Michael M. Santiago/Getty Images News

Many investors view the large U.S. money center banks as similar and expect them to trade in a pack. In reality, though, each has a very different business mix that manifests in very different outcomes for shareholders.

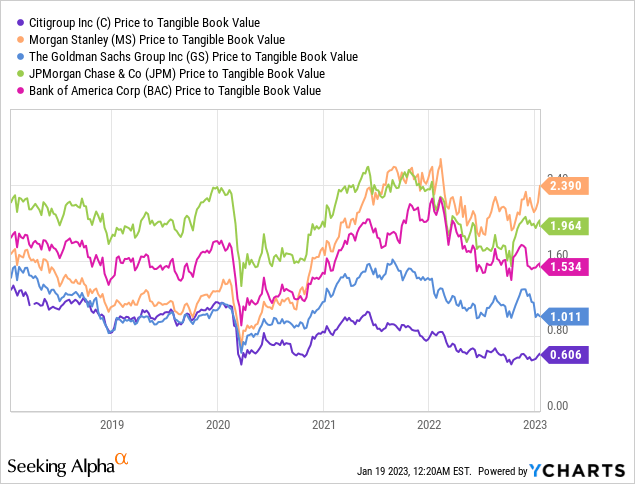

My favorite matrix for banks is the price to tangible book value (“TBV”) and return on tangible common equity (“RoTCE”).

Consider the below chart for the large U.S. banks:

As you can see from above, the valuation of these 5 large U.S. banks diverges materially. For example, Morgan Stanely (NYSE:MS) is ascribed a premium of ~4x to Citigroup (C). This is primarily a function of the business model and mix that evolved over the last decade or so in the wake of the global financial crisis (“GFC”).

The GFC was a watershed moment for the large banks as the rules of the game were rewritten by regulators which in turn completely changed the returns profile of the different businesses. In the post-GFC world, the trading businesses (e.g. FICC) became much more expensive to run and attracted a much higher capital charge compared with their consumer banking cousins. On the flip side, capital-light businesses like wealth management and asset management became much more attractive. Some management teams understood this very early on (like James Morgan) whereas others like Citi and Goldman Sachs (NYSE:GS) missed the boat and are still looking to revamp their business model.

In other words, Coming out of the GFC, each bank made a strategic decision to double down on certain business segments and deemphasize others. The current valuations of these banks are effectively a product of these capital allocation decisions.

For example, Citi opted to focus on being a global consumer bank operating in multiple jurisdictions. Citi’s management believed at the time, that emerging markets’ GDP will grow faster than its home market in the U.S. and thus allocated capital and aligned its business model accordingly. It also doubled down on the corporate investment bank as well as the global Credit Cards business believing the latter should deliver ROE in the high teens. Citi deemphasized wealth management and sold its JV interest in Smith Barney to Morgan Stanley (MS). The strategy has proven to be an unmitigated disaster and Citi’s new CEO has essentially reversed that in a rather painful and protracted strategic revamp.

In this article, though, I will compare and contrast GS and MS and conclude which is the better investment for 2023.

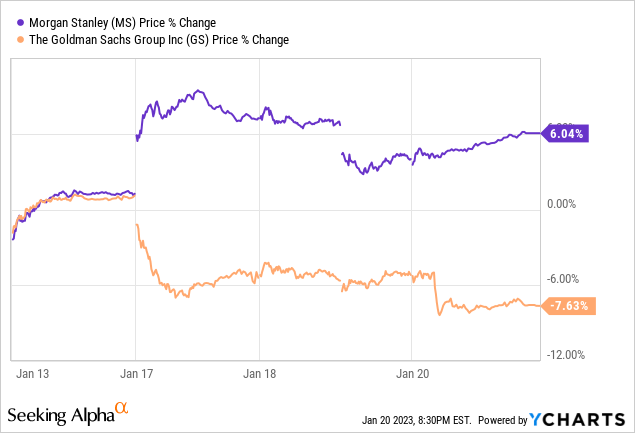

The Reaction To Q4 Earnings

GS’s CEO, David Solomon, must have been fuming looking at the divergent market reaction to the Q4 earnings reports released by MS and GS on the 17th of January (which incidentally coincided with his birthday).

The relative ~14% in relative performance this week reflects both the undeniable success of MS’s focus on the capital-light wealth management business as well as GS’ over-reliance on volatile investment banking and the ill-advised adventure into consumer banking.

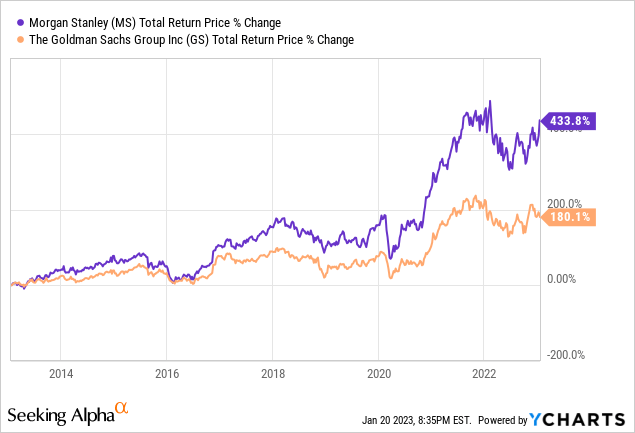

The longer-term picture over the last 10 years tells the same story:

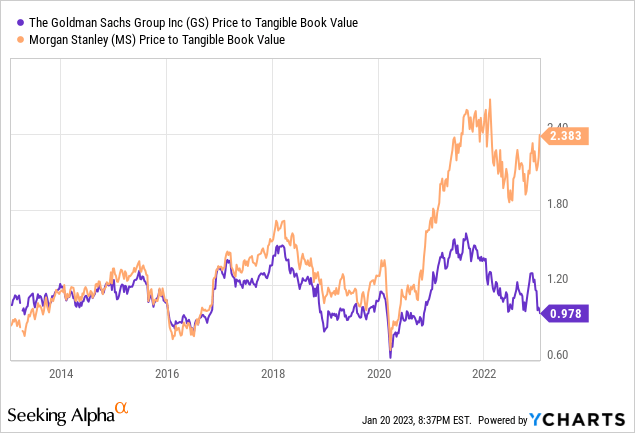

Viewing the same chart through a price-to-book valuation:

The valuation of MS catapulted in recent years as the market rewards it for the success of its wealth management strategy that consistently delivers durable and strong returns even in bear markets.

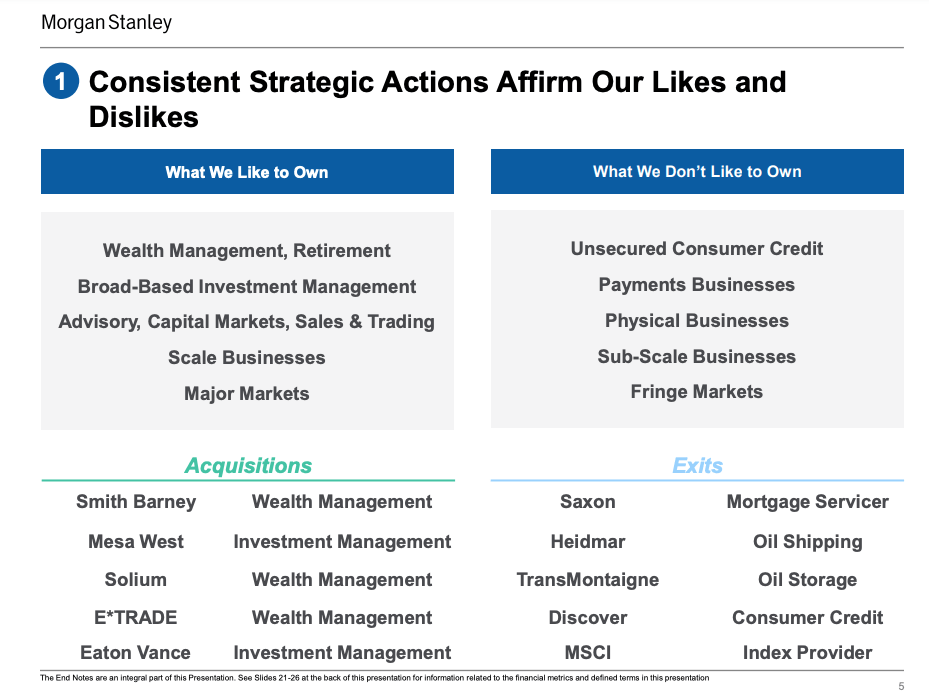

MS (perhaps with a slight dig towards GS and other peers) has highlighted “our likes & dislikes” business lines in the strategic update presentation released on the 17th Jan 2023:

MS Investor Relations

Clearly, MS is highly focused on quality businesses and executing a clear and coherent strategy to grow the capital-light businesses of wealth and asset management.

GS, on the other hand, is facing an identity crisis. There is no doubt, GS is the best class in investment banking and global markets division. The problem is that Mr. Market will not give high multiples for these businesses as they are both volatile and consume a lot of capital. As noted above, this is a function of the post-GFC regulatory capital framework as well as the Dodd-Frank Act.

Understanding Goldman Sachs

GS operates through 3 divisions:

- Global Banking & Markets (“GBM”);

- Asset & Wealth Management (“AWM”); and

- Platform Solutions (“PS”)

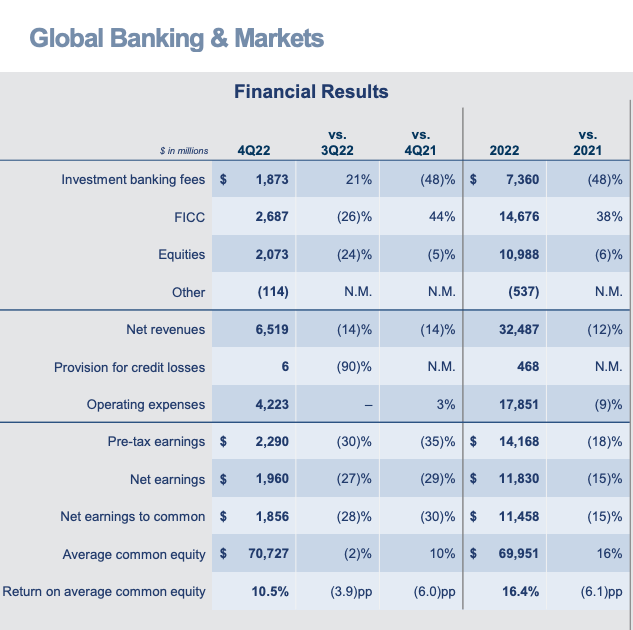

GBM is the largest and comprises the markets trading business (i.e. FICC and Equities trading) as well the investment banking segment (debt, equity, and M&A advisory). The results for 2022 are shown below:

GS Investor Relations

As can see above, GS allocates ~$70 billion of capital to this division and generated an ROE of 16.4% in spite of strong headwinds in investment banking where the industry wallet was down more than 50% due to the bear market in 2022 and rapidly rising rates that cause both debt and equity issuances to freeze.

Make no mistake about this, these are fantastic results and it is very clear that GS is the market leader in terms of returns in this business. I estimate that the likes of Citigroup and JPMorgan (JPM) would ordinarily generate only about 10-12% ROE in these segments.

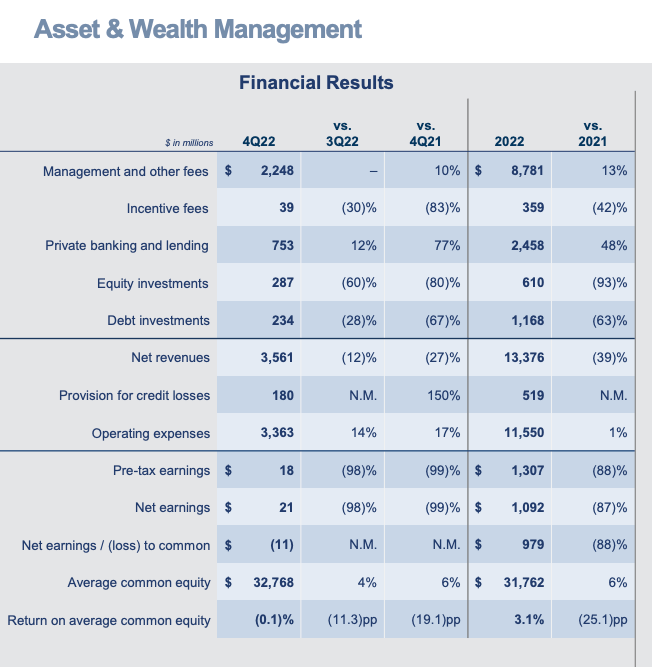

The AWM division comprises wealth management, asset management, private banking business as well as GS’ proprietary equity and debt investments (e.g. private equity):

GS Investor Relations

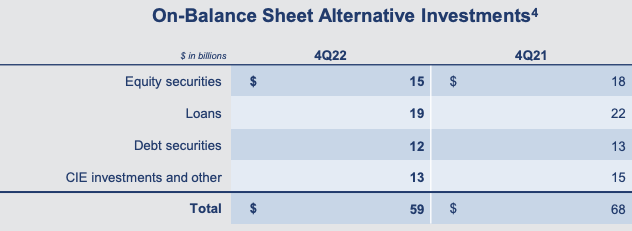

As can ascertain from above, the returns in 2022 were far from impressive at only 3.1% ROE. The main culprit is the proprietary investments (equity and debt investments) that were down 93% and 63% respectively due to the bear market valuations. The proprietary investments currently stand at $59 billion and consume a disproportionate amount of capital, it is a very capital-heavy business model. GS’s strategy has been to work these down over time but the pace has not been frantic, to say the least:

GS Investor Relations

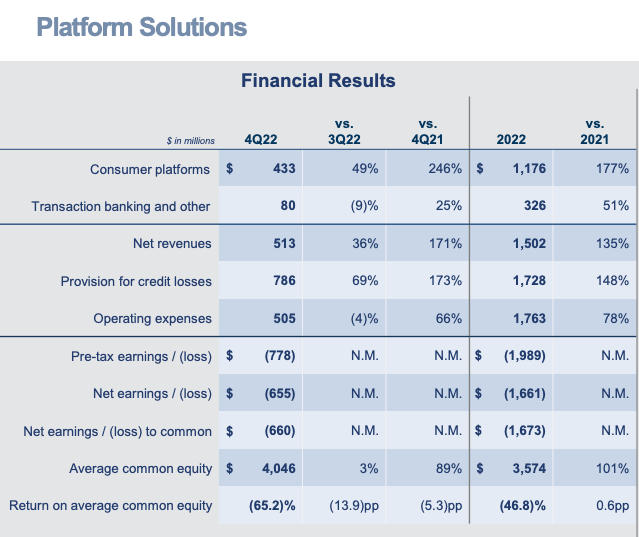

The third division is known as Platform Solutions which comprises the consumer business as well as transaction banking. It only consumes ~4b of capital and is approximately 3% of the bank, yet produces disproportionate net income losses (~$1.7 billion) as can be seen below.

GS Investor Relations

GS’s strategy is now to deemphasize the consumer lending business (Marcus), pivot to high-net-worth clientele, reduce costs and attempt to deliver profitability. It is retracting from the strategy outlined previously by Lloyd Blankfein. The losses are too large to bear and GS is in a hurry to cut their losses and move on. Whereas the transaction banking business is a nice one but still sub-scale and unlikely to move the dial anytime soon.

Understanding Morgan Stanely

MS is operating through two large divisions:

- Institutional Securities (“IS”)

- Wealth Management (“WM”)

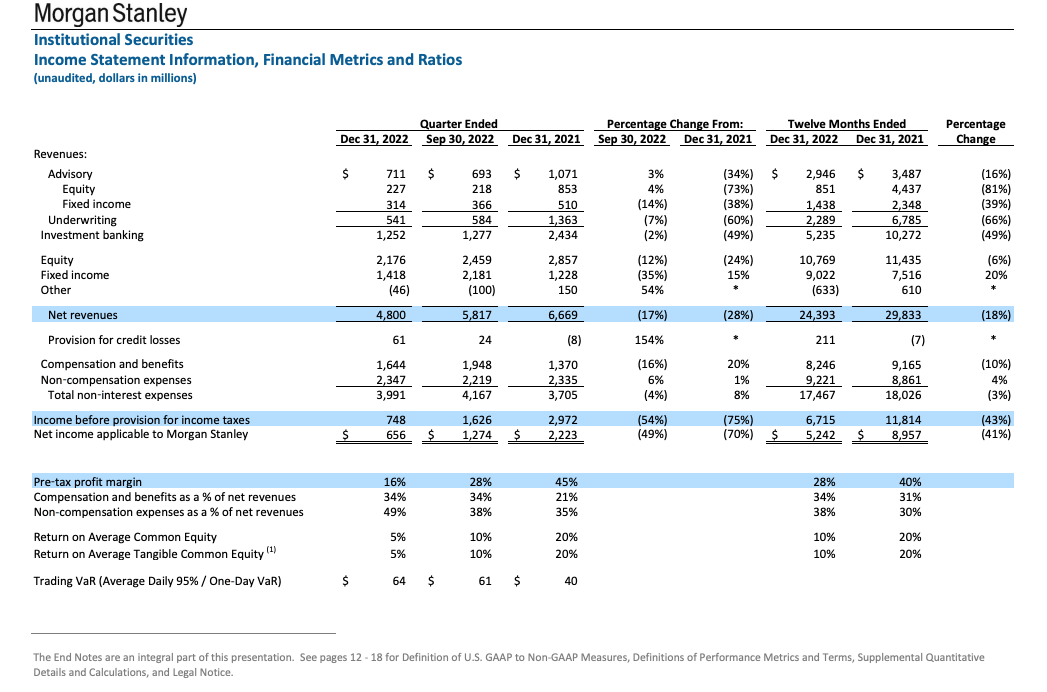

IS is similar to GS’ GWB and comprises both market trading businesses (FICC and Equities trading) as well as investment banking (debt, equity, and M&A advisory). From a business mix, MS is more slanted towards Equities trading as opposed to FICC. As such, it is not surprising that its returns in the IS division in 2022 (at 10% ROE) were significantly lower than what GS delivered (16.4%).

MS Investor Relations

As can be seen from above, similar to GS, the investment banking fees were ~50% lower in 2022 in line with industry wallet reductions due to the bear market. Also, Equities trading was lower (-6%) year-on-year whereas FICC delivered 20% year-on-year growth. As noted above, MS’ business mix is heavily slanted toward Equities trading and as such, underperformed on a relative basis compared to peers who are stronger in FICC trading.

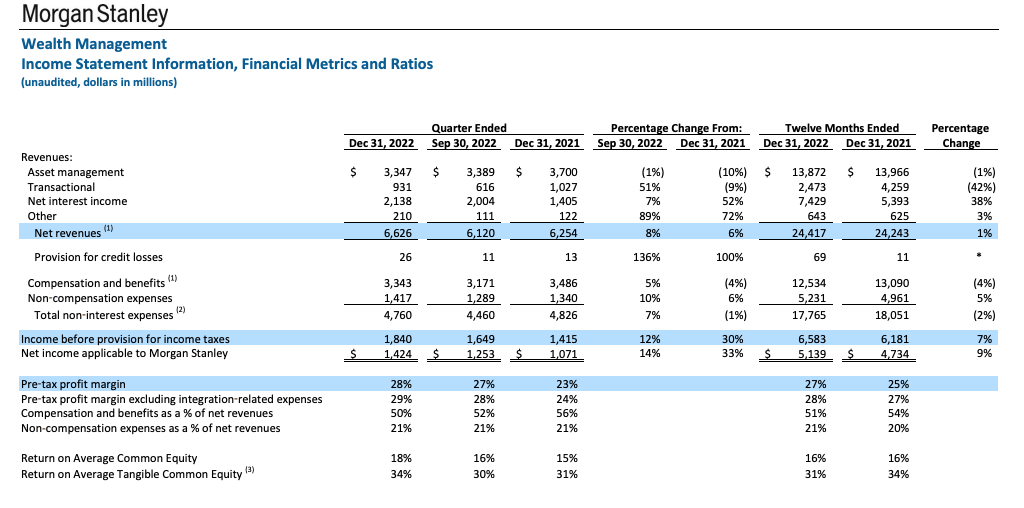

MS’s wealth management division continued to deliver in 2022 in spite of the deep bear markets in both bonds and equities. The WM division produced a 9% year-on-year growth in net income which is astounding given the macroeconomic conditions prevailing in 2022.

MS Investor Relations

As can be seen above, WM is delivering >30% ROE which is an exceptional return for a bank. Interestingly, the WM net income is roughly the same as the IS division (~$5b of net income), however, utilizes a third less capital.

And this is really the success story of MS and why it is ascribed to such high multiples. The WM is delivering not only exceptional returns (>30% ROE) but are also stable and durable in almost all market conditions.

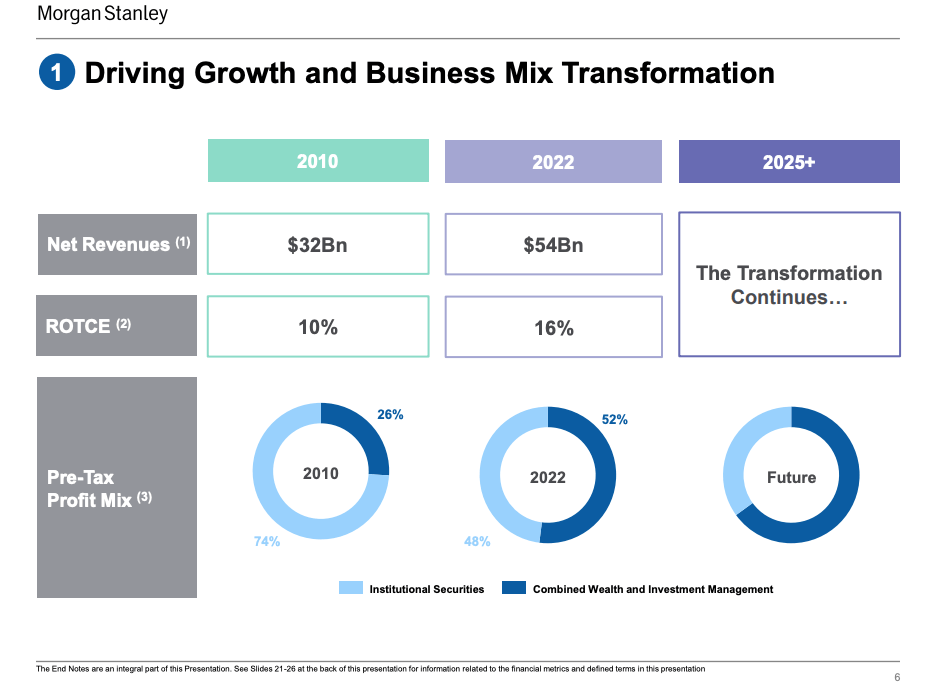

MS strategy remains the same and is all about increasing the percentage of WM net income in the earnings mix. In 2022, it is ~50%, and management projects that it will be much higher in the medium term as reflected in the below slide from the strategy update:

MS Investor Relations

Discussion: Which Bank Is The Better Investment In 2023?

GS is the market leader in investment banking and trading. However, Mr. Market will not ascribe a high multiple even in boom times when it delivers astounding trading results. Simply because it is a capital-heavy and volatile business. GS recognized this several years back and attempted to develop other more stable business lines. It clearly failed to execute the strategy and all it has to show for now are sub-scale businesses and losses. The good news is that management realizes this now and is cutting its losses quickly as it deemphasizes the consumer businesses.

It is also clear that the only viable strategy for GS is to double down on WM and third-party asset management. GS has to grow this division both organically and inorganically and reduce its reliance on proprietary investments.

MS, on the other hand, is executing a brilliant strategy. The higher the business mix shifts to wealth management, the higher valuation Mr. Market will ascribe to its stock. It currently holds $5.5T of client assets and expects to almost double it to $10T in the medium term. It is astounding that it increased its profitability in 2022 when the equity markets were down ~20% and bonds were down ~15% and a testament to its exceptional business model.

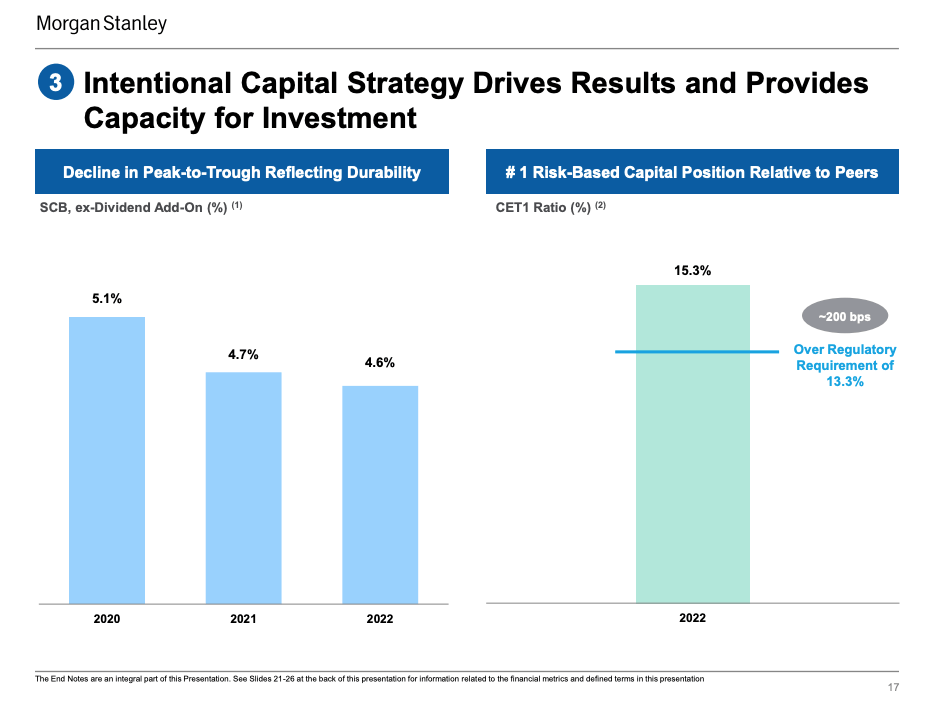

The business model is also very efficient from a capital utilization perspective. MS is delivering this profitability whilst operating with 200 basis points capital buffer above its minimum requirement and is performing exceptionally well in the Fed’s CCAR stress tests.

MS Investor Relations

Having said that, at 2.4x tangible book, MS is more than fairly valued relative to its peers and specifically GS. It has always been a strong buy signal to buy GS where it traded below tangible book.

It is true that many of GS’s problems are business model related and somewhat self-inflicted. However, I am confident management will be laser-focused on fixing this. 2022 has been a tough year for GS and returns have been hurt by both losses in the consumer platforms as well as negative marks in the proprietary debt and equity investments. The latter is unlikely to recur. On a normalized basis, one would expect GS to deliver mid-teens ROE. The upside or game-changer will manifest if it can seriously grow the asset and wealth management division. GS has some of the best talents in the industry, I would not bet against it.

Final thoughts

The resiliency of the banking industry and business model is nothing short of astounding (yet I am not surprised) given the macro conditions prevailing in 2022.

In a deep bear market, MS and GS delivered 15% and 10% ROE respectively. GS still delivered 10% ROE in spite of negative marks on proprietary investments and loss-making consumer division to the tune of $1.7 billion. MS wealth management division delivered 9% year-on-year growth where both the equity and bond markets were deep in the red. These are exceptional results.

MS has clearly a superior business model compared to GS but is fairly valued on a relative basis. GS is trading lower than tangible book value as I write this article. In part, this is due to its business model which is much more volatile but I believe management can fix it in the medium term. The key remains inorganic acquisitions in the asset and wealth management division(similar to the path MS has taken). GS has some of the smartest talents on Wall Street, to me, the risk/reward is highly attractive at current valuations. GS will hold its investors’ day on the 25th of February, I expect it to reveal the refreshed strategy. I have little doubt, it will be focused on the asset and wealth management division growth.

As such, I rate GS as a strong buy now. I also absolutely love the MS business model and rate it as a buy given that it is fairly valued on a relative basis to peers.

Be the first to comment