chonticha wat

Owning gold has required patience these last two years. After surging following the onset of COVID and peaking above $2,000 per ounce back in August 2020, gold has churned in the time since and is currently trading -15% below its all-time highs. Given these lackluster results the last couple of years, what would compel an investor to want to own gold today?

Portfolio diversification

From an asset allocation perspective, a primary appeal for owning gold is the diversification benefits it provides. For example, over the last nearly twenty years, the performance of gold has been virtually uncorrelated with that of U.S. stocks with a correlation coefficient of +0.07 (+1.00 is perfectly correlated, -1.00 is perfectly negatively correlated, and 0.00 is uncorrelated). Gold also has had a low positive correlation with U.S. Treasuries at +0.20. As a result, incorporating an allocation to gold within a broad asset allocation framework can lower overall portfolio risk over time as measured by standard deviation of returns.

Two-way hedge

Gold also serves as a safe haven for investors during periods of uncertainty. The yellow metal is typically regarded as an attractive hedge against inflation, but it has historically been mixed during periods of pricing pressure. This is due to the fact that when inflation becomes elevated, investors begin to anticipate central banks including the U.S. Federal Reserve will respond with monetary tightening including raising interest rates, which has a dampening effect on the gold price.

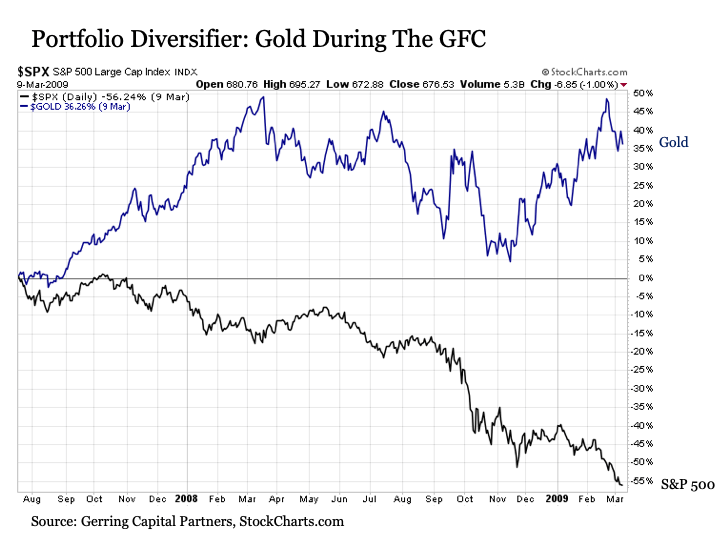

Instead, gold historically has served as a much more impactful portfolio hedge during periods of economic instability and uncertainty. A prime recent example was the performance of gold during the Great Financial Crisis. During the time when the S&P 500 Index plunged by more than -55%, the price of gold increased by as much as +50% (not without its own bouts of price volatility along the way it should be noted).

StockCharts.com

From a fundamental perspective, given that we may be at the early stages of what could become a more prolonged economic slowdown as the Fed continues to aggressively battle high inflation in an environment marked by ongoing shifts in the global geopolitical order, we are looking forward with no shortage of economic instabilities and uncertainties at least for the next couple of years.

Struggling substitute

Another development promises to provide an added boost to the appeal of owning gold going forward. For the last many years, a good number of investors migrated away from owning gold and opted instead to own cryptocurrencies instead as an alternative portfolio diversifier that some referred to as “digital gold”.

But the notion that cryptocurrencies could replace gold’s function as a safe haven hedge was always wildly misguided for several reasons.

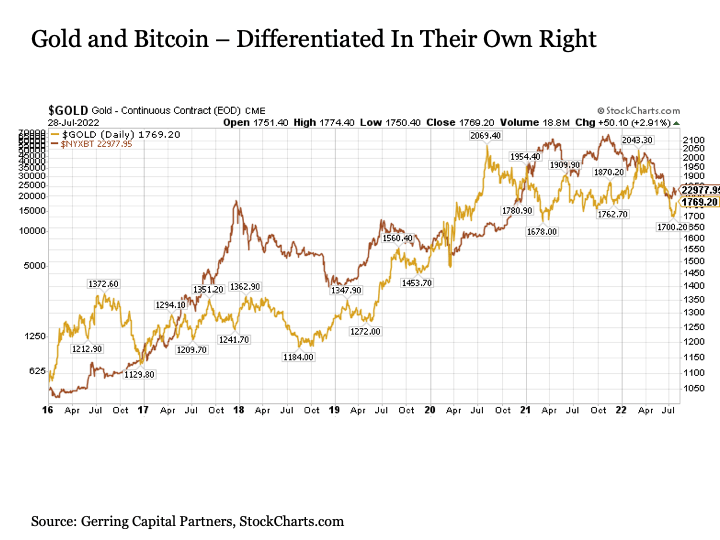

First, gold and cryptocurrencies trade with a very low correlation in their own right. For example, gold and Bitcoin (BTC-USD) over the last seven years have a returns correlation of +0.12, which is virtually uncorrelated.

StockCharts.com

If anything, a case could be made from an asset allocation, portfolio diversification perspective for owning both gold and cryptocurrencies given their low correlation with each other along with most other major asset classes. But I would not own cryptocurrencies for their own specific fundamental reasons (or lack thereof).

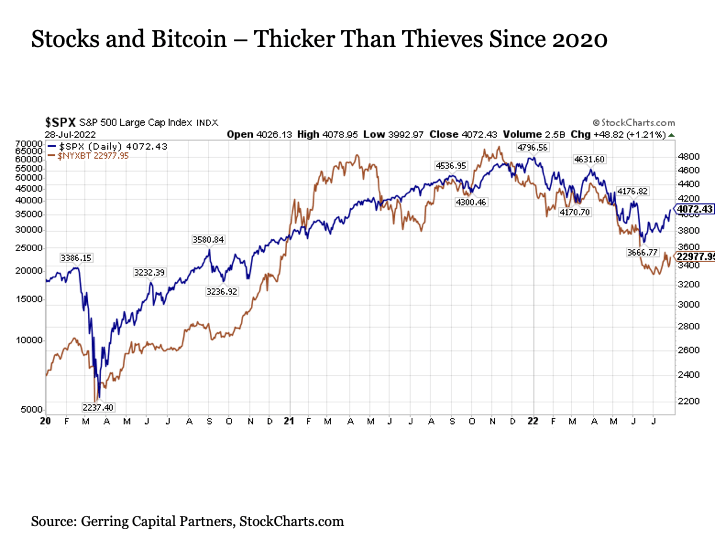

StockCharts.com

Next, unlike gold, cryptocurrencies do not have a track record of performing well during periods of economic uncertainty. Instead, cryptocurrencies have increasingly shown the propensity to trade with a relatively high correlation to U.S. stocks. For example, the correlation of returns between the S&P 500 and Bitcoin since January 2020 has been +0.62, which is notably high correlation. This is due to the fact that the cryptocurrency trade is just as dependent as stocks if not more so to the steady flow of liquidity into the market. If this liquidity dries up, both stocks and cryptocurrencies will likely struggle.

Unfortunately for cryptocurrency investors, they are discovering this high correlation with U.S. stocks the hard way in 2022. For while the S&P 500 Index is lower by -15% and gold only recently turned negative for the year to date at -3%, Bitcoin, which is regarded as the old stalwart in the cryptocurrency space, has fallen by more than -55%.

If anything, those safe haven seeking investors that migrated away from gold with the notion that cryptocurrencies were a comparable “digital gold” alternative may be inclined to migrate their way back to gold, which could help put a tailwind behind the gold price going forward.

Turning to the technicals

One of the challenges associated with evaluating gold on its fundamental merits is the fact that it does not generate cash flows. As a result, another way to evaluate the potential opportunities associated with gold is to employ technical analysis, which is for all intents and purposes the graphical representation of statistical information to guide and make more precise the investment decision making process. Technical analysis is not for everyone, but if something is being widely used and has a demonstrated track record of working and being useful, I want to incorporate it into my investment decision making process.

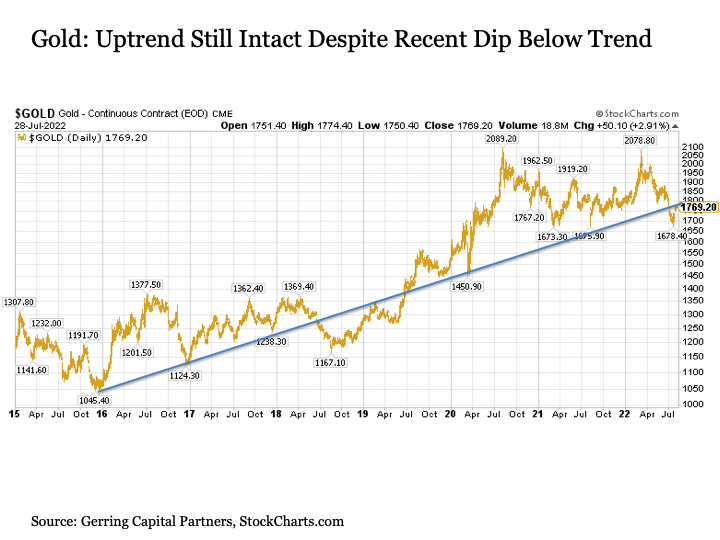

StockCharts.com

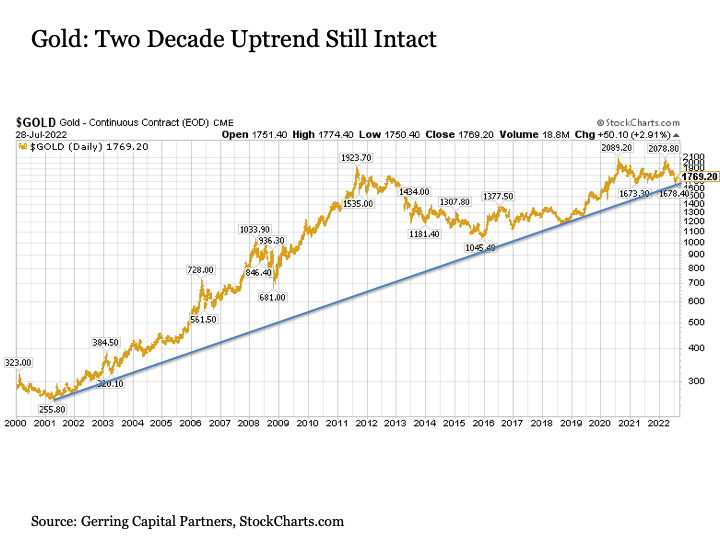

First, the uptrend in gold remains intact from the 2015 lows. Although the gold price recently edged below the upward sloping trendline, this does not mean support is necessarily broken. After all, we saw gold trade below trend for nearly a year from mid-2018 to mid-2019, yet gold eventually regained this support level and continued its advance to the upside.

StockCharts.com

Zooming out much further provides additional support for the long-term uptrend. While gold got way ahead of itself in 2011 and has spent the last decade effectively regressing to its long-term trendline mean. In recent years, gold has been trading close to trend as is effectively at trendline support today.

StockCharts.com

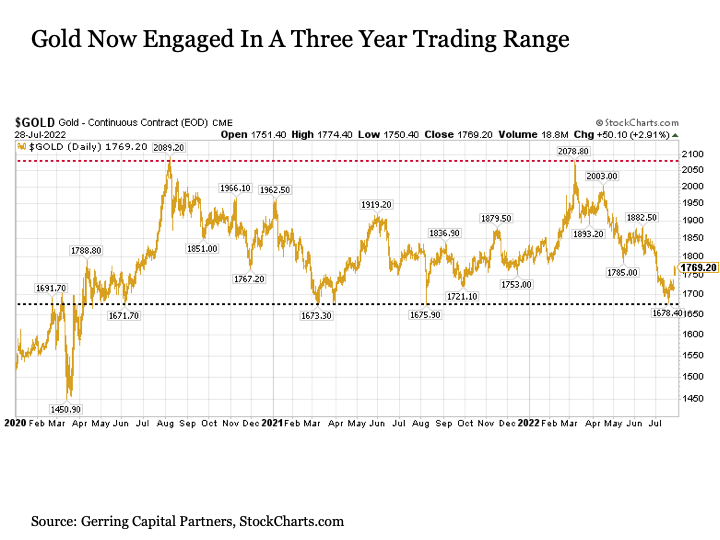

Focusing back in on the more recent period since 2020, we see that a well-defined trading range has formed for gold between $1,675 and $2,080 per ounce. And since March of this year, we have seen the gold price drift from the top end of this trade range to the bottom in July.

This is where the attractive opportunity presents itself for gold today from a technical perspective. Gold has since bounced strongly from its 1675 support, having already added $90 per ounce in recent weeks.

Having missed this initial bounce provides an added advantage, however, as it now provides a downside target to shoot against for those that may have a more short-term focus to their investment approach. In short, an investor buying today has a -5% cushion to the downside that they can utilize in establishing a downside protection strategy.

As for the potential upside, a return to the top of the trading range implies nearly +18% upside from current levels, which is attractive returns potential in any environment. Moreover, it is possible that gold could break out to the upside beyond 2080 going forward, particularly given the gathering economic fundamental tailwinds. This scenario would enable a full resetting of the allocation with gold having broken out into a higher trading range, but this is a possibility to start to consider once gold makes its way back to the upside first.

Bottom line

Gold offers appeal for investors in the current market environment. Not only is the technical set up favorable, but economic and market developments also support a higher gold price. While gold is widely regarded as being more volatile and unpredictable relative to stocks, it is also worth noting that along with the favorable upside return potential at present, the risk associated with gold as measured by standard deviation has been only three-quarters that of U.S. stocks as measured by the S&P 500 Index over the last two decades, which is an added plus.

It should also be emphasized that any allocation to gold should be measured with a broader asset allocation framework. Barring those that are experienced investing in precious metals and have a high conviction in the allocation, the typical weighting to gold in a broader asset allocation is around 5%, which is reasonable. I will disclose that I currently have a 7% portfolio weight to gold, which reflects a measurable overweight to gold within my current broad asset allocation framework.

Whether gold is suitable for your investment strategy and at what weight is ultimately dependent on one’s own specific return expectations and risk tolerance and should be considered carefully and deliberately as a result.

Be the first to comment