marchmeena29

Introduction

In May 2022, I wrote an article on SA about Mexico-focused gold and silver mining company Gold Resource Corporation (NYSE:GORO) in which I said that Back Forty looked like a compelling project but that I was concerned by the high peak funding requirements.

The company keeps investing significant funds into its Don David gold mine, whose production and financial results look underwhelming. In addition, quarterly dividends are still $0.01 per share and I think that there could be significant stock dilution here if the plan remains to start construction in 2024. Let’s review.

Overview of the recent developments

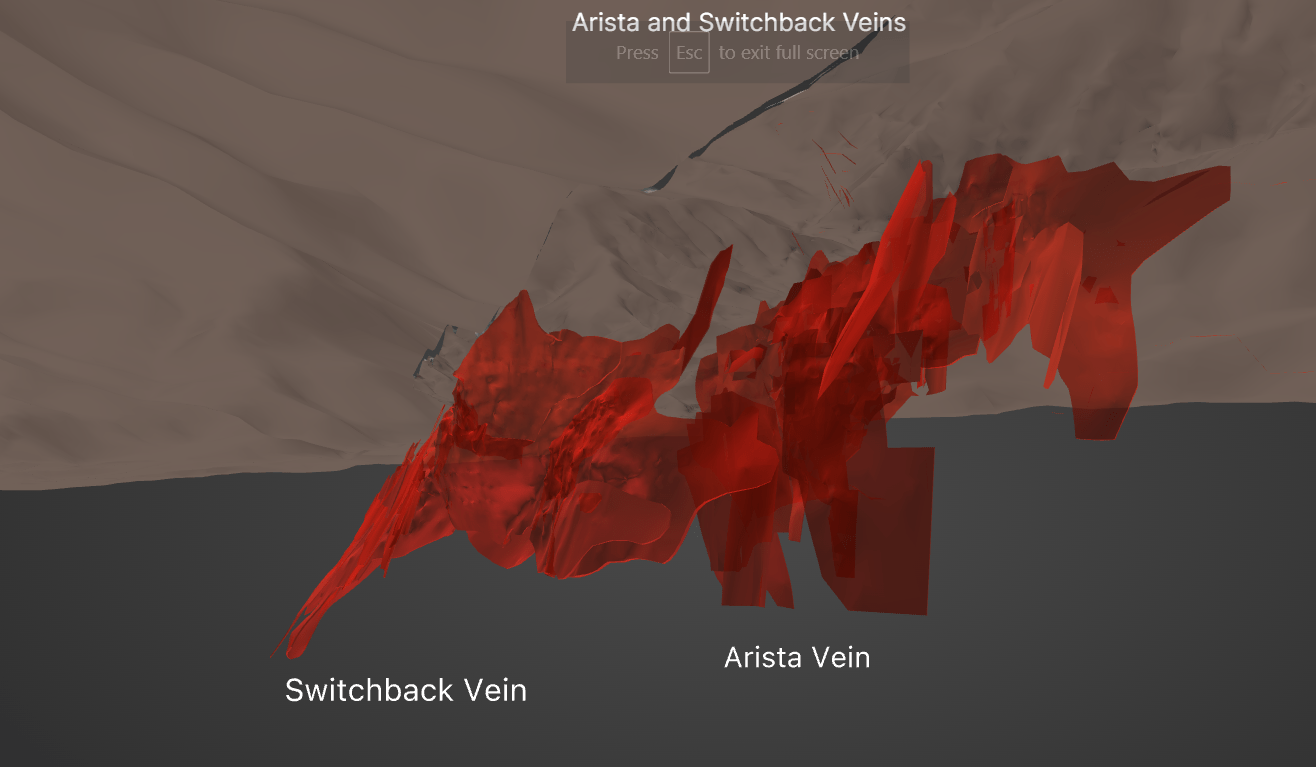

In case you haven’t read any of my previous articles about Gold Resource, here’s a brief description of the business. The company owns a package of six polymetallic projects in Mexico’s southern state of Oaxaca that form the Don David gold mine. At the moment, the vast majority of production comes from the El Aguila project that hosts the Arista deposit, which contains gold, silver, copper, lead, and zinc.

Gold Resource Gold Resource

As of December 2021, Don David had proven and probable reserves of 123,500 ounces of gold equivalent, a total of 118,000 ounces of which are located at Arista. In my view, this number is likely to increase in the future, as the deposit is currently open in strike and at depth.

Gold Resource

In December 2021, Gold Resource acquired the Back Forty gold and zinc project in the U.S. state of Michigan through the C$30.9 million ($23.9 million) purchase of Aquila Resources. In 2018, the latter released the results of a feasibility study according to which the project has an after-tax net present value (NPV) of $208 million at $1,300 per ounce of gold using a discount rate of 6%. At today’s gold prices of just over $1,000 per ounce, the NPV should be about $540 million.

Aquila Resources

Average annual gold production is expected to stand at 67,000 ounces over a life of mine of just 7 years, but the estimated average all-in sustaining costs (AISC) are forecast to come in at just $397 per ounce on a by-product basis, which would make Back Forty one of the lowest-cost gold producers in the world. In my view, the main issue here is the high initial CAPEX and long construction period, as the mine will take two years to get built, and the peak funding requirement is $296 million. The number is likely to be significantly higher today, as we’ve witnessed significant inflation in materials and labor costs over the past four years.

Aquila Resources

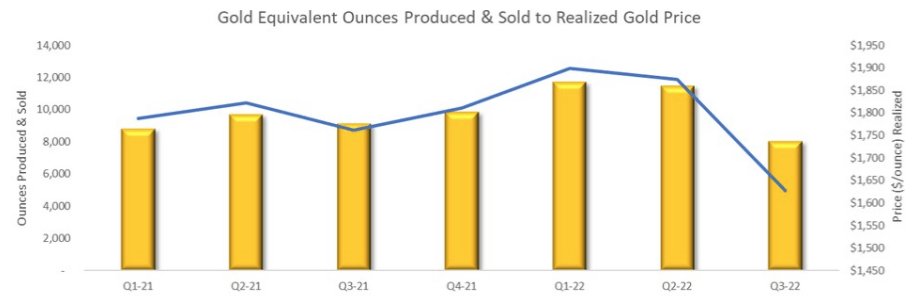

Turning our attention to the financial performance of Gold Resource, the first 9 months of 2022 were challenging, and cash and cash equivalents decreased to $22.5 million from $33.7 million as of December 2021. The third quarter of the year was particularly tough as metal prices decreased while gold and silver production at Don David declined by 16% and 2% year on year to 5,851 ounces and 261,256 ounces, respectively. The reason for this was lower gold and silver grades processed as production was deliberately slowed down to improve safety specific to ground support and ventilation. In addition, the company faced a long rainy season.

Gold Resource

Looking at the financials, Q3 2022 sales declined by 13.1% to $27.7 million while costs soared due to a $2.1 million increase in production costs as well as a $3.1 million rise in depreciation expenses as Gold Resource completed $16.9 million capital projects. This put Don David deep in the red, as the net loss came in at $9.7 million.

Gold Resource

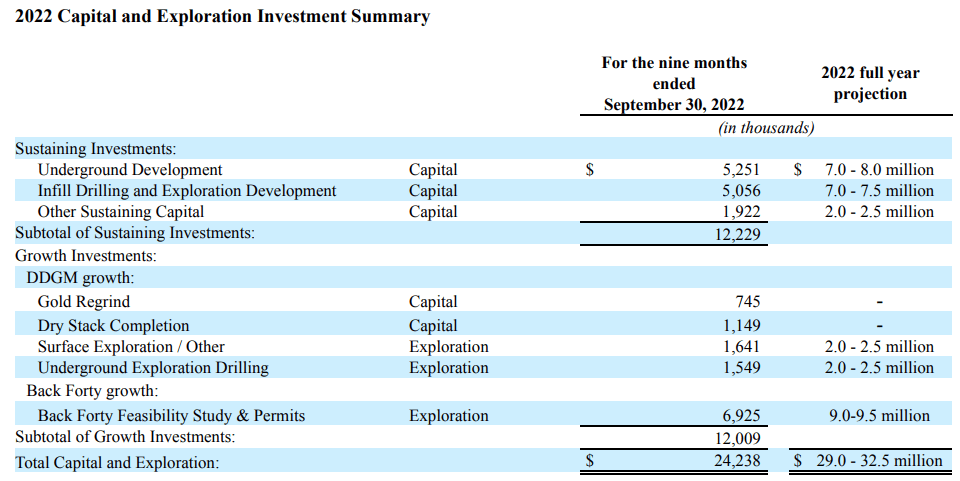

In my view, Gold Resource is in deep trouble from a liquidity perspective as another $6.9 million was invested in feasibility and permitting initiatives at Back Forty during the first 9 months of 2022. CAPEX and exploration expenses for the full year were expected to stand at between $29 million and $32.5 million.

Gold Resource

In addition, Gold Resource is keeping its quarterly dividends unchanged at $0.01 per share which is equal to about $3.6 million on an annualized basis. The liquidity situation will be further complicated by the fact that the company has to make payments of C$9 million ($6.7 million) when Back Forty enters commercial production and there is a streaming agreement under which 18.5% of gold production will be sold at up to $600 per ounce until reaching $105,000 ounces, after which the stream drops to 9.25% of the refined gold production. In the case of silver, 85% of production will be sold at $4.00 per ounce. This means that cash flows during the first two years of commercial production will be impacted significantly. With just $22.5 million in the bank and Don David generating negative EBITDA, Gold Resource will need a significant funding package to put Back Forty into production and wait until the streaming agreements become more bearable. According to the September corporate presentation of the company, the new mine is forecast to reach commercial production in 2026. Considering construction should take two years, I expect Gold Resource to announce a financing package by the end of this year. In my view, the funding is likely to include a significant equity portion.

Gold Resource

Building a gold mine is often challenging, and delays and cost overruns could put significant pressure on financials. With no meaningful catalysts for the share price on the horizon, I think that this is likely the wrong moment to invest in Gold Resource.

Investor takeaway

Gold Resource’s Don David mine slipped into the red in Q3 2022 and the company’s cash and cash equivalents decreased to $22.5 million at the end of September. While Back Forty should have a NPV of over $500 million at today’s gold price, Gold Resource is likely to require a significant capital increase in the near future if it wants to start construction in 2024. Considering there could be delays and cost overruns and cash flows will be limited during the first two years of production, I think there are better investment opportunities in the gold sector at the moment. In my view, it could be best for risk-averse investors to avoid this stock.

Be the first to comment