photovs/iStock via Getty Images

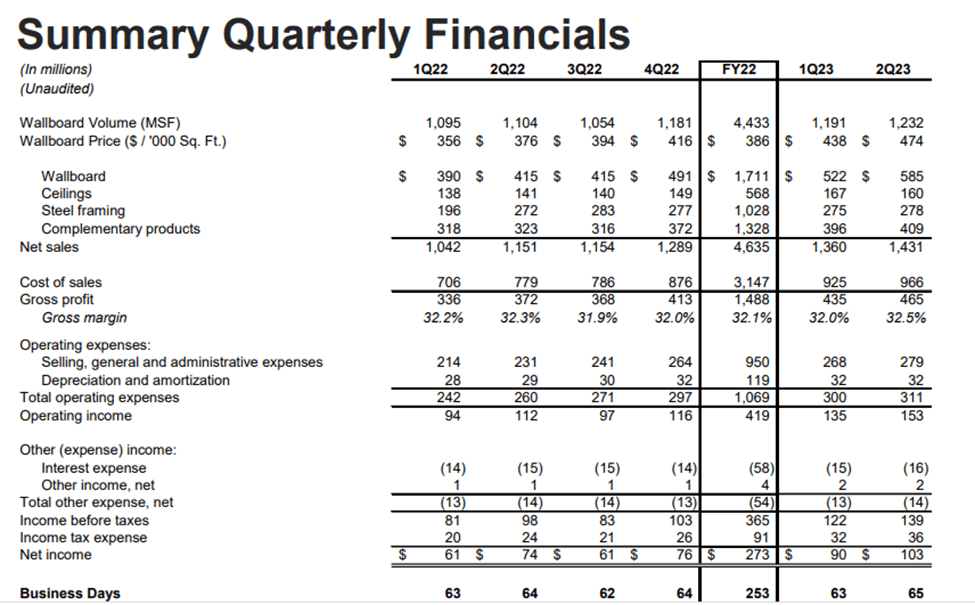

GMS Inc. (NYSE:GMS) reported an EPS of $2.79 in Q2 2023 beating Wall Street estimates by $0.45. Revenues in the quarter came in at $1.45 billion, indicating an increase of 24.37% (YoY). It beat consensus estimates by $69.20 million. The company’s organic sales grew 22.2% (YoY) driven primarily by product inflation and year-over-year volume growth in inventories like wallboard, ceilings, and complementary construction products. GMS Inc.’s stock price is up 17.17% in the last 6 months, indicating strong momentum.

Thesis

GMS Inc’s entry into New York City with the acquisition of Tanner Bolt and Nut Inc will help the company to execute its strategic growth expansion as well as its complementary product base. GMS also seeks to improve its cash flow by tapping into the supply chain dynamics including e-commerce and other B2B processes. The company is set to realize more benefits of scale from Greenfield opportunities and more AMES stores into 2023.

GMS has its headquarters in Tucker, Georgia with up to 297 distribution centers or branches across the U.S. and Canada. Entry into New York City means that the company intends to capitalize on an underpenetrated location with a higher market share. Firstly, the global gypsum board market was valued at $26.60 billion in 2021. It is forecast to reach $38.19 billion by 2028 growing at a CAGR of 5.3% over the period. The bulk of this growth is expected to emanate from North America, followed by Europe and Asia. Thus additional investment in North America is a key step toward the GMS expansion agenda.

GMS has tried to balance operations from a metropolitan statistical area (MSA) perspective. As noted in its Q2 2023 earnings report, the company did not have representation in New York and Utah (in the U.S.), so having distributions in these two centers remained a vital priority. In Canada, GMS is found in all major locations except Montreal and areas around the Eastern Provinces. According to me, having a GMS outlet in Montreal and other parts of Canada will be a top priority come 2024 since the country is home to Nova Scotia- a global frontier in gypsum mining.

The acquisition of Tanner Bolt and Nut as a subsidiary of GMS brings on board an additional revenue stream from the sale of safety and related construction implements, tools, and fasteners. It has been in operation for close to 44 years after it was founded in 1979. Apart from the four metro area locations acquired from Tanner, GMS will also acquire a new Greenfield location in Brooklyn. From here it will increase its supply of ceiling products, especially in the Northeast through its broader relationship with USG.

While making this announcement, GMS CEO, John Turner stated,

“We are pleased to take this first step into such a significant market. With Tanner’s focus on tools and fasteners, these additions, along with the establishment of several new greenfield yard locations and AMES stores over the last several months, represent our continued commitment to the execution of our strategic priorities of platform expansion and Complementary Product growth.”

These accretive acquisitions and Greenfield opportunities have been a top priority for GMS. The company has wanted to expand its product assortment since Q1 2022. As of Q2 2023, GMS had opened 5 Greenfield yards as well as 9 AMES store locations. Organic sales in the quarter rose 22.2%, while net sales were up 22.5% (YoY). The company now has one additional selling day as compared to the Fiscal Year ending 2022. In Q2 2023, this additional selling day resulted in net sales increasing 22.5% (YoY) and daily organic sales were up 20.3%. This additional day brings the total quarterly business days to 65, up from 64 a year earlier.

GMS

As seen, GMS’ performance included a 24% (YoY) rise in net sales and a 14.7% (YoY) growth in operating income. GMS also increased its net income by 68.85% (YoY) indicating stable progress into Q4 2023.

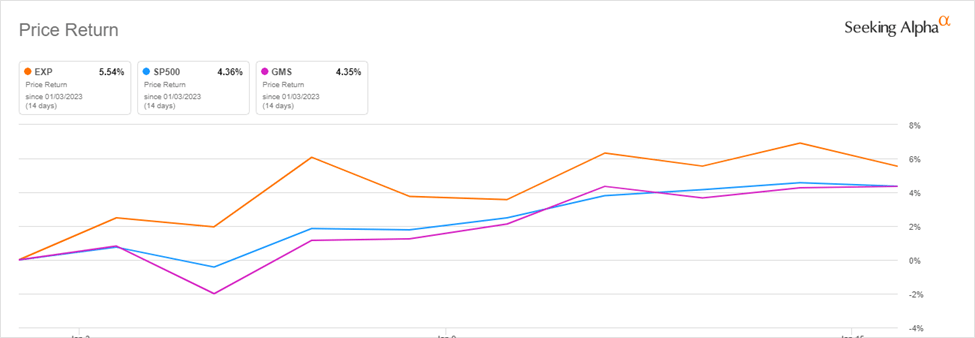

GMS is trading at +4.35% (YTD), while Eagle Materials (EXP) rose 5.54% (YTD). They are moving at par with the S&P500 which also gained 4.36% (YTD).

Seeking Alpha

Sector performance assessment

Sales from the US residential space according to GMS Q2 2023 earnings report shot 34% (YoY) guided by the growth of the multifamily housing units. Multifamily real estate during the pandemic times has been described as a hedge against inflation as it is largely seen as a need-driven asset. Sales from single-family units were also up 29% (YoY) despite the sector having some backlog into 2023. I can foresee a decline in demand in selling activities within the single-family housing units as compared to multifamily units, but the decline may be offset by an improvement in commercial construction in Q3 2023.

Sales from commercial units gained 17% (YoY) with additional constructions expected in the near as North America continues to recover. If we factor in the aspect of favorable pricing which GMS has always championed and an activated residential construction segment, we will see quicker partial offsetting of negative currency translation currently plaguing the sector.

GMS recorded $584.6 million in wallboard sales up 41% (YoY) in the quarter representing a 38.9% sales growth (on a-per-day basis). The undertones of this growth included a 28.9% increase in price/ mix and a 9.9% gain in volume.

Q2 2023 saw organic sales of wallboards grow 41.4% (YoY) with the sales up 39.2% (on a-per-day basis). It consisted of a 30% rise in price/ mix and volume gained 11.4% (YoY).

Steel-related sales and volume declined 7% (YoY). I expect steel framing as well as the pricing of the ceiling grid to slow down into Q3 2023. The decline is organic and will be driven by the rise in inflation especially due to the price of steel.

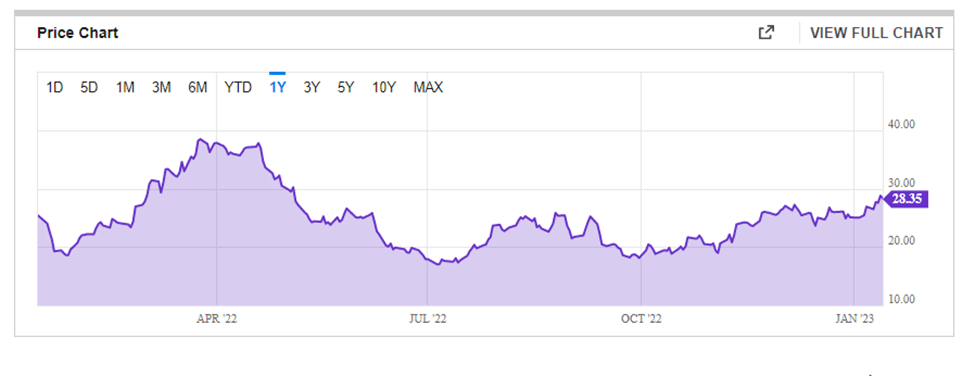

YCharts

A ton of steel in the US now costs $28.35 up 18.08% (YoY). However, price readjustments made GSM realize $278.2 million in steel framing sales indicating a 2.3% rise (YoY). We are likely to see an influx of “stick-built lower-rise structures” into the market that may lead to less steel framing being incorporated especially in office units in 2023.

Online sales will also continue to be a game changer for GMS. As of Q2 2023, GMS recorded that more than 80% of its top 100 customers were signed up online. Out of this percentage, about 60% were monthly users of the e-commerce system. Into 2023, GMS intends to leverage its production scale and incorporate technology to improve customer service and raise profit. I am looking at aspects such as e-ordering, online delivery status updates/ notifications, and pictures of consignments.

In its Q2 2023 earnings report, GMS stated that customers had the opportunity to check product pictures and ascertain that they were dispatched after ordering. However, sales from e-commerce stood at a fair level of $65 million (on-a per-month basis), indicating that there was room for improvement.

Risks to Consider

The cost of revenues for GMS has risen 24.09% (YoY) to $966.3 million as of October 2022. Total operating expenses have also grown 20.7% (YoY) owing to the increase in price/ mix of basic raw materials.

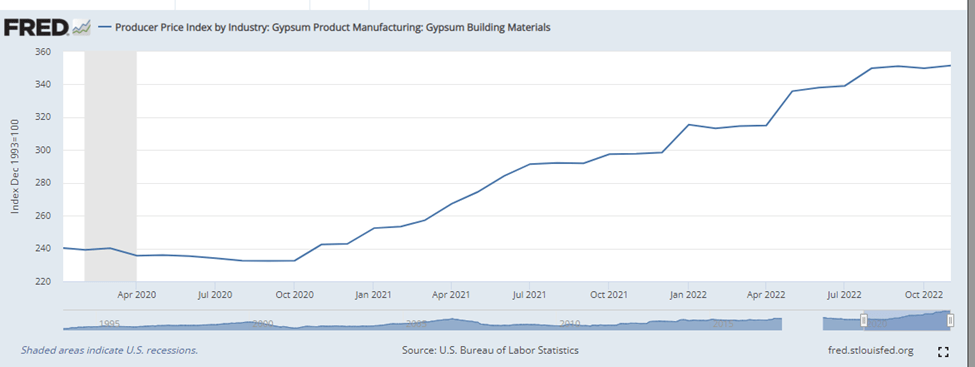

US Census Bureau

The producer price index for gypsum indicates the building commodity is trading toward its all-time high of 360. Both GMS and Eagle Materials, which are national producers of gypsum wallboards, have been forced to review their prices. This increase in the cost of goods may raise prices and thereby affect demand. As mentioned earlier, we are likely to see an influx of “stick-built lower-rise structures” as an alternative to steel framing.

Overall, the housing market is pegged on the inflation rate that closed 2022 at 6.5% having fallen from 7.1% in November 2022. Despite the high margin, I expect the inflation rate to continue decreasing due to the slowdown in monthly forecasts.

According to the US Census Bureau residential construction as of November 2022 stood at $868 billion about 0.5% below the consensus estimate of $872.4 billion. This decrease indicates a slight decrease in private housing construction demand. The Bureau is set to release the next construction spending estimates in February 2023.

In its Q2 2023 earnings report, GMS indicated that there was a slowdown in the development of new single-family permits and starts that affected building activity in the quarter. Still, the company is looking forward to a strong residential market into 2023 with longer-build cycles.

Bottom Line

GMS is positioning itself with more product offerings including complementary products. The company’s acquisition of Tanner Bolt and Nut as well as new Greenfield locations is expected to drive growth in the remaining section of FY 2023 while still lowering the net debt leverage. GMS is also investing in technology to improve work automation and raise productivity. The stock is trading 9% below the 52-week high of $58.73 and may outperform comparable stocks such as EXP in the long term. For these reasons, I recommend a buy rating for the stock.

Be the first to comment