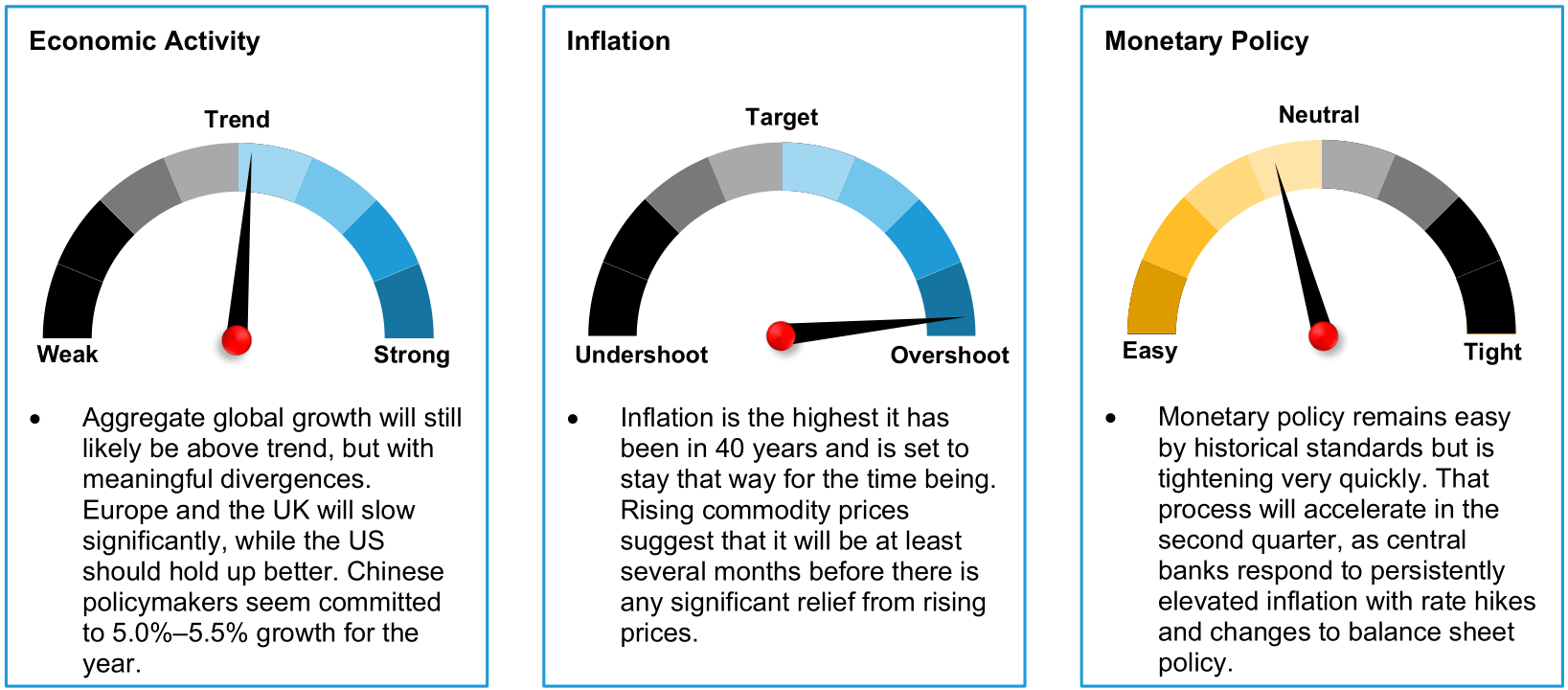

The Macro Picture

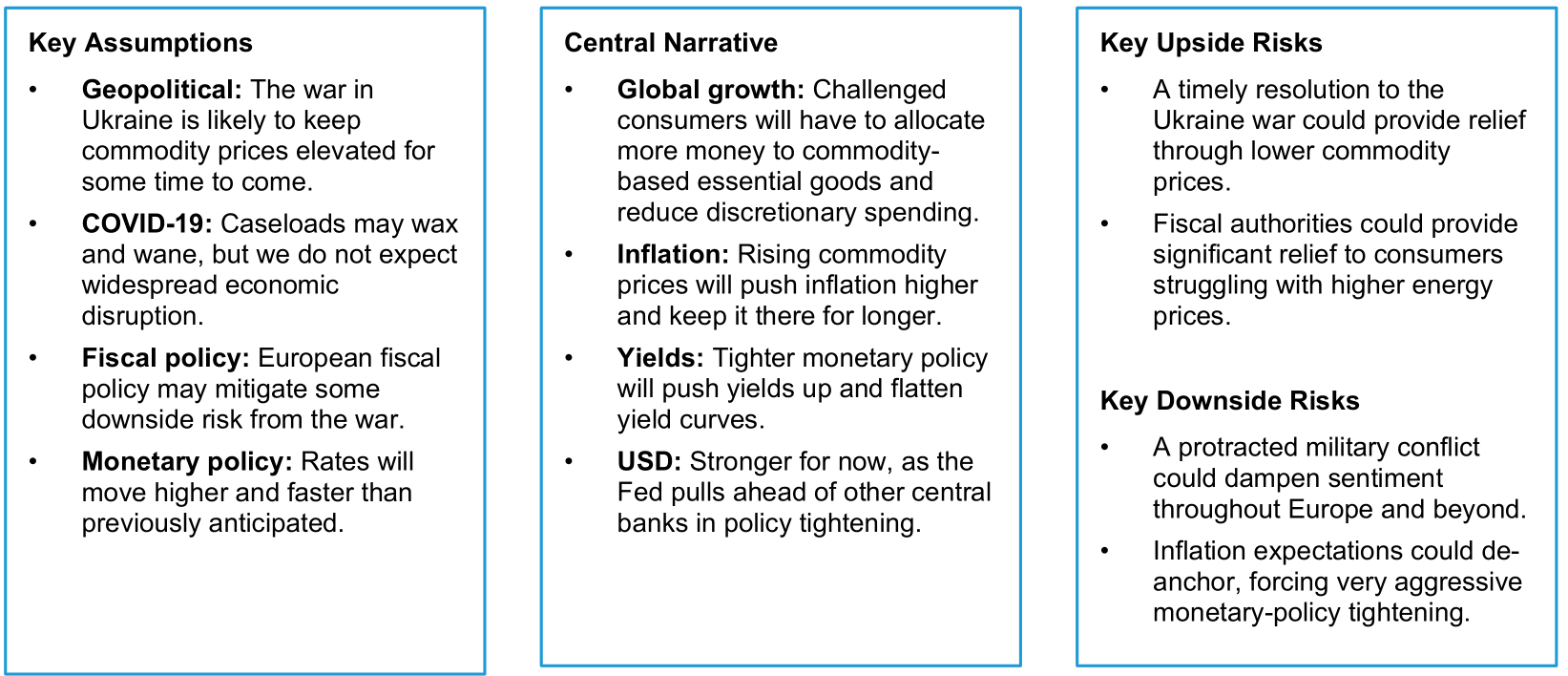

Just as the global economy was on the cusp of recovery from the COVID-19 pandemic, the world faces a second shock in the Russian invasion of Ukraine. As with any geopolitical risk event, the situation can change rapidly, making forecasting the economic outlook particularly difficult. These are uncertain times. More often than not, the global economy can shrug off geopolitical disruptions in fairly short order and with minimal long-term impact. That said, the direction of travel emerging from the ongoing crisis is clear: growth will be lower than previously expected and inflation higher.

The magnitude of the impact on growth and on inflation will be determined by how much energy prices rise and how long they stay high. Consumer demand for food and energy-related commodities is largely inelastic: higher prices for food and gasoline won’t reduce demand for those necessities, but will instead force consumers to spend less on other goods and services, slowing growth more broadly. The longer it takes for commodity prices to find a new equilibrium, the greater the downward pressure on global growth.

We don’t expect the war in Ukraine to impact every country identically. Instead, the impact will fall disproportionately on the European economy and some emerging markets with significant exposure to Russia and Ukraine. Geographical proximity and non-commodity trade linkages are a clear transmission mechanism between the war and the economic outlook in Europe. So is the reliance of Western Europe on commodity exports from both Russia and Ukraine; roughly one-third of Western Europe’s natural gas comes from Russia. The growth rate of real household income in Europe was already negative in year-over-year terms before the war; with the spike in energy prices, households will find it even harder to maintain their spending levels. We think Europe’s economy is more likely than not to slip into recession in the next few months unless the war ends soon. European fiscal authorities may be able to cushion the blow to consumers somewhat with fiscal support. If delivered in sufficient size, it could ease growth worries.

The outlook is less grim the further one gets from Eastern Europe, though the knock-on effects of the war will still be felt. Rising energy prices come at a particularly bad time for the global economy. Inflation is already at multi-decade highs in the US and many other countries, and rising energy prices will not only push inflation higher but also increase the risk that inflation expectations come unhinged. That development would make the ongoing inflation spike last longer, forcing a more aggressive monetary policy response.

As if that risk weren’t enough, the war, economic sanctions and the associated rise in energy costs are likely to exacerbate global shipping impediments, which had only just started to recover from the pandemic. As a result, any relief from the easing of supply- chain constraints is now further away than it appeared only a few weeks ago. Developments in China suggest the same. The zero- tolerance policy for COVID-19 cases still in place there has prompted lockdowns in major cities with the potential for significant impacts on global trade. That drag will further delay the supply chain recovery.

All these developments point to higher inflation, and we expect most central banks to continue tightening monetary policy, even as consumers face a hit to real incomes from rising energy prices. Policy tightening during an energy-induced supply shock runs contrary to the monetary policy lessons of the past few decades, but with inflation already elevated, this is what we expect the Fed, Bank of England, and many emerging market (EM) central banks to do.

The Fed started tightening in March, and we expect rate hikes at each policy meeting for the next several months—and a start to balance-sheet reduction. The Bank of England will likely continue raising rates, too, though the UK growth outlook is deteriorating rapidly, suggesting to us that the tightening cycle there will be less sustained than the Fed’s. Other major central banks, from New Zealand to Canada and throughout the emerging world, are also likely to start or keep raising rates—with only the Bank of Japan (BOJ) and European Central Bank (ECB) the likely exceptions among major players. As a result, we expect interest rates to continue rising and yield curves to flatten further, while equity and credit markets are likely to remain volatile in the coming weeks and months.

While recent developments point almost uniformly in a negative direction, perspective remains important. The reopening from COVID-19 pushed economic growth well above its long-term trend globally, and US households in particular have accumulated a reservoir of savings that will allow them to smooth consumption through trying times. That should truncate the downside risks and limit the scope of the economic disruption. A slowdown need not be a disaster. Monetary policy may be tightening, but it’s tightening from very accommodative levels that should still provide ongoing support. And history suggests that geopolitical events typically don’t disrupt the economy for very long.

As long as the tension in Ukraine resolves in the coming months, the hit to growth is likely to be temporary rather than permanent, and the disruption to the economic order much smaller than those of the past two years. But that’s a big if—the dominant theme for the time being is uncertainty.

The Global Cycle for 2Q:2022

Global Forecast

Forecast Overview

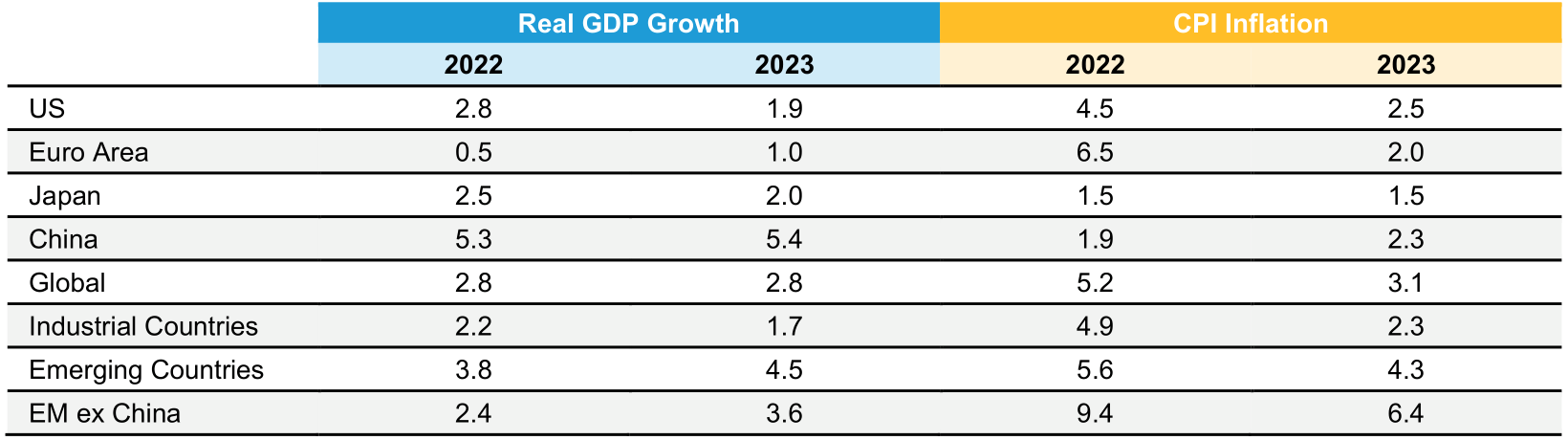

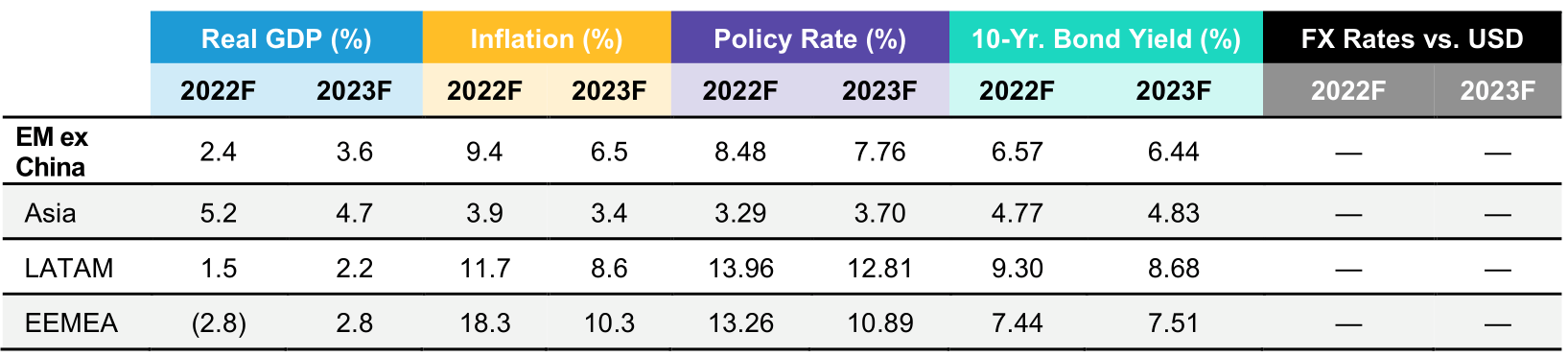

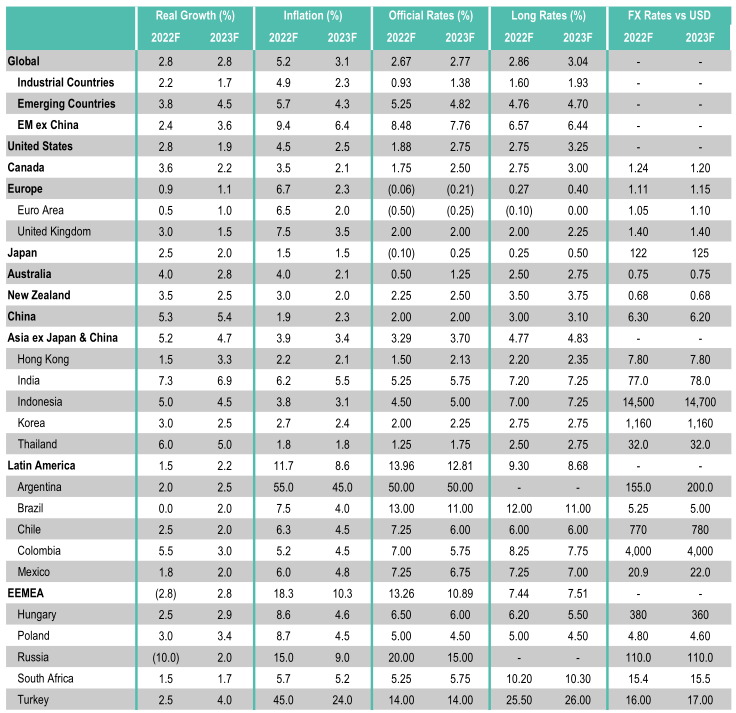

AB Growth and Inflation Forecasts (Percent)

As of March 31, 2022 Source: AB

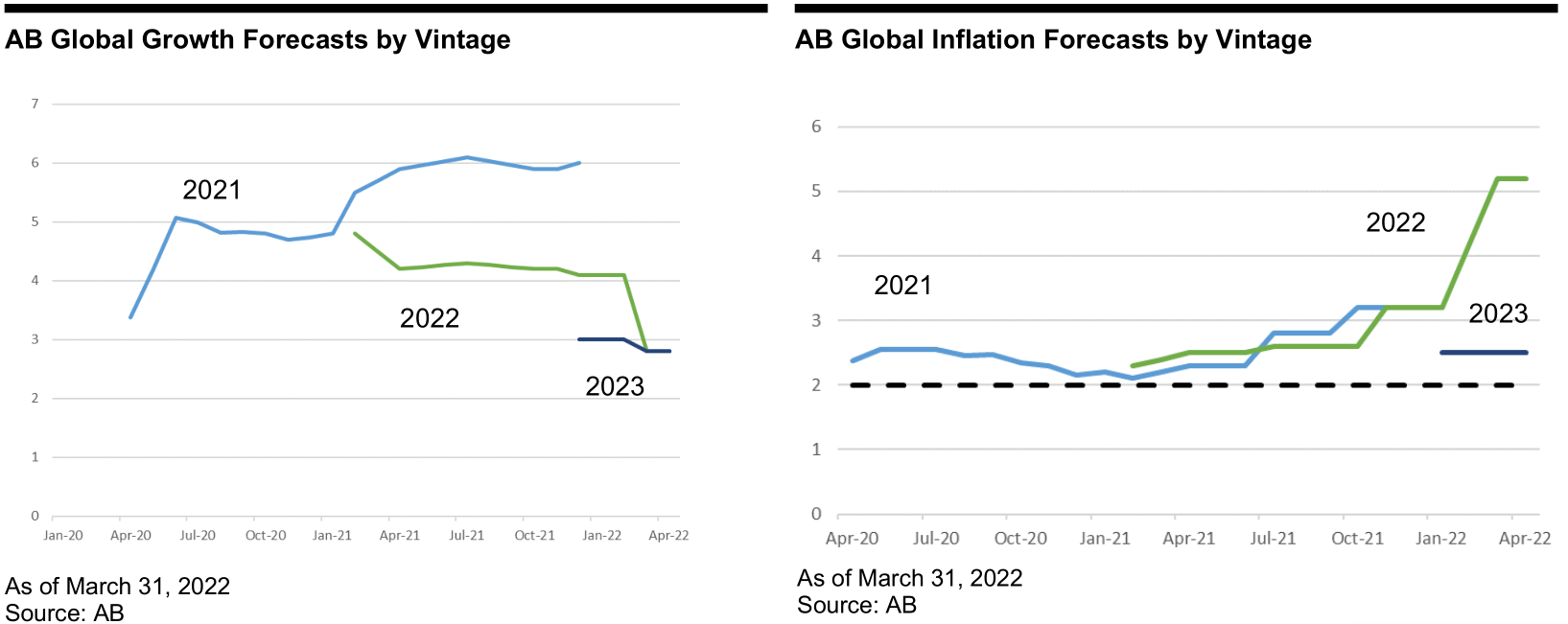

Forecasts Through Time

Outlook

- The war in Ukraine doesn’t have a large direct impact on the US economy, but the probability that commodity prices will stay elevated and supply-chain healing will be further delayed makes inflation likely to go higher and stay there longer than previously expected.

- More persistent inflation will translate into tighter monetary policy: the Fed is likely to raise rates sharply in the next few months to keep inflation expectations from becoming unanchored.

- Rising prices for daily necessities leave households with less disposable income. That suggests slower growth ahead, though a significant reservoir of untapped savings built up during the COVID-19 crisis should enable a gradual deceleration rather than a sudden stop. We expect growth to slow, not collapse.

Risk Factors

- Persistent geopolitical tension could push commodity prices still higher, taking inflation up and growth down by more than we expect. Alternatively, a rapid resolution to the war could ease tension and boost the outlook.

- It appears likely, based on the leading edge of the data, that COVID-19 infection rates are set to rise again in the coming months. We don’t expect a significant economic disruption but can’t rule out that outcome altogether at this stage.

Overview

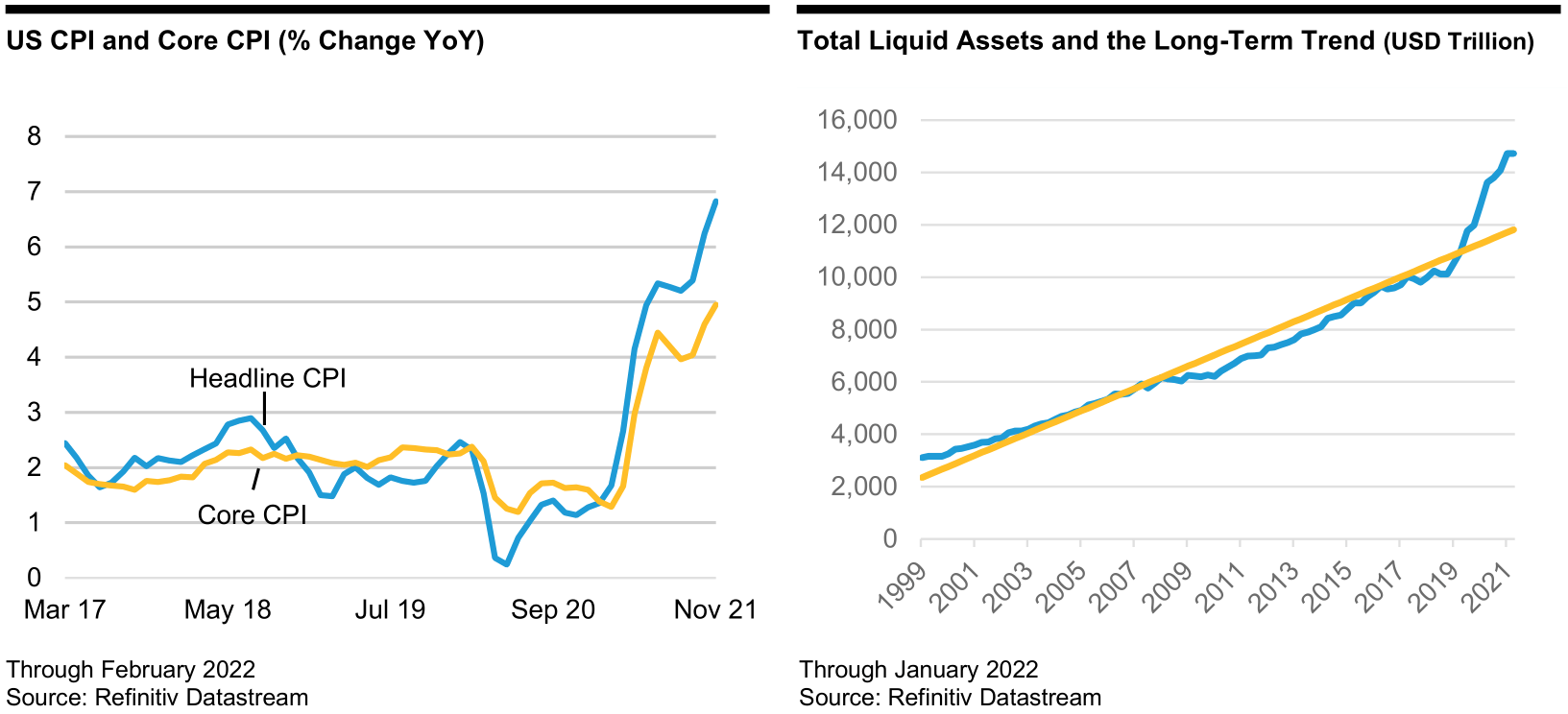

The US economic environment was very challenging before the war in Ukraine and has become even more so since, even if the direct impact of the war is limited. The channel to watch is commodities prices, which seem likely to stay elevated for at least the next several months. That will push inflation, already too high, still higher, and exacerbate the existing growth slowdown.

The good news is that US household finances are in excellent shape. The strong labor market has kept real incomes positive even as inflation has risen, and rising asset prices over the past few quarters have boosted net worth to previously unseen levels. Many households have also accumulated cash balances that are well above the long-term trend. That will allow them to smooth consumption even when confronted with the prospect of paying more at the pump. As a result, we expect a gradual deceleration rather than a sudden stop in activity.

Nonetheless, rising inflation and slowing growth are an awkward and uncomfortable combination for policymakers. For the past few decades, central bankers have preferred to look through energy price shocks as likely temporary. However, with inflation starting at such an elevated level, that won’t be possible this time around. The risk of inflation expectations becoming unanchored is a clear and present danger for the Fed, so we expect it to raise rates aggressively while also starting balance-sheet reduction. That should push yields higher and likely keep the yield curve flat, suggesting a challenging investing environment for some time to come.

China

Outlook

- Consistent with our expectation, the National People’s Congress held in March reiterated the importance of growth stability, setting the GDP growth target at “around 5.5%” this year. This implies a target range with an acceptable upper/lower boundary not far from 5.5%. The Chinese government has never fallen short of its targets, which have been increasingly binding in recent years. So, the lower boundary is more or less a hard constraint: growth below 5% appears unacceptable to the government. That said we don’t expect significant sequential acceleration either. The government doesn’t want to overstimulate its economy as it has in past cycles to prevent the buildup of additional imbalances.

- Cyclical policy in recent months has echoed the central government’s mantra: stabilize the economy as early as possible. But amid old shocks (the housing sector) and new shocks (the Russia-Ukraine crisis and latest COVID-19 outbreak), questions remain in the market about the determination and ability of the government to maintain macro stability in this politically important year. To us, the government appears resolute and is on track to deliver supportive macro policy, to improve its communication with the market and to enhance policy coordination. That gives us confidence that the growth target will be achieved, even in the face of downside geopolitical and COVID-19 risks.

Risk Factors

- The largest risk for our growth forecast is the ongoing COVID-19 outbreak, which weighs on still-recovering services and consumption.

Overview

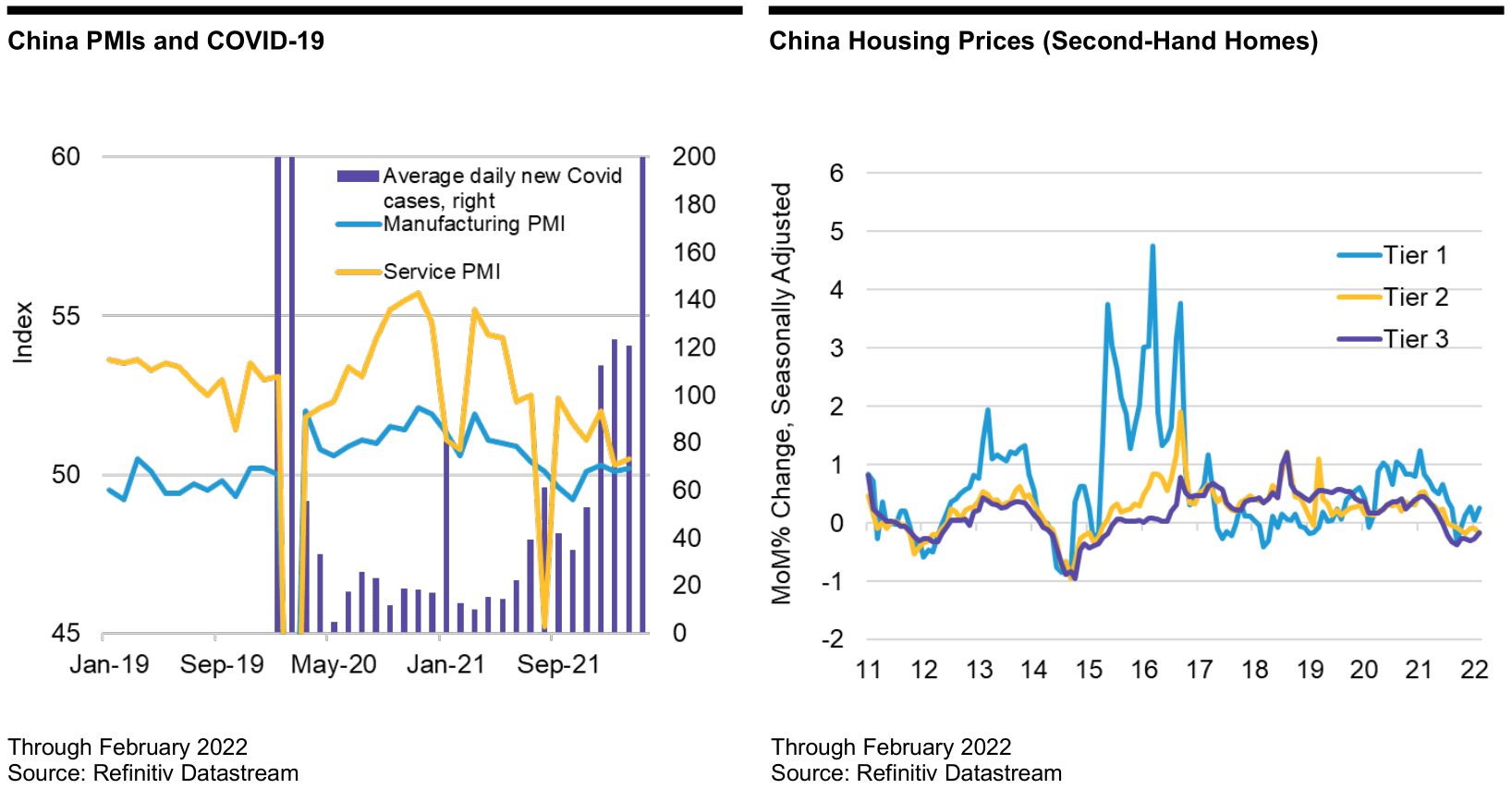

Three key factors warrant close watching in the coming months. The first is the path of COVID-19. Before the current outbreak, we forecast a moderation in sequential GDP growth in Q1 followed by higher sequential growth in Q2 as public investment growth gains stronger momentum. The latest outbreak poses downside for the Q1 growth forecast. But the path in coming quarters depends on how quickly the government can control the outbreak and the size of additional policy support in coming quarters. Given the many uncertainties around the outbreak, we’re still maintaining a 5.3% annual GDP forecast for now, but we’ll continue to monitor the situation closely to assess risks to our forecast.

The second factor to watch is the housing sector. Stabilizing it is important in achieving decent growth this year, given that it’s hard to see a big upside from organic growth drivers and that the government is reluctant to implement a massive fiscal stimulus. We’ve seen policy efforts on both the national level (such as the Peoples’ Bank of China pushing banks to support mortgages and lower loan prime rates) and local levels (including lower mortgage interest rates, reduced down payment ratios and tweaks in purchase restrictions) lead to sequential stabilization in housing sales volume, though at weak levels. Stabilization has remained highly uneven across cities, and we expect more local relaxation ahead.

The third factor is fiscal and monetary policy. The government budget suggests that the on-budget fiscal deficit will be effectively much higher than last year. Although the local government special bond quota is the same as last year, a decent amount of last year’s proceeds, which weren’t used, would be used this year. Overall, the broad fiscal stance should be materially more expansionary than last year’s. We expect further monetary easing, especially in required reserve ratio cuts to increase the credit supply and accommodate expansionary fiscal policy. The likelihood of a policy-rate cut has risen after the latest COVID-19 outbreak, which could send a strong supportive signal and boost market confidence, even if the macro impact might be limited.

Euro Area

Overview

The European economy is directly exposed to the war in Ukraine by virtue of geographic proximity, refugee flows and trade linkages. Western Europe is particularly reliant on Russia and Ukraine for energy and other commodity exports, and with those channels closed we expect a sharp deterioration in euro area growth if the conflict isn’t resolved quickly. As with other regions of the world, inflation in Europe is too high, but we expect the growth shock will be large enough to push inflation to the back burner within a few months: a recession in the euro area seems more likely than not to us at this stage.

The ECB has not yet indicated that it will change its plans to normalize monetary policy and raise interest rates later this year. If we’re right about the growth outlook, however, those plans will likely change. In contrast to the US, the starting point for consumption in Europe is not robust: real household income was already shrinking before the war and will fall further as energy prices rise. The ECB made the mistake of raising rates into a commodity price shock with negative real income growth a decade ago and found itself forced to reverse course very quickly. We don’t expect the ECB to repeat the error. Once the magnitude of the growth slowdown becomes evident, the central bank will likely back off. If not, the outlook could become even more dire.

UK

Overview

The UK economy is being pulled apart. Inflation is high and rising: changes to regulated commodity prices ensure a spike in prices in April and likely another in October. Any hope for a near-term peak in inflation has dissipated. At the same time, the growth outlook has deteriorated significantly. Even before Russia invaded Ukraine, real incomes were falling—rising energy prices will make the situation even worse.

There are no good answers for the BOE. There’s no prospect of inflation returning to target in a reasonable time frame, even if growth slows—as it seems very likely to do. The central bank has already started raising rates and is likely to continue, but it has also signaled its intent to truncate its tightening cycle fairly soon because of the hit it anticipates to real growth. Given where inflation is and, more importantly, where it’s likely to go, slowing or stopping rate increases will be very difficult indeed. We expect several more rate hikes this year despite a deteriorating growth outlook.

Japan

Overview

Japan is the great outlier among developed markets. Yes, inflation is likely to rise as the year progresses—but not nearly so much as in other economies, and not in a way that’s likely to mandate a policy response. While we expect the BOJ to eventually allow rates to move modestly higher, resetting the yield curve control regime a bit higher isn’t nearly as restrictive as the rate hikes that we anticipate elsewhere. Rate hikes remain quite a distant prospect in Japan.

Growth is likely to remain steady, if perhaps unexciting, with the global economy not strong enough to pull Japan into a durable acceleration. If and when the global cycle takes a turn for the better, Japan will follow, especially given the weaker yen. In the meantime, domestic demand will be supported to a degree by both fiscal and monetary policy. Low inflation gives Japanese policymakers that luxury, much to the envy of its global peers.

Emerging Markets

Outlook

- The war in Ukraine amplified stagflation risks and our concerns about the EM outlook.

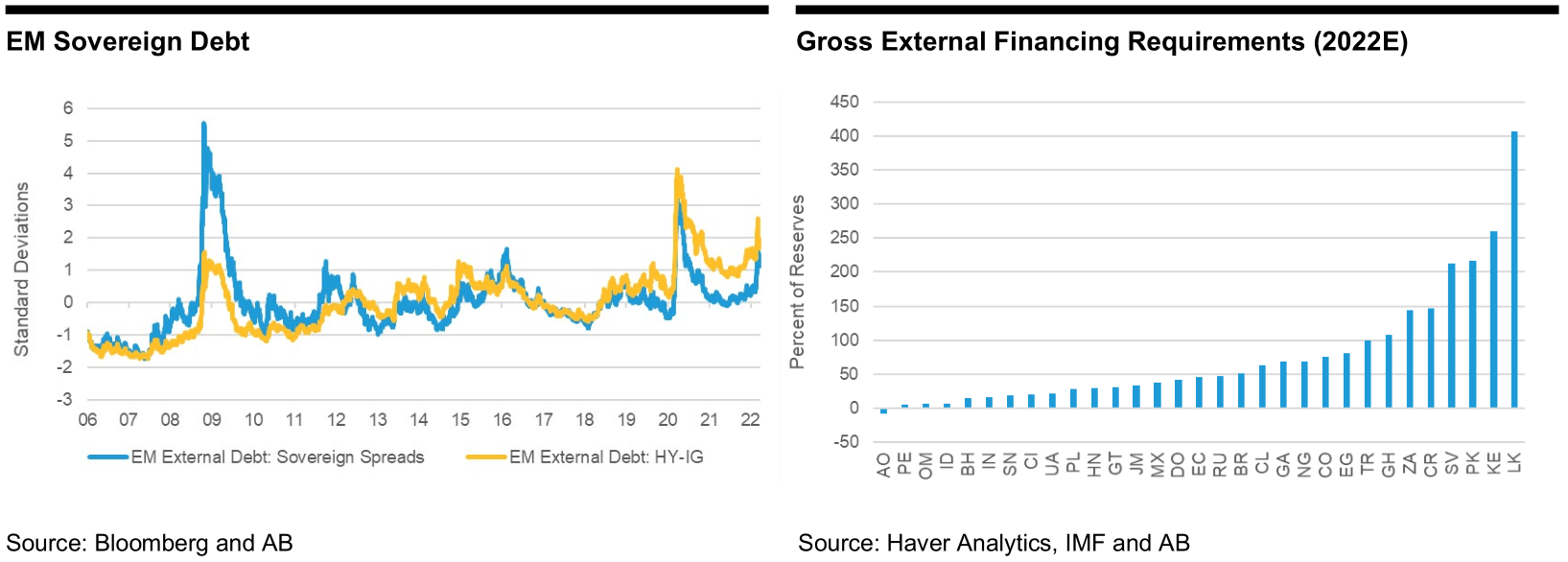

- Although the derating of EM sovereign debt through February and March was extreme, we think there’s been a fundamental deterioration that’s unlikely to reverse in the near term.

- The invasion also sowed the seeds for further fragmentation of relations between the East and the West, social unrest, and economic/policy divergence.

Risk Factors

- Rising external risks amid elevated debt will make it more challenging to generate debt-consolidating economic growth.

- We think back-to-back global shocks have raised the risk of deeper social and governance dislocations (economic scarring), especially in more fragile EMs.

Overview

At the start of the year, we had three primary concerns about the outlook for EM. First, the growth outlook for EM excluding China was not particularly constructive (broadly on par with DM). Second, inflation remained surprisingly sticky and, while some of the adverse COVID-19 influences (supply bottlenecks and goods-demand-driven dislocations) were likely to fade, EM central banks had to keep hiking until core inflation showed signs of cooling (or risk a more enduring shift in inflation expectations). That tilted the balance of risks to the growth outlook further to the downside. Third, the incomplete economic recovery following COVID-19 in many of the more fragile EM economies (the high-yield cohort) and the prospect of waning external buffers heightened the risks associated with the reduction in global liquidity that would likely be triggered by the Fed’s policy normalization.

The war in Ukraine amplified stagflation risks and our concerns about the EM outlook. The marked de-rating of EM sovereign debt through March was extreme, but there has been, in our view, fundamental deterioration that is unlikely to reverse in the near term.

In addition to the adverse growth and inflation implications, the invasion also sowed the seeds for further fragmentation of relations between the East and the West (deglobalization/trade wars), social unrest in response to rocketing global food and fuel prices, and economic/policy divergence between commodity exporters and manufacturing exporters. Commodity exporters—which generally led the policy-rate normalization process through 2021—could be the “safer havens.” However, we think geographical insulation (from Europe) and low external financing needs are other favorable characteristics in the current environment. While external (funding) risks are rising, debt sustainability risks remain elevated, too, with back-to-back global shocks (the COVID-19 pandemic followed by the war in Ukraine) making it more challenging to generate debt-consolidating economic growth.

The invasion of Ukraine has raised the environmental, social and governance (ESG) risk for Russia to an extreme level but also highlighted the importance of critically assessing investment opportunities through an ESG lens. In Russia’s case, the incursion, the widespread scale of international sanctions and the resulting economic isolation have impacted almost every aspect of the country’s ESG profile. But this case also highlighted the potential “externalities” of government behaviour and the need to incorporate those risks into ESG frameworks. Russia’s governance score had to be reduced because of the adverse humanitarian implications of their actions. At the same time, governments in Central Europe, in particular Poland, will likely have to be rewarded in their ESG assessments for their laudable efforts to accommodate large numbers of refugees seeking safety. Beyond the potential idiosyncratic shifts in ESG scores triggered by the war, we think back-to-back global shocks have raised the risk of deeper social and governance dislocations (economic scarring), especially in more fragile EMs.

AB Global Economic Forecast April-22

- Growth and inflation forecasts are calendar year averages.

- Interest rate and FX rates are year end forecasts.

- Long rates are 10-year yields unless otherwise indicated.

- The long rates aggregate excludes Argentina and Russia; Argentina is not forecasted due to distortions in the local financial market; Russia is not forecasted because local market is inaccessible to foreign investors.

- Real growth aggregates represent 29 country forecasts not all of which are shown

Be the first to comment