the payment processors have had to face a large interest cost headwind to their profitability.

Brazil’s SELIC Rate (%)

Tradingeconomics.com

Alongside many other stocks, and also alongside this interest rate headwind, PagSeguro stock has been crushed. The stock is down more than 85% since its 2021 peak.

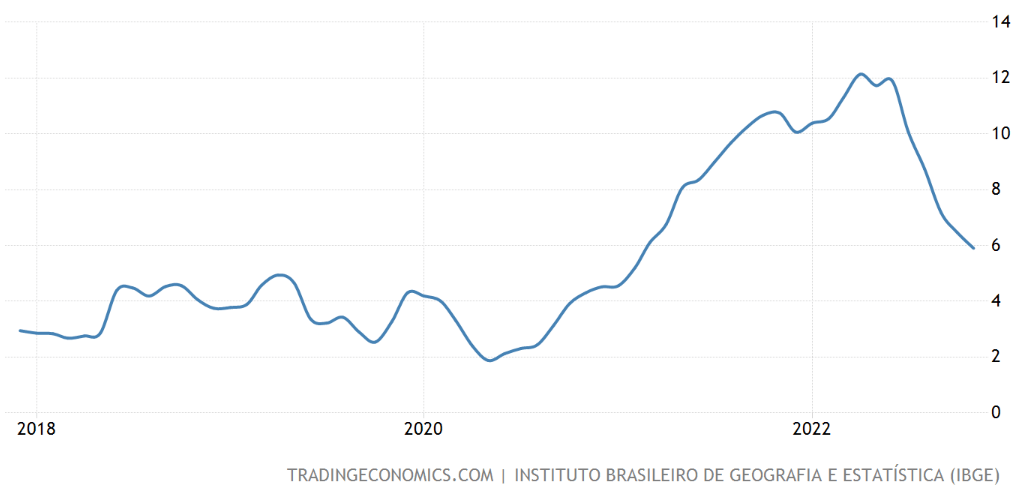

Finally, a great PagSeguro earnings driver, interest rates, looks set to drop rapidly. After all, while Brazil’s SELIC reference rate sits at 13.75%, its inflation rate has now crashed all the way to 5.9%:

Tradingeconomics.com

There’s no doubt the Brazilian Central Bank will start cutting rates and start cutting rates soon. Indeed, it’s almost odd that some analysts have been downgrading PagSeguro due to rates staying high for a tiny bit more time, when it’s so obvious that they’re about to be cut hard.

Given that PagSeguro has continued growing, and the overall context in which it does business seems so favorable, it’s natural to look at it and evaluate it as a potential investment, which is what I did. Especially since considering its consensus EPS, it trades at 8.7x 2022 earnings and 7.6x 2023 earnings.

Sure, there are other concerns, like the cap on interchange rates. Or Brazil’s intent to raise capital requirements for payment processors. However, the company has said the most concerning of those (cap on interchange rates) won’t have much impact on its earnings.

If this was all there was to PagSeguro, I would immediately see it as a strong buy, though I have subjective concerns on this sector potentially being open to extreme competition. The strong buy would be based on the prospects plus the extremely low valuation.

However, I did find something which, while not stopping me from seeing PagSeguro as a potentially decent investment, does make it look less cheap than I previously thought.

The Problem With PagSeguro’s Earnings And Thus, Price/Earnings

To be short about it, what I found is that there’s a factor which greatly influences PagSeguro’s reported and non-GAAP earnings, and in my opinion, this factor can’t be ignored.

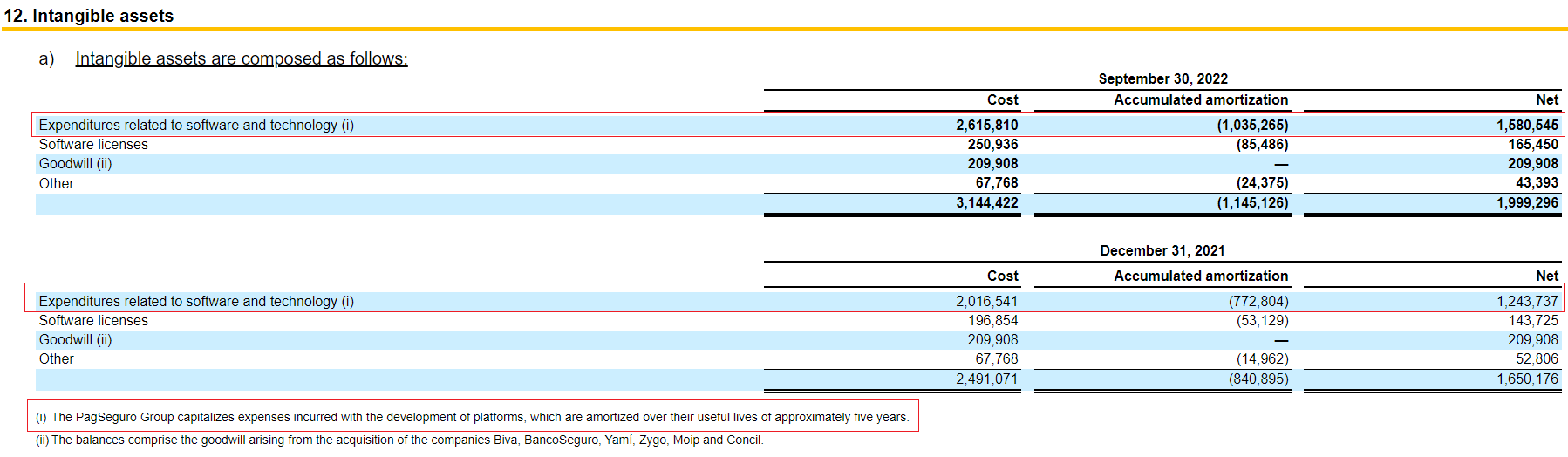

The factor is that PagSeguro capitalizes on a lot of software development, and then depreciates this software development on a 5-year schedule (red highlight is mine).

PagSeguro

In the last 9 months, there were roughly 340 million BRL capitalized in this way (net of amortization of prior capitalized costs). In the same timeframe, PagSeguro had 1,280 million BRL in pre-tax profits. Had these costs been expensed, and pre-tax profits would have been 27% lower, and the P/E would thus be 37% higher. For instance, the 2022 P/E would be 12.0x instead of 8.7x.

8.7x is quite cheap and gives something of a margin of safety. 12.0x looks a lot more normal for a financial company.

This effect gives me some pause regarding PAGS. Instead of “deep value”, it makes it look more like “value”. Instead of “strong buy”, it makes it look more like “buy”.

Of note, it’s not like other companies, for instance, Fiserv (FISV), don’t do the same. They do. There’s nothing untowardly here. But when I try to find opportunities, this search isn’t necessarily restricted to a specific sector – instead, the search focuses on many different sectors, and most don’t have this large (so relevant) capitalization of what would otherwise be simple operating costs.

Conclusion

PagSeguro has a lot going for it, including the context it acts in and the lack of competitiveness in Brazil’s banking market. Also, Brazilian interest rates are set to start declining visibly soon, with a high degree of confidence. This bodes well for future profit growth.

At the same time, optically, PagSeguro already seems extremely cheap at 8.7x earnings. The combination of a positive profit catalyst and currently extremely low apparent valuation is very attractive.

However, upon closer inspection, it does seem that PagSeguro’s amortization for software development inflates current earnings somewhat. If we strip out this effect, the valuation becomes somewhat more mundane at 12.0x earnings.

PagSeguro still looks attractive, though. Just not as attractive.

Be the first to comment