David Becker/Getty Images News

Thesis

Advanced Micro Devices (NASDAQ:AMD) had a tough 2022. Both earnings and valuation multiple contracted substantially, leading to a painful share price decline. To wit, its stock prices fell by about 50% during the past year, compared to a loss of about 15% in the S&P 500 index. Indeed, business at AMD has been facing strong headwinds lately, with most of its segments weighed down by weakening PC demand and also inventory digestion across the industry. Take its recent Q3 as an example. Q3 sales came in at $5.57 billion, representing the first sequential decline in nearly 3 years. And the decline was attributed to lower client segment revenue (down by 40% YOY).

Seeking Alpha data

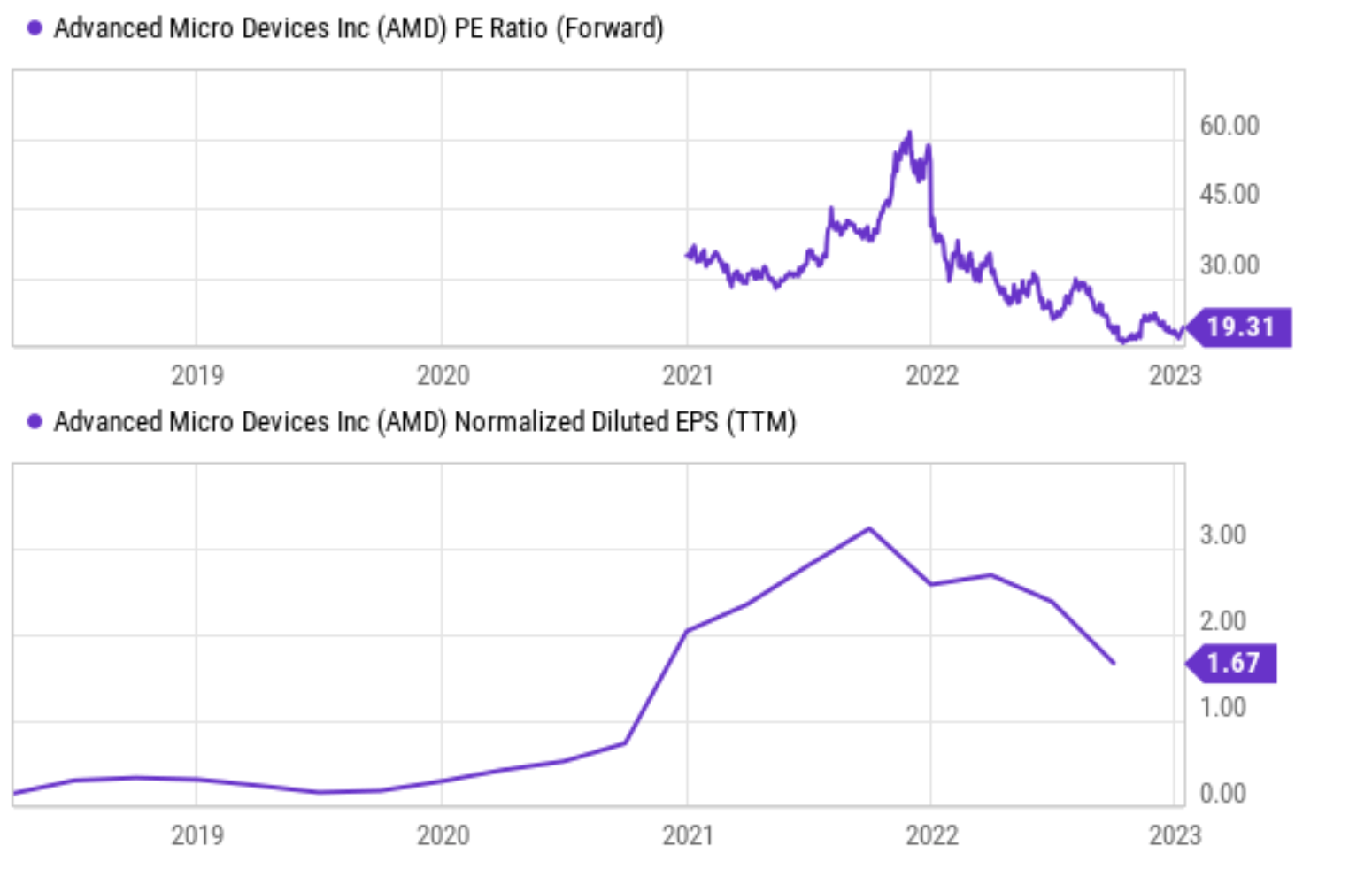

Looking ahead, I see a robust growth curve, especially in its Embedded and Data Center segments. And I see the current valuation contraction overdone. With an FW PE ratio around 19x, I see its PEG (P/E growth ratio) falling below the threshold of 1x, representing a good opportunity to buy a high-growth and high-quality business at a reasonable price.

There are a few strong growth catalysts ahead. First, I see the gaming segment poised to enjoy long-term tailwinds due to AMD’s relationship with Sony and Microsoft, the two global game console leaders. Second, AMD actually maintained a robust gross margin amid all recent headwinds. It is just that a good part of the margin was canceled off by higher operating expenses. However, I see such higher operating expenses to be also temporary as inflation eases. And finally, and most importantly, I see the recent successful acquisitions of Pensando and Xilinx to spur growth in two of its strategic segments for years to come, as to be detailed in the remainder of this article.

Xilinx and Pensando acquisition

Like many AMD investors, I see the Embedded and Data Center segments to be two of its strategic growth areas for the future. And I further see its two recent successful acquisitions, Pensando and Xilinx, to spur growth in these strategic segments for years to come. Both acquisitions were completed in the recent 1~2 years (Xilinx in Feb 2022 and Pensando in May 2022). Details of both acquisitions are provided in AMD’s press releases and quoted below with slight edits by me.

Xilinx acquisition press release: Xilinx offers industry-leading FPGAs, adaptive SoCs, AI inference engines, and software expertise that enables AMD to offer the strongest portfolio of high-performance and adaptive computing solutions in the industry and capture a larger share of the approximately $135 billion market opportunity we see across cloud, edge, and intelligent devices. AMD expects the acquisition to be accretive to non-GAAP margins, non-GAAP EPS and free cash flow generation in the first year.

Pensando acquisition press release: AMD today announced that it has completed its acquisition of Pensando Systems in a transaction valued at approximately $1.9 billion. Pensando’s distributed services platform will expand AMD’s data center product portfolio with a high-performance data processing unit (DPU) and software stack that is already deployed at scale across cloud and enterprise customers including Goldman Sachs, IBM Cloud, Microsoft Azure, and Oracle Cloud.

Xilinx and Pensando add both scale and scalability

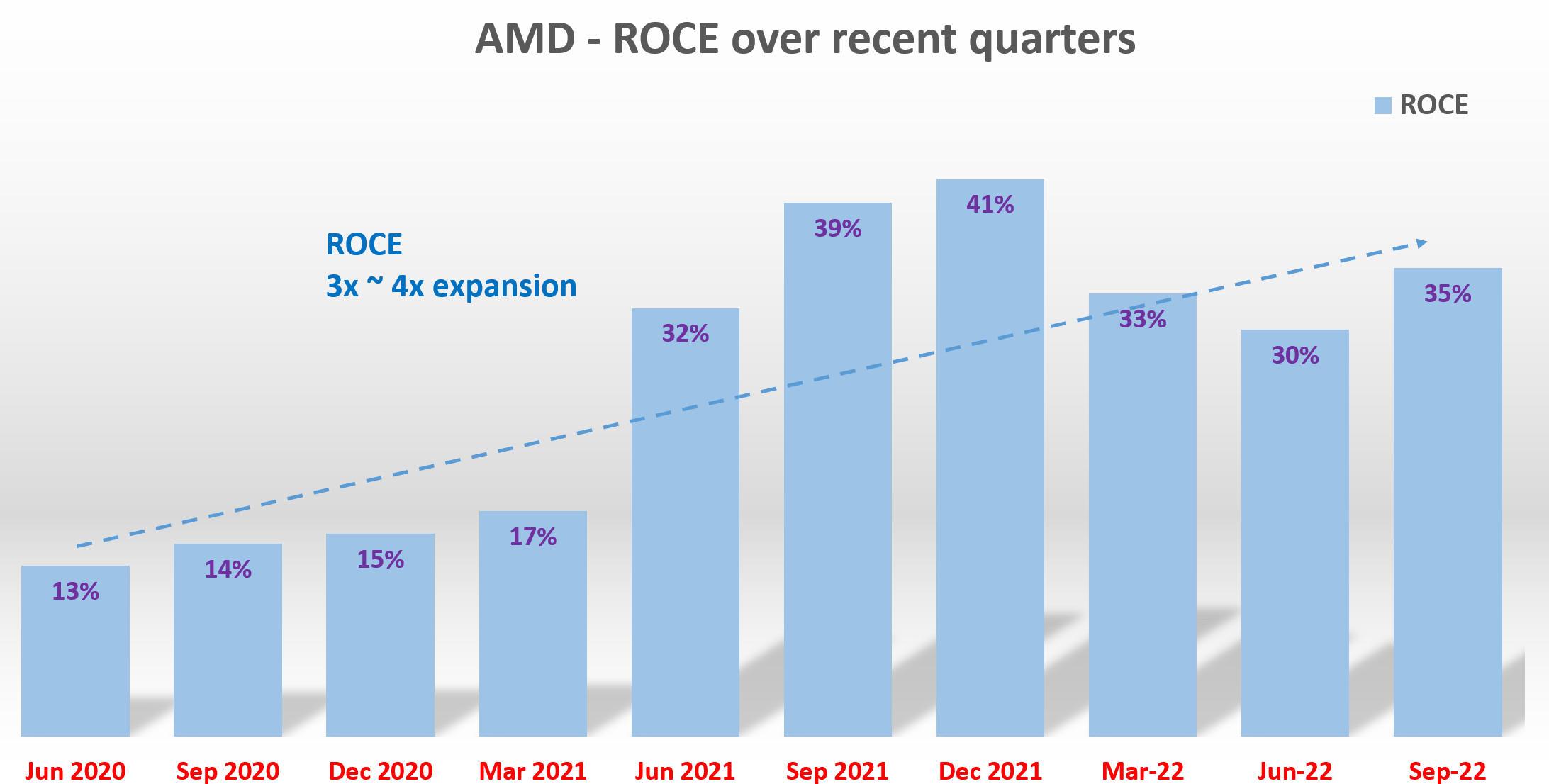

Next, I will show why I agree with AMD’s expectation that these acquisitions should be accretive to earnings (non-GAAP margins, non-GAAP EPS, et al.) during the first year. I will further argue that these earnings benefits are only 1st order effects and there are 2nd order benefits to be considered too. For the earnings benefit, I argue based on its ROCE (return on capital employed). And for the 2nd order benefits, I will base my argument on the MROCE (marginal ROCE) analysis.

And let me start with the ROCE. The graph below shows the ROCE for AMD in recent quarters on a TTM basis. Details are provided in my earlier articles. As seen, AMD’s ROCE sat around 13%~15% as recently as in 2020. Then its profitability expanded at an accelerated pace starting in the March quarter of 2021, a clear indicator of it passing a critical scale in my mind. All told, since then, its ROCE expanded by about three to four folds to the ~40% level in a short period of about 1 year. Currently, despite the headwinds aforementioned, its ROCE hovers around 35%, still about 3x higher than its 2020 level.

In the next section, I will examine the MROCE data to argue for these acquisitions’ 2nd order benefits.

Author based on Seeking Alpha data

Data center’s scale and scalability

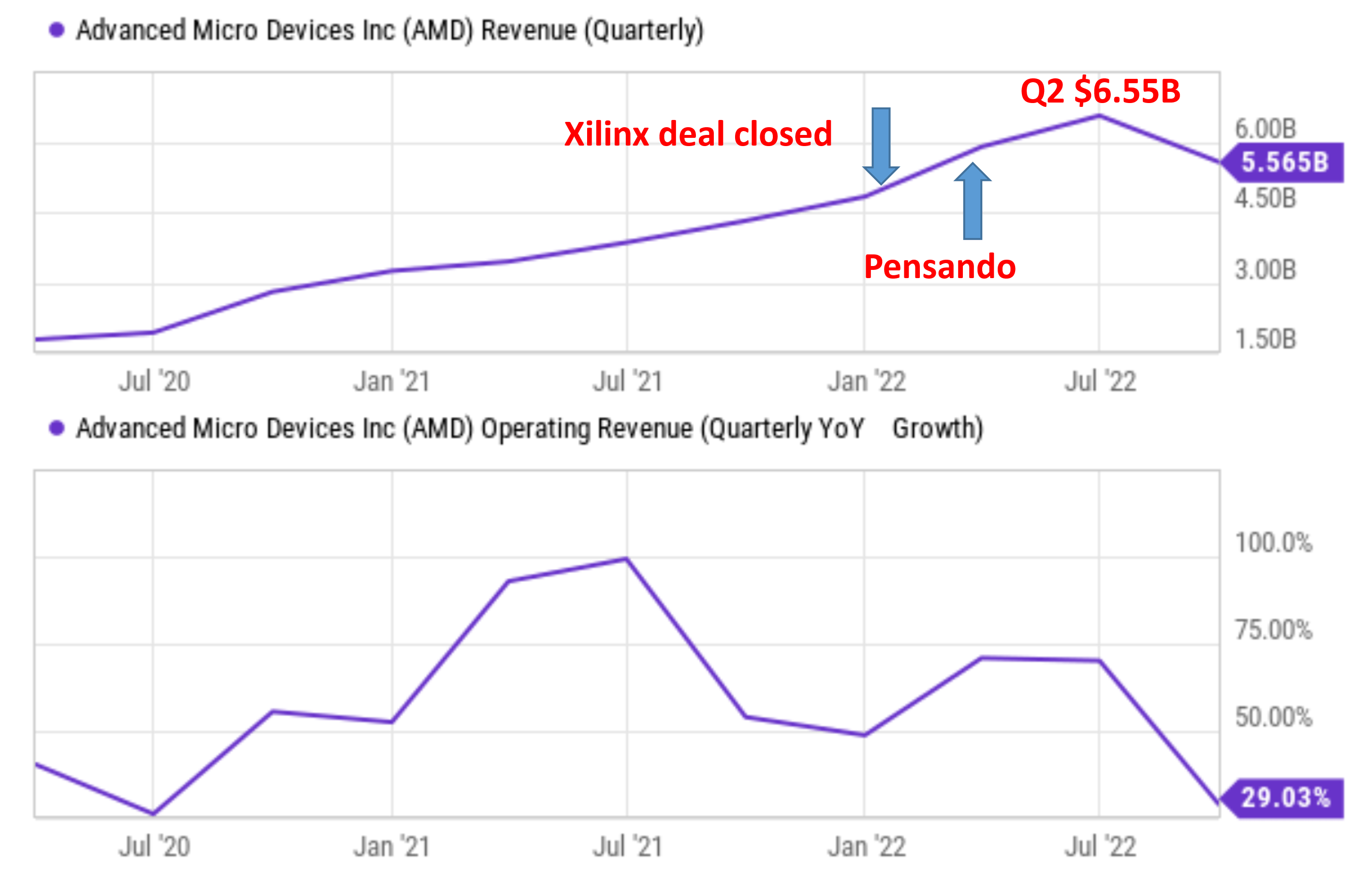

As aforementioned, the Xilinx acquisition was completed in Feb 2022 and the data below clearly show the synergistic benefits of this acquisition. The sale growth curve accelerated shortly afterward. Its YoY growth rates of quarterly revenues jumped to almost 100% from the already-rapid rate of 50% level before the acquisition. Then, it also completed its Pensando acquisition in May 2022. And again, you see that after a relatively short period of these acquisitions, AMD was able to monetize a good part of the synergies and its total revenues peaked at $6.5B during the June quarter of 2022.

Author based on Seeking Alpha data

Next, I’ll further illustrate the benefits of these acquisitions using the concept of MROCE (marginal ROCE). The MROCE concept is detailed in my earlier article:

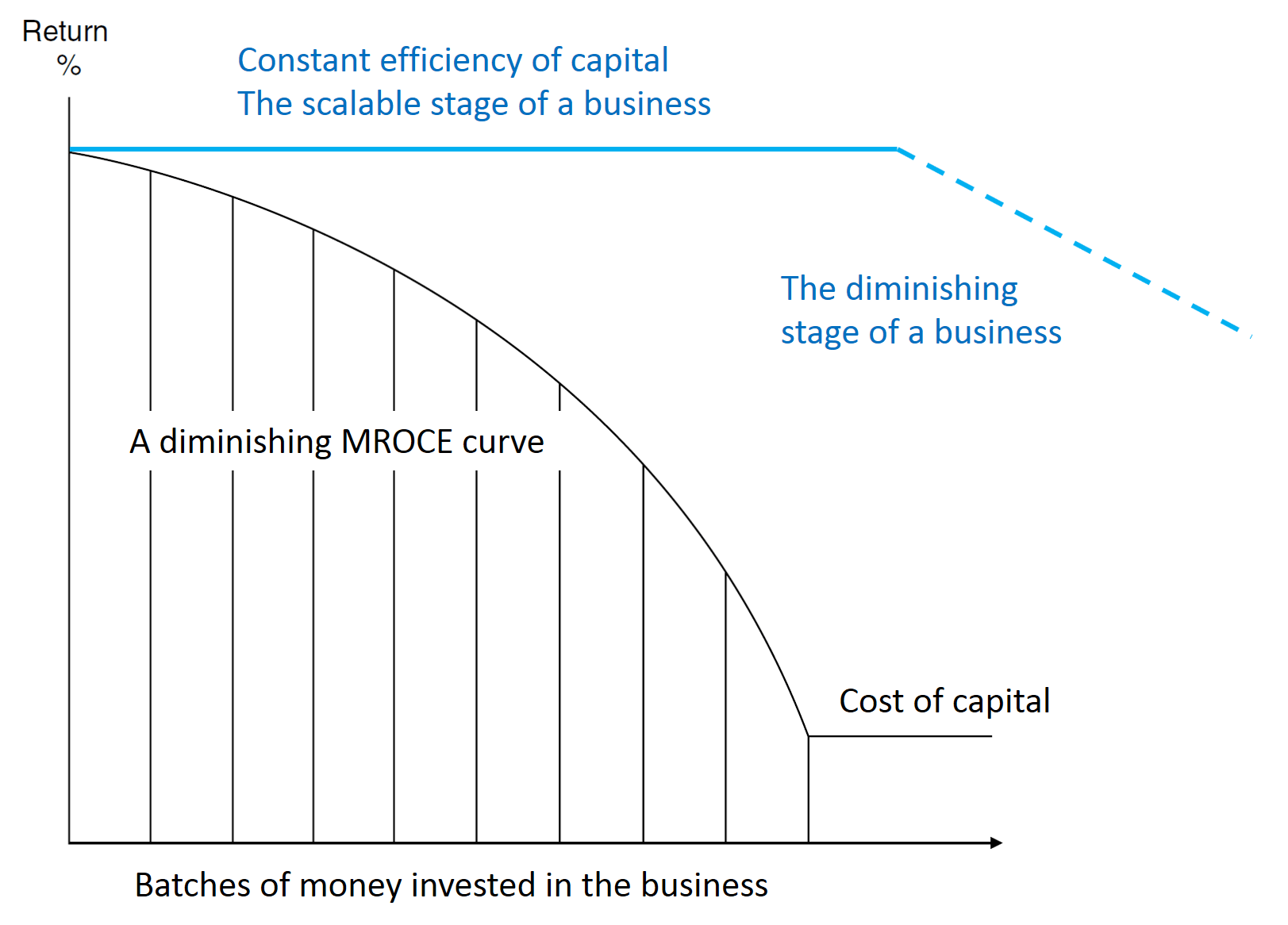

What the MROCE concept captures is a basic law in economic activities: the law of diminishing returns. A business will first invest its money in projects with the highest possible rate of return. Therefore, the first batch of available resources is invested at a high rate of return – the highest the business can possibly identify. The second batch of money will have to be invested at a somewhat lower rate of return since the best ideas have been taken by the first batch of resources already, and so on. And finally, the end result is a diminishing MROCE curve as shown.

Author

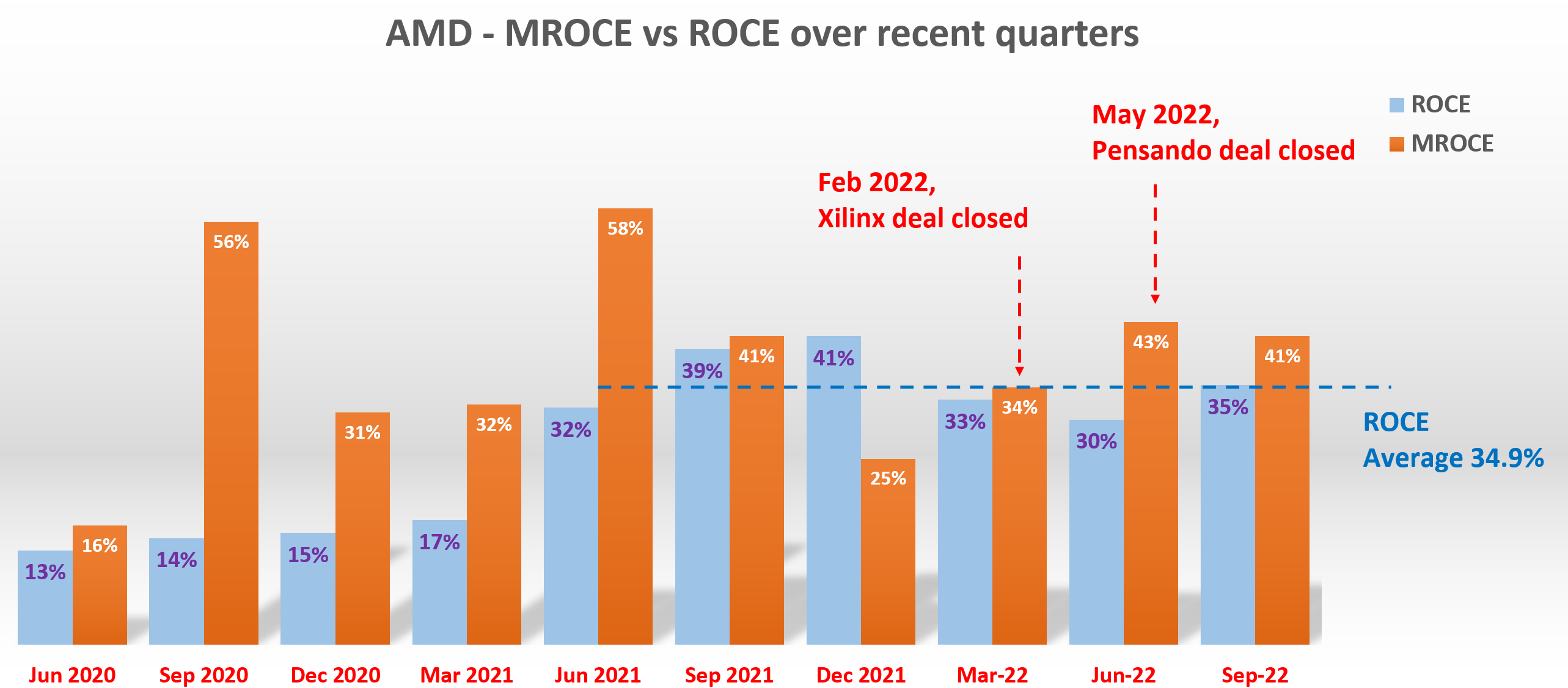

The MROCE results for AMD before and after these acquisitions are displayed in the plot below. The results were obtained by taking the derivative on the ROCE data shown earlier (hence the 2nd order effects) as detailed in my earlier article. Also, a running average was used during periods of abnormal fluctuations. Such running averages also make sense at a fundamental level because many capital projects may have a life cycle of more than 1 year.

The results indicate an expansion of MROCE since the acquisitions as seen. To refresh our memory, its ROCE has been averaging 30%~40% during 2022. And as you can see from the following chart, the average MROCE has been above 40% (43% and 41%, respectively) in the two quarters since the Xilinx deal was closed, higher than the average ROCE by a good amount.

Author based on Seeking Alpha data

Risks and final thoughts

To recap, AMD faced strong headwinds in 2022 and many of them will further persist in the near future. Many of its business segments had been weighed down by the global weakening PC demand and also inventory digestion in the chip sector. AMD’s CEO Lisa Su expected a double-digit demand decline per her following comments during a recent earnings report (slightly edited with the emphasis added by me):

…we have taken a more conservative outlook on the PC business. So, a quarter ago, we would have thought that the PC business would be down, let’s call it, high single digits. And our current view of the PC business is that it will be down, let’s call it, mid-teens. And that’s contemplated into our third quarter guidance.

However, overall, I see these issues to be only temporary. For the mid to long term, I see a robust growth curve ahead, especially in its Embedded and Data Center segments. A few key catalysts position AMD to resume rapid growth once the macro conditions improve. The gaming segment is poised to enjoy tailwinds given its relationship with game console leaders such as Sony and Microsoft. And the recent successful acquisitions of Pensando and Xilinx will spur growth in its strategic Embedded and Data Center segments. All told, I see the current concerns as overblown and the valuation contraction as overdone, providing a good GARP (growth at a reasonable price) opportunity.

AMD Q2 2022 ER

Be the first to comment