Michael M. Santiago

Goldman Sachs BDC (NYSE:GSBD) currently provides a 12.1% dividend yield generated by a safety-focused debt-centric investment portfolio, and the business development company covers its dividend with net investment income.

Goldman Sachs BDC also provides exposure to a floating rate portfolio of debt instruments, implying rising net investment income if the central bank continues to fight inflation in 2023.

Since the BDC’s stock was trading at a much higher NAV premium last year (and is now trading at a discount) and the portfolio has become less risky, I believe GSBD is an even more compelling buy right now than it was two months ago when I last covered the BDC.

Safe And Floating Rate Portfolio

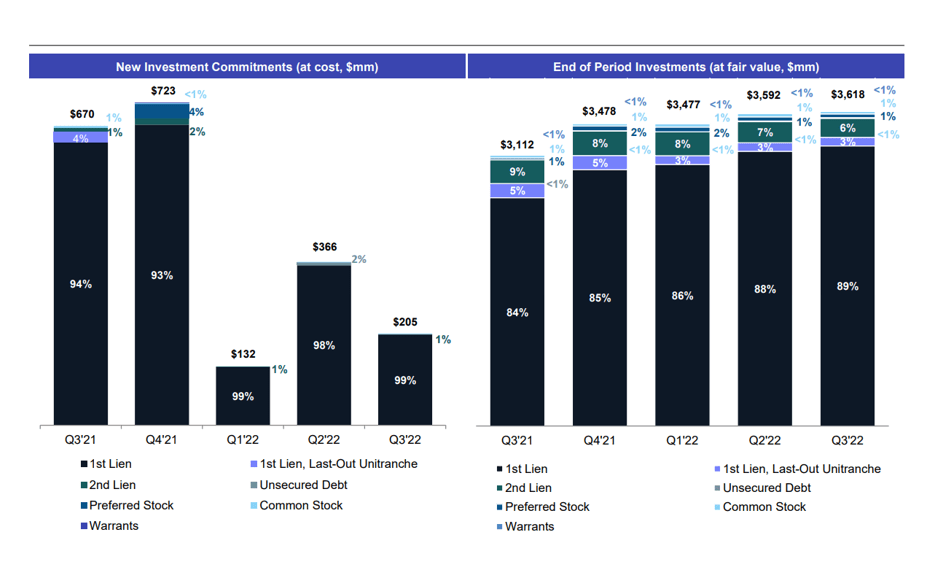

Goldman Sachs BDC is a higher quality business development company with a developed focus on the highest quality forms of investment debt. Goldman Sachs BDC invested $3.6 billion in its portfolio, which included secured first liens (89%), second liens (6%), and other assets such as unsecured debt, preferred stock, and common stock.

Also worth noting: new investment commitments made in the third quarter (as well as in the previous year) were overwhelmingly for First Liens, which explains why they have grown in relative importance for the business development company in 2022. First Liens accounted for 84% of portfolio investments in 3Q-21, implying that the share of high-quality debt increased by 5 percentage points over the previous four quarters to 89% in 3Q-22.

By prioritizing higher-rated First Liens, Goldman Sachs BDC has positioned its portfolio to provide greater protection against a recession and an increase in loan defaults.

New Investment Commitments (Goldman Sachs BDC)

The investment portfolio of Goldman Sachs BDC is also poised to benefit from rising interest rates. In order to combat inflation, the Federal Reserve embarked on an aggressive rate hike cycle in 2022, and since inflation remains high, the central bank has a strong case for justifying further interest rate increases in 2023.

Higher interest rates increase the BDC’s net interest income potential because floating rate assets account for 99.6% of all portfolio assets.

The Federal Reserve is expected to raise rates by 25 basis points at the end of January, and Citigroup expects rates to reach 5.5% in May as the Fed works to return inflation to its long-term target of 2.0%.

The Federal Reserve is expected to raise rates by 25 basis points at the end of January, and Citigroup expects rates to reach 5.5% in May as the Fed works to return inflation to its long-term target of 2.0%.

If inflation proves to be more of a nuisance than expected in 2023, which is not an entirely unreasonable assumption given the strength of the labor market, interest rates may remain higher for longer, helping Goldman Sachs BDC make an even stronger investment case.

84% Dividend Pay-Out Ratio

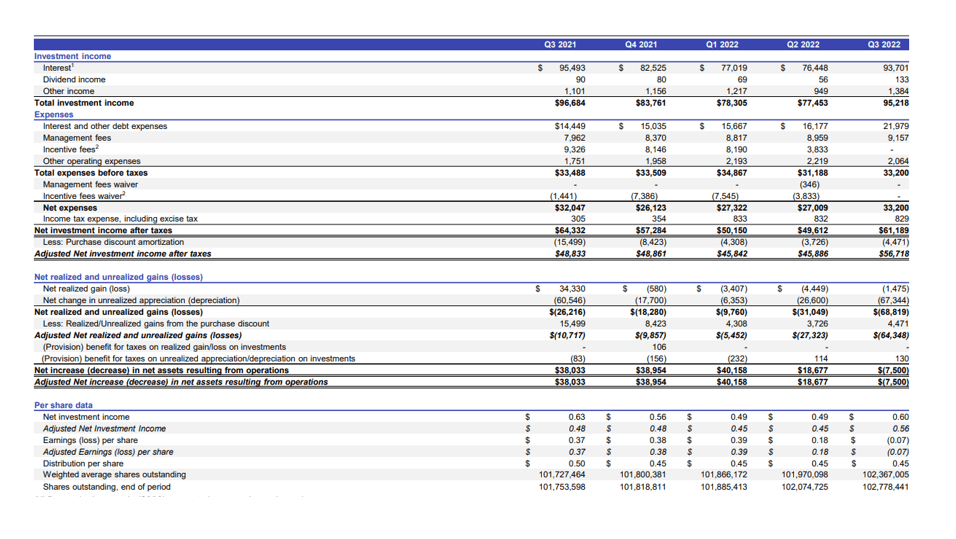

Goldman Sachs BDC has covered its dividend payments with net investment income over the last year. In the period 4Q-21 to 3Q-22, the business development company earned $2.14 per share in net investment income, while Goldman Sachs paid out $1.80 per share in dividends. The dividend pay-out ratio for the last twelve months was 84%, providing the BDC with adequate dividend protection.

The GSBD portfolio’s floating rate exposure may result in a lower dividend pay-out ratio, though the ultimate impact will depend on the extent of the central bank’s interest rate hikes.

Net Investment Income (Goldman Sachs BDC)

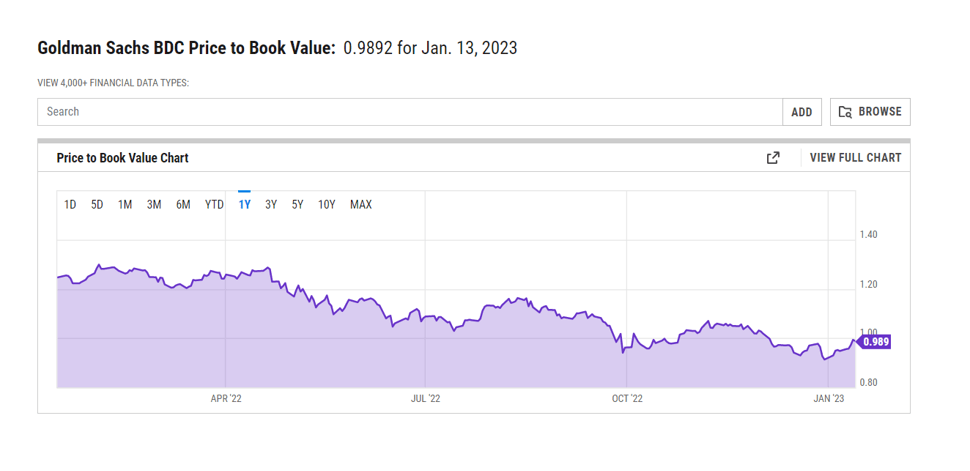

1x P/B Valuation

The stock of Goldman Sachs BDC is now trading at around portfolio net asset value, making this a great time to buy the BDC in my opinion.

GSBD traded at a 28% premium to net asset value, and I believe the BDC’s valuation can be restored if the company maintains good portfolio quality and continues to pay its $0.45 per share quarterly dividend.

Price To Book Value (YCharts)

Why Goldman Sachs BDC Could See A Lower Valuation

Just because a company has good dividend coverage now does not guarantee that it will have good coverage next year, or even next quarter. I believe Goldman Sachs’ First Lien-focus is a strong selling point for the business development company, as is the portfolio’s floating rate exposure for passive income investors.

The extent to which GSBD earns its dividend will be largely determined by the central bank, which may ease off the gas in terms of interest rate hikes once inflation has been brought down to an acceptable level.

My Conclusion

Goldman Sachs BDC is a high-quality business development company with a portfolio that has become safer in the last year as a result of a more focused allocation of capital to high-quality First Liens.

The central bank also has a compelling case for its rate hike policy, which will benefit Goldman Sachs BDC’s portfolio income potential.

Given that Goldman Sachs BDC covers its dividend with net investment income and that the BDC’s stock sold at a relatively high premium to NAV last year, I believe GSBD’s NAV multiple has room to grow.

Meanwhile, investors can enjoy a covered 12.1% dividend yield, and I’m buying more.

Be the first to comment