Igor Kutyaev/iStock via Getty Images

The Macro Picture

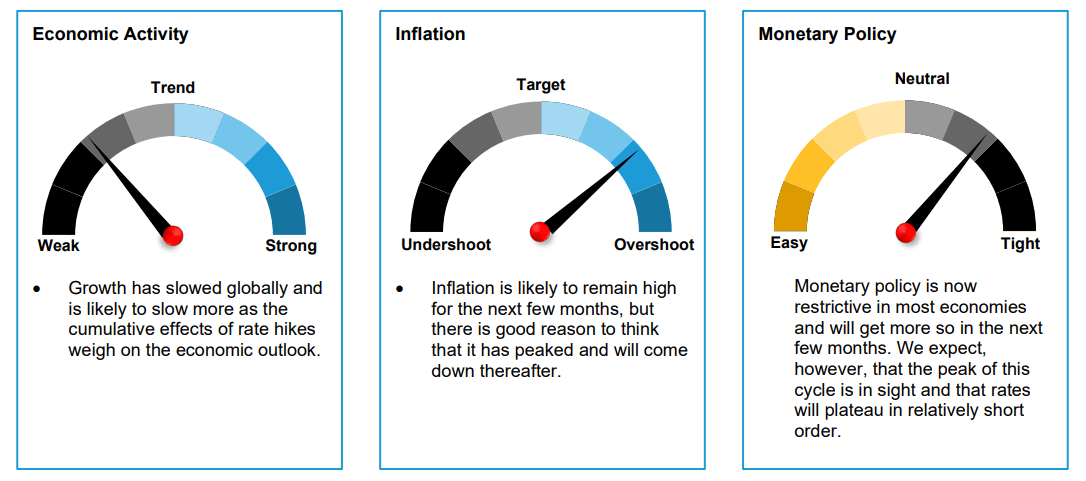

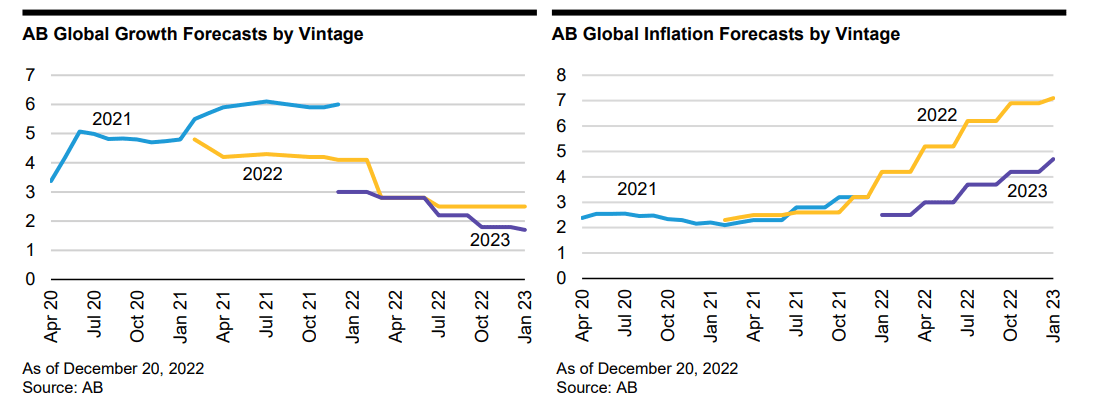

2022 was a year defined by inflation and the policy response to it. We expect 2023 to be a year of transition, with gradual fading of price pressures allowing policymakers and market participants to take a more balanced approach to assessing growth and inflation dynamics. A more balanced approach should reduce market volatility and foster a more benign environment for investors. The timing of that transition, however, remains unclear and is likely to be defined by the amount of damage done to the economy by this tightening cycle.

To be clear, the job of fighting inflation isn’t done, and we expect additional rate increases in most major economies during the first quarter. But we’re confident that the cumulative impact of rate hikes last year and early this year will be sufficient to bring inflation down. That means that the pace of rate hikes will continue to slow and, we expect, cease within a few months.

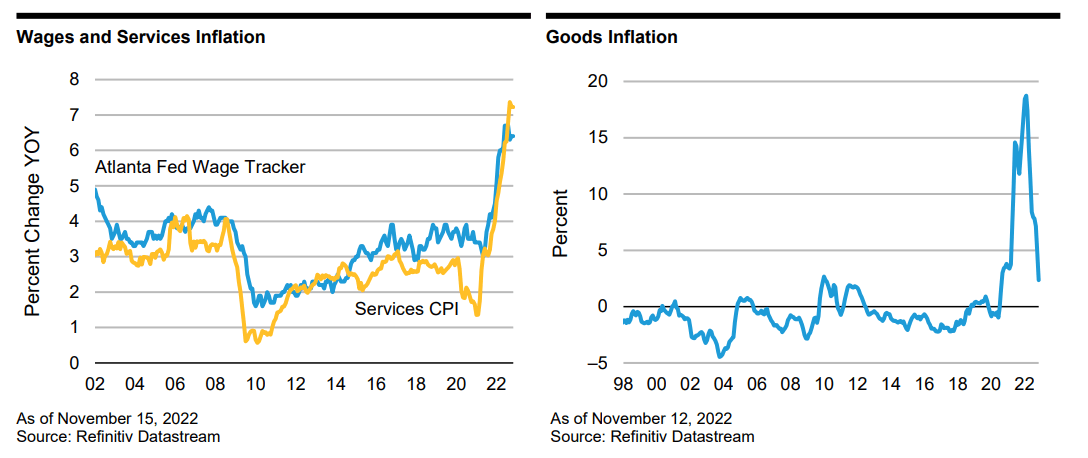

Our confidence that inflation will slow stems from a bottom-up look at the components of price pressures. We identify three broad inflation categories: goods, housing, and services.

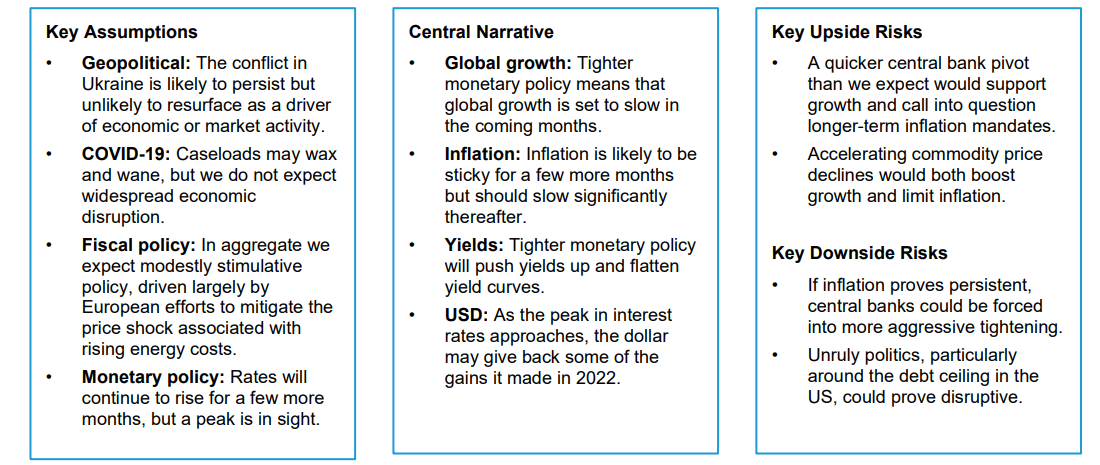

Goods prices were the primary driver of the early stages of inflation’s surge. Supply chain disruptions resulting from the COVID-19 pandemic pushed goods prices higher as manufacturers struggled to acquire production inputs. Now, however, goods prices have started to fall—down on a month-over-month basis in each of the last three months in the US. Evidence from manufacturing surveys makes clear that supply chain disruptions are largely behind us, and producer inventories have recovered to normal levels. Commodity prices have fallen sharply; oil is down roughly 25% from peaks, and even natural gas has fallen despite the ongoing war in Ukraine. This gives us confidence that goods prices will continue to contribute to disinflation in the coming months.

Housing-related inflation hasn’t likely peaked, but we expect that it will in the next few quarters. Shelter inflation is driven largely by house prices, which have turned lower in many developed-market economies as rising mortgage rates bite into demand. We recognize that measured housing inflation significantly lags developments in real-time house prices; most estimates are that it takes roughly 12–15 months for price developments to pass through into inflation. Since house prices appear to have peaked in April 2022, it may not be until mid-year that housing-related inflation falls materially. Nonetheless, we have high confidence that it will, which will provide further support for the disinflationary process.

The most stubborn of the inflation categories is the broader services measure. Here, there’s still no tangible relief, nor strong signs that it’s imminent. The primary driver of non-housing services inflation is the labor market. Tight labor markets mean rising wages, which are being passed to consumers, pushing services inflation higher. And labor markets remain tight globally.

Because labor markets remain tight, we disagree with the market narrative describing the change in central bank policy as a “pivot.” We prefer to think of it as a “plateau.” Central banks are likely to stop raising rates, but they’re also likely to leave them at restrictive levels until the labor market weakens meaningfully. Inflation rarely comes down without causing some economic pain, which we expect to become more evident as the year progresses.

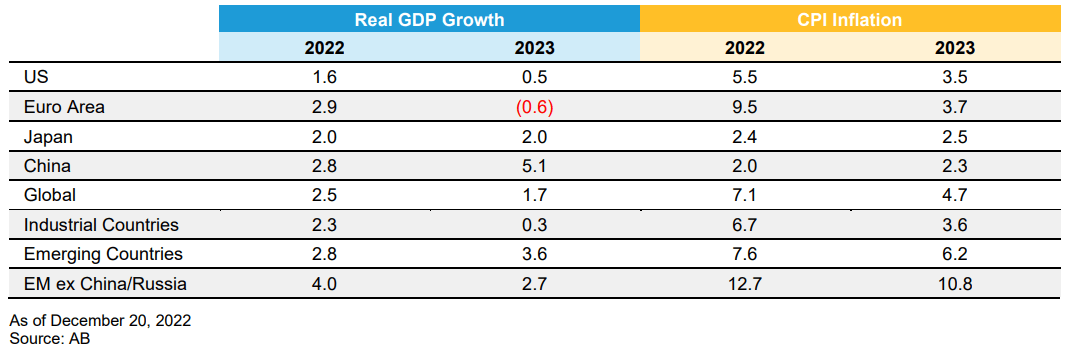

Our forecasts for the major economies of the world incorporate a fairly mild recession, characterized by GDP growth close to zero in the US and slightly below that in the UK and the euro area. We also expect unemployment to rise above its equilibrium level in each economy. The damage is likely to be greater in Europe because of the shock of the Ukraine war on natural gas imports to the euro area, and in the UK due to a more limited post-Brexit labor supply.

Some good news: we see little evidence of significant economic or financial imbalances that could cause a mild recession to spiral into something more severe. The global financial system is better capitalized and heightened regulation in the aftermath of the financial crisis means that there is a much lower probability that poor risk management will lead to leverage or liquidity concerns. That is critical to the outlook because the financial sector if in distress, can fuel the fire if the global economy starts to slip.

Similarly, we see no evidence of asset-price bubbles in systemically important sectors of the economy. To the extent that there are bubbles, they seem most likely to appear in smaller segments of the financial system—places where their impact is less likely to cause significant collateral damage. There’s no guarantee, of course—the tricky thing about bubbles is that they are often hard to observe until after the fact—but for now our assessment is that the systemic risk posed by inflated asset prices seems quite limited.

Not all global economies are headed in the same direction, and the outliers may offer investors a different opportunity set. Japan comes into 2023 still in full easing mode, with both fiscal and monetary stimulus at close to full throttle. We expect rising inflation in Japan to lead to some tightening of monetary policy, but the magnitude of that tightening is likely to be far more limited than elsewhere. As a result, we don’t expect as severe an economic downturn in Japan as we do in developed western economies.

China, too, is off cycle with the rest of the world, largely because of its slow and halting reopening from the COVID-19 pandemic. We expect sequential acceleration in Chinese growth in 2023 even as growth among its trading partners decelerates because reopening will accelerate into the year and we expect additional fiscal and monetary policy support.

Emerging markets (EM), too, may offer opportunities in 2023. Many EM economies tightened policy earlier and more aggressively than their developed-market brethren, which could mean an earlier start to easing and an increase in growth expectations. That may not happen until developed-market central banks are firmly on hold, but we expect it in the coming months.

What does this mean for financial markets? The growth outlook for the global economy is a gloomy one, to be sure. But in contrast with 2022, we expect policymakers increasingly to acknowledge the economic slowdown as the year progresses. Slowing inflation and stable monetary policy should reduce interest-rate volatility, and lower volatility typically favors higher-yielding assets. It is likely that the ride will remain bumpy at least for the first few months of the year, but the overall outlook for markets has improved significantly in the last few months, and we expect that trend to hold for 2023.

The Global Cycle for 1Q:2023

Global Forecast

Forecast Overview

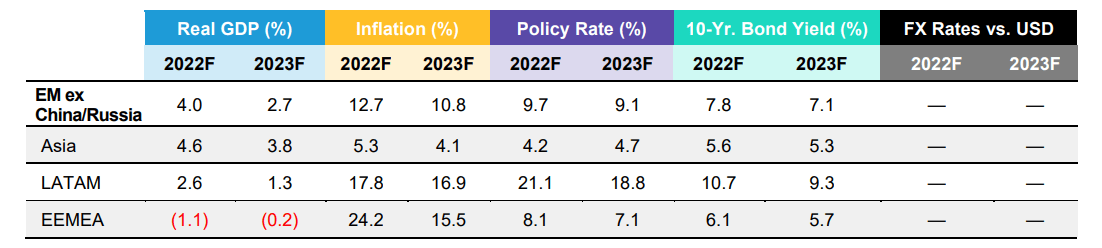

AB Growth and Inflation Forecasts (Percent)

Forecasts through Time

US

- Inflation remains elevated and is likely to come down only gradually in the first part of 2023. Still, our conviction that it will come down has strengthened. Supply chain disruptions have eased, house prices have fallen and growth is set to slide, all of which argue for reduced price pressures in 2023.

- The one variable not in place for inflation to return to the Fed’s 2.0% target over the next couple of years is the labor market, which remains very strong. We think it unlikely, however, that labor-market strength will persist. The cumulative weight of the Fed’s very aggressive tightening over the past few quarters will dampen labor demand and help to rebalance the economy by slowing growth. We expect a mild recession in 2023.

- We expect additional rate hikes in the near term to be followed by a sustained period of stable monetary policy. Rate cuts are possible in late 2023 but we are not nearly so confident in that outcome as financial markets appear to be.

Risk Factors

- Sticky inflation remains the predominant risk: if inflation doesn’t fall, the Fed will have little choice but to keep tightening even at the risk of causing a more negative economic outcome.

- We don’t foresee the variables in place for a spiraling downturn, but financial-sector instability or bursting asset bubbles remain a possibility as growth slows.

Overview

The near-term outlook calls for more of the same: high inflation and rate hikes, albeit at a slower pace. But beyond the near term the situation appears to be improving. There is good reason to expect inflation to fall, which should allow the Fed to take a more measured approach to monetary policy. While we don’t share the market’s confidence that the Fed will pivot to aggressive rate cuts in 2023, we do expect a plateau in interest rate, which should be sufficient to dampen financial market volatility to a significant degree.

The key variable as we move into 2023 is the labor market—it won’t be until the labor market has weakened that the Fed is comfortable enough with the inflation outlook to stop rate hikes. Timing that turn is impossible ex ante, but we’re confident that it will come. The accumulated weight of the rate hikes already undertaken and not yet fully felt in the economy is going to slow growth to the point that labor demand weakens. Whether the economy ends up in a recession or not is in the eye of the beholder: there is no one official definition of recession. To us, the combination of growth close to zero and a rise in unemployment will be enough to characterize the picture as recessionary, but others may differ. Either way, it won’t be a pleasant experience. The good news is that we don’t see the factors that would turn “unpleasant” into dismal; the financial sector looks healthy and systemically significant asset bubbles are hard to see. Not all recessions are catastrophic, and our expectation is that the coming slowdown will be mild by historical standards.

China

Outlook

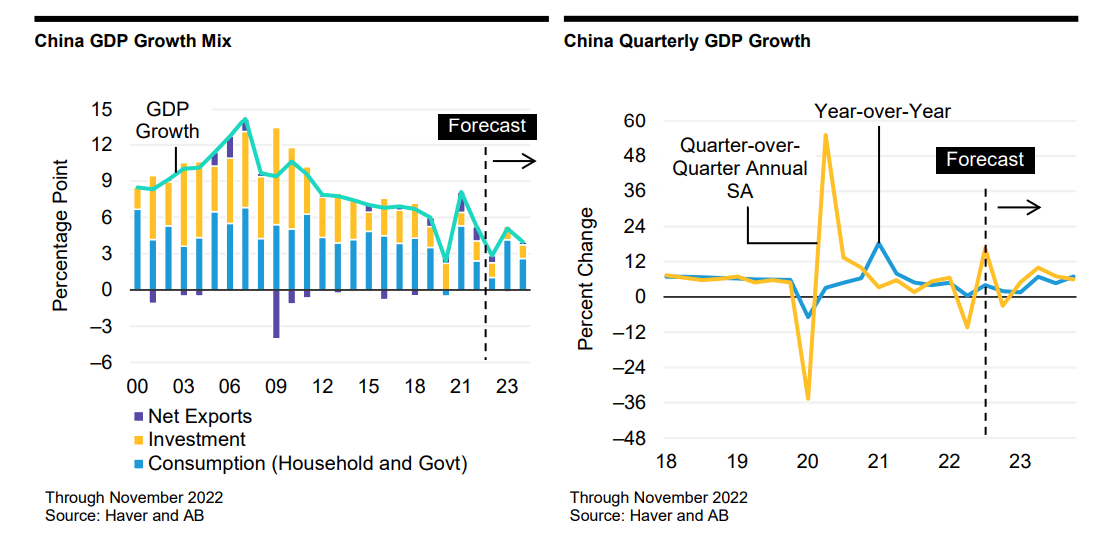

- China’s economy has been hit by a series of significant and unexpected shocks in 2022, forcing an intra-year adjustment in the policy reaction function balancing debt and growth. As a result, growth has fallen short of forecasts. The tug-of-war between sluggish private demand and strong public demand has left the economy stuck in the middle—not so slow as private demand would suggest but not as strong as public policymakers might have hoped. That balance will continue to define China’s growth trajectory in the near term.

- We remain relatively constructive in growth for 2023, because we think that maintaining the economic growth rate within reasonable range in 2023 will be the government’s top priority. Developments at the recent Central Economic Working Conference are consistent with this perspective. An accelerating reopening from COVID-19 lockdowns and more efforts in stabilizing its housing sector have also revealed this preference, which should mitigate two major sources of downside risk.

Risk Factors

- It’s encouraging to see the government start to shift to a reopening regime sooner than expected, but there could be downside for near-term activity if the population remains hesitant to reengage.

- A slower and/or weaker-than-expected recovery in housing activity—if sentiment around the sector doesn’t improve or even gets worse—could pose downside risks for growth.

Overview

Our baseline forecast for GDP growth in 2023 is 5.1%, helped by a favorable base effect, with a shift in growth mix. With progress in vaccination levels and the government starting to accelerate reopening, we expect private demand to improve sequentially— household consumption is gradually approaching pre-pandemic trends; however, it will likely be difficult to have as strong a rebound as we saw in the west. Housing investment will see a shallow stabilization supported by further policy easing. Household expectations around the property market will be a key factor affecting the pace and slope of recovery in the housing sector. In the meantime, government-driven investment may slow somewhat from the large stimulus that was required in 2022. But we still expect solid public sector demand until organic drivers are robust enough to boost growth sustainably. Dividends from exports, which emphasizes both higher income per capita and smaller inequality, rather than just sacrificing growth to achieve smaller inequality. Given high amounts of income/wealth inequality in China, narrowing inequality could be good for economic rebalancing and long-term growth.

Beyond the cyclical outlook, and with the conclusion of the 20th Party Congress, another key focus is on long-term structural policy. To appreciate China’s long-term outlook, nothing is more important than correctly understanding “Xi thoughts” and their intention. Maintaining decent long-term growth is still very important to the Chinese government, and it’s equally important as the improvement in the quality of that growth. China isn’t trying to roll back decades of market-oriented reform, but rather will push reform further, especially in factor markets. This, alongside a focus on innovation and strong support for manufacturing, is key to China’s long-term growth potential. And decent long-term growth is a precondition for achieving “common prosperity,” which emphasizes higher income per capita to shrink inequality. Given high amounts of income/wealth inequality in China, narrowing inequality could be good for rebalancing wealth and long-term growth.

Euro Area

Overview

While the economic outlook for Europe remains challenging, developments in recent months have been better than expected. An aggressive effort to rebuild natural gas stockpiles and a warm start to the winter season have limited the risk of energy rationing, reducing the probability of a severe recession. Nonetheless, the growth outlook is poor. Elevated inflation is forcing the European Central Bank to push rates higher and start reducing the size of its balance sheet; higher interest rates in a low-growth economy can bite hard and fast. The war in Ukraine drags on, an unhelpful overhang for business investment. As a result, we continue to expect negative growth in 2023.

Fiscal policy is an important lever for authorities to manage the downturn. We expect fiscal support will be limited to addressing the worst effects of the natural gas price surge rather than endeavoring to push growth onto a higher trajectory.

UK

Overview

The UK is in truly difficult circumstances. Inflation remains far too high due largely to energy costs, leaving policymakers with the choice of either subjecting households to pain or taking the brunt of the adjustment onto government fiscal accounts. The Sunak government has chosen the latter, at least for now, but if prices don’t fall the cost will only increase.

While energy costs are the primary culprit for high inflation, limited labor supply is also playing a role. In a post-Brexit world, labor supply is likely to be relatively inelastic, forcing policymakers to make the unappetizing choice of constricting demand to bring it down to the new supply level.

That means rate hikes, which the Bank of England (BoE) has delivered. As with other central banks, we believe that the BoE will stop raising rates at some point in the first half, but also that the long-term equilibrium for the UK will be less favorable: the new normal will have lower growth and higher rates than the old normal.

Japan

Overview

Japan’s macro outlook is fascinating. Inflation is rising, but given the country’s historical experience, policymakers and other economic actors are rightfully skeptical that the increase will prove durable. That has forced the BOJ to remain extraordinarily accommodative even as other central banks around the world have tightened aggressively. The result is that the yen has weakened far beyond most measures of long-term equilibrium.

With inflation rising and the weak yen causing rising political pressure, we expect the BOJ to change course in 2023 and tighten policy, a process that began in December with the widening of the yield curve control band. The transition at the central bank’s helm scheduled for spring is an event to watch closely to see if incoming leadership has a different view than the outgoing one.

Emerging Markets

Outlook

- We think the worst of the EM sovereign default cycle is over.

- The year-ahead macro outlook seems somewhat clearer than it did at the start of last year. This is largely because central banks appear to be approaching the end of their interest-rate hiking cycles, inflation has started to ease, and a slowdown in economic growth is in train.

- We think the stage has been set for a better carry environment to start the year, with the potential for more substantive returns further out.

Risk Factors

- A key risk is that the slowdown in global growth causes a collapse in commodity prices.

- There might be a settlement of the conflict between Russia and Ukraine, but continuation of the conflict seems more likely.

Overview

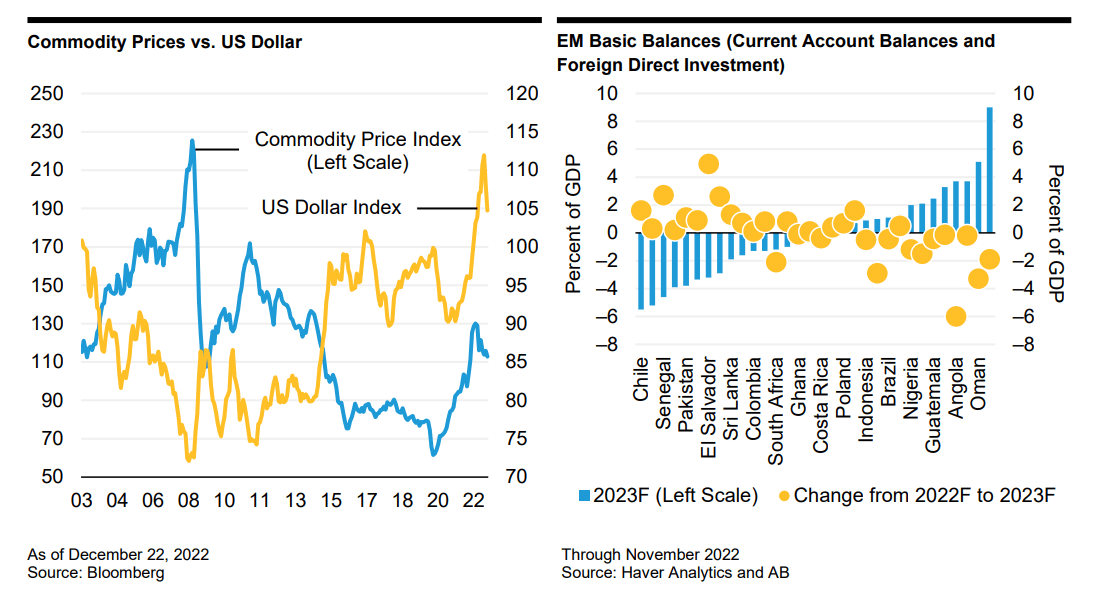

Commodity prices eased in the second half of 2022, but they generally remained well above pre-pandemic levels. Higher commodity prices are, on balance, positive for emerging markets (EM), especially when it coincides with US dollar weakness. The cycle over the past two years has, however, been somewhat unusual—commodity prices increased sharply, but the US dollar appreciated too (Figure 1). This mix (higher commodity prices / stronger dollar) fueled inflationary pressures and challenged EM’s fiscal resolve. We think the worst of the EM sovereign default cycle is over, but relatively high debt ratios and high debt service costs could continue to curb EM asset prices as the global economic downdraft gains traction early in 2023.

A key risk is for the slowdown in global growth to cause a collapse in commodity prices. That would certainly help the goods disinflation cycle and remove some heat from core rates. Emerging countries with large local debt markets and mature interest-rate hiking cycles (Brazil, Chile, Colombia, Mexico, Peru, and South Africa) might benefit. But such a scenario could be quite challenging for commodity-dependent countries with large external financing requirements. In fact, rising external debt amortization and deteriorating basic balances (Figure 2) could be particularly challenging for EM countries with limited bond market access.

The potentially more resilient countries mentioned above do, however, face their own challenges. In Brazil, President Lula’s left-leaning policies would need to be effectively moderated by the opposition-controlled congress, while idiosyncratic risks in Chile (constitutional process), Colombia (economic/institutional reforms), Mexico (regional elections which could set the stage for the presidential elections in 2024), Peru and South Africa (political risks) could disrupt their respective financial markets.

Two developments that contributed to EM’s lackluster performance in 2022 included China’s economic underperformance and the multiple crosswinds caused by the Russia-Ukraine war. Signals that China might be winding down its zero-COVID policy are encouraging, but we don’t think China’s normalization in 2023 will boost the EM growth outlook meaningfully. Still, China’s potential reopening, combined with its current low commodity inventories, should be a stabilizing factor for commodity prices and EM. The risk of a collapse in commodity prices might also be less than would generally be gleaned from the global growth cycle due to recent underinvestment in the sector.

The Russia-Ukraine war could unfortunately persist throughout 2023. The military momentum seemed to shift in Ukraine’s favor by August when the Ukrainian armed forces managed to make major territorial gains. But with Russia recently consolidating its new lines of defense, risks are high that Ukraine’s military momentum wanes and the conflict reaches another stalemate. We think there’s a possibility for a settlement in late 2023, but a continuation seems more likely.

For 2023, the macro outlook seems somewhat clearer than it did at the start of last year. This is largely because central banks appear to be approaching the end of their interest-rate hiking cycles, inflation has started to ease and a slowdown in economic growth is in train. We think the stage has been set for a better carry environment to start the year, with the potential for more substantive returns further out.

Investment Risks to Consider

The value of an investment can go down as well as up and investors may not get back the full amount they invested. Past performance does not guarantee future results.

Important Information

Note to All Readers: The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA -Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). Information in this document is intended only for persons who qualify as “wholesale clients,” as defined in the Corporations Act 2001 (Cth of Australia) and should not be construed as advice. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. AllianceBernstein (Singapore) Ltd. is regulated by the Monetary Authority of Singapore. This advertisement has not been reviewed by the Monetary Authority of Singapore. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (聯博香港有限公司), a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional distribution. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Important Note For UK and EU Readers: For Professional Client or Investment Professional use only. Not for inspection by distribution or quotation to, the general public.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

© 2022 AllianceBernstein L.P.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment