Torsten Asmus

Article Thesis

Global X Funds’ Global X NASDAQ 100 Covered Call ETF (NASDAQ:QYLD) is a specialized income-focused fund that currently offers a hefty 14% dividend yield based on the payments that it made over the last year. Before jumping on this yield, investors should consider the downside of QYLD’s strategy — capped upside — and the fact that declining equity market volatility could result in lower dividend payments in the future.

QYLD’s Unique Strategy

Tech is generally seen as a high-growth industry. Not surprisingly, average valuations are high, and due to a focus on reinvesting for growth, many tech stocks offer low or no dividend yields. There are some outliers, but overall tech is not very welcoming for income investors.

And yet, the Global X NASDAQ 100 Covered Call ETF is a high-yield vehicle despite its tech focus. That’s possible thanks to a unique strategy. The fund has a goal of replicating the performance of the CBOE NASDAQ-100 BuyWrite V2 Index. This index shows the performance of a theoretical portfolio that owns the NASDAQ 100 companies and that sells covered calls on these companies. QYLD’s performance is close to the performance of the CBOE NASDAQ-100 BuyWrite V2 Index, with its expense ratio making a small difference.

The writing of covered calls allows QYLD (and the underlying index) to generate income via the option premiums that the seller (or writer) of the call option receives. Those option premiums vary over time and depend on a couple of factors, including (assumed) volatility. Generally, selling options with a short time span until expiry generates higher option premiums. QYLD (and the underlying index) use 1-month call options for this strategy, which results in hefty option premiums received over time — which is why the dividend yield is this high, despite the fact that the tech stocks themselves oftentimes offer no dividend or only very small ones to their owners.

Of course, every strategy has a downside, and that also holds true for QYLD. While selling covered calls generates additional income over time, this strategy also caps the upside of the investment. Let’s look at an example:

Let’s say an investor owns 100 shares of Advanced Micro Devices (AMD), worth $6,700 at the time of writing. If the investor sells a call option with an expiry date of February 10, 2023, with a strike price of $70, the premium received would be around $3.50 per share or $350 in total. While that would make for a very nice cash-on-cash return, considering it’s only a 1-month time frame, the upside of the investment would be capped. In case AMD was to rise to $75 or $80 over that time frame, for example, the investor would still only receive the $70 when shares get called away (which would happen in this scenario).

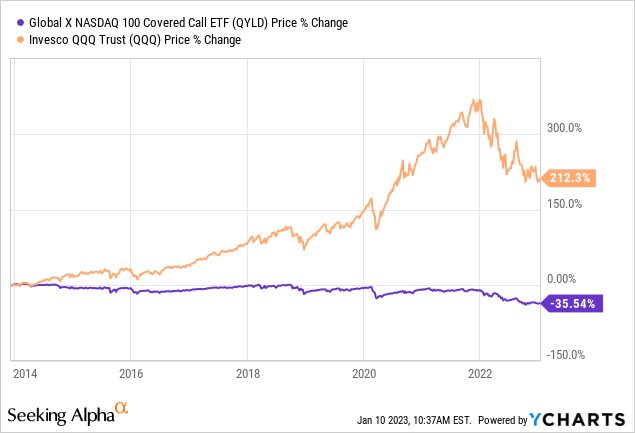

QYLD’s strategy of selling covered calls on tech names thus limits the upside potential on these tech shares — when they rise too much or too fast, they get called away, and QYLD has to enter a position in the same stock at a higher price. On the other hand, QYLD continues to hold on to these tech names when share prices decline. In other words, QYLD’s upside is limited, while its downside is not limited — there thus is a downward bias when it comes to QYLD’s net asset value, and thus also its price:

Since QYLD started trading, its shares are down by more than one-third. Meanwhile, the NASDAQ 100 has experienced a massive 210% gain over the same time frame, even following the hefty pullback over the last year. At the beginning of the year, QQQ was ahead by around 350% , while QYLD was still down compared to when it started trading.

Of course, QYLD’s share price underperformance versus the broad tech market is partially offset by QYLD’s much higher dividends. But even on a total return basis, where dividends are included, QYLD has underperformed QQQ substantially — QYLD is up 67% since late 2013, while QQQ has offered a total return of 240% over the same time frame.

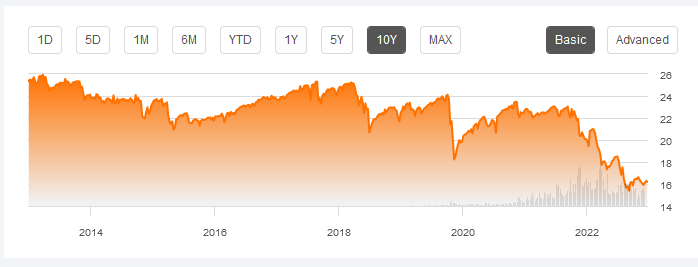

We can summarize that while QYLD offers a very high dividend yield, that dividend yield comes at a real cost: Due to its unique strategy of selling short-dated covered calls, QYLD’s upside is capped and its share price and NAV have a tendency to decline, even during times when the tech sector experiences steep share price gains. I do believe that it is unlikely that this will change meaningfully going forward — it’s a built-in mechanic of how selling short-term covered calls works. Investors should thus expect that QYLD will continue to underperform the tech industry massively on a share performance basis. Even further capital erosion seems likely, as there is a clear trend for that since QYLD began trading:

Seeking Alpha

The above chart shows that the highs that QYLD hit shortly after it started trading were never hit again. At the same time, the above chart shows that QYLD offers very little protection during times when the tech industry pulls back, such as in 2022. QYLD experiences substantial drops during these times, but does not recover/rise when the tech industry performs well, which is an important issue that investors should consider before putting money into QYLD.

QYLD’s Dividend: Massive Yield But Volatile

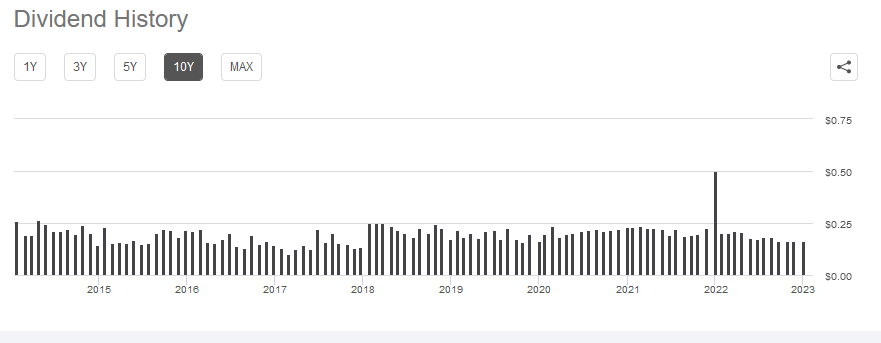

Based on the dividend payments that QYLD has made over the last year, the dividend yield is currently very high, at 14%. But investors should note that there is no guarantee that the forward dividend yield is this high as well. In fact, dividends have declined over time, both over the last year and since the ETF started trading:

Seeking Alpha

While the regular monthly dividend was as high as $0.26 in 2014, dividends have pulled back over time. Over the last twelve months, QYLD has paid out $2.19 per share, which pencils out to $0.1825 per share per month.

The most recent dividend declarations were even smaller, however, as QYLD paid out $0.16 per share per month for the last three payments. Annualized, that makes for $1.92 per share, which translates into a dividend yield of 12% at current prices. While that is still a very elevated dividend yield, the downward trend in dividend payments is not a positive sign. Dividend payments have declined, at least to some extent, due to principal erosion since the ETF started trading. Since QYLD’s share price and net asset value have pulled back, an unchanged return on its net asset value results in declining profits, and thus also declining dividends.

There are other variables at play on top of that, such as volatility in equity markets. Increased volatility results in higher option premiums, which is beneficial for QYLD’s dividend, whereas declining volatility results in lower option premiums, all else equal, and thus causes lower dividends.

Due to the aforementioned headwinds for QYLD’s net asset value — a capped upside and no downside cap — it would not be too surprising if net asset value continues to decline in the long run, as it has done for many years. That could cause further dividend reductions — not at a hefty pace, but it seems quite possible that per-share dividends will be lower five or ten years from now. QYLD thus is not a suitable dividend growth investment at all, I believe, although its dividend yield is still pretty high.

Is QYLD A Good Investment?

A tech investment with a double-digit yield sounds great, but investors shouldn’t rush into QYLD. The underperformance versus the uncapped QQQ is dramatic, and dividends have been trending down instead of up. While QYLD offers a compelling dividend yield and will likely do so for the foreseeable future, I do not deem it a great investment due to its sub-par total returns and principal erosion, even during the last decade — which was great for tech stocks.

Be the first to comment