thamerpic/iStock Editorial via Getty Images

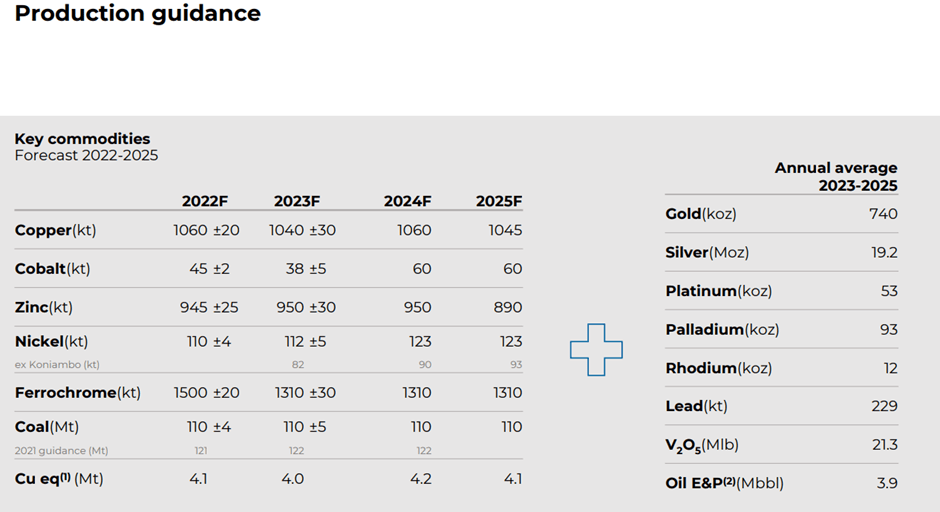

Glencore’s (OTCPK:GLNCY) investor update earlier this month saw key guidance changes that were largely consistent with the rest of the global miner universe. Of note, capex guidance was meaningfully increased relative to prior guidance at $6bn for FY23 (vs. $4.7bn) despite production guidance for FY23/24 being lowered across the board. Alongside the guidance update, management also indicated a strategic pivot toward growth with a new focus on ‘greenfield’ mine developments and a higher net debt ceiling to provide headroom for M&A opportunities.

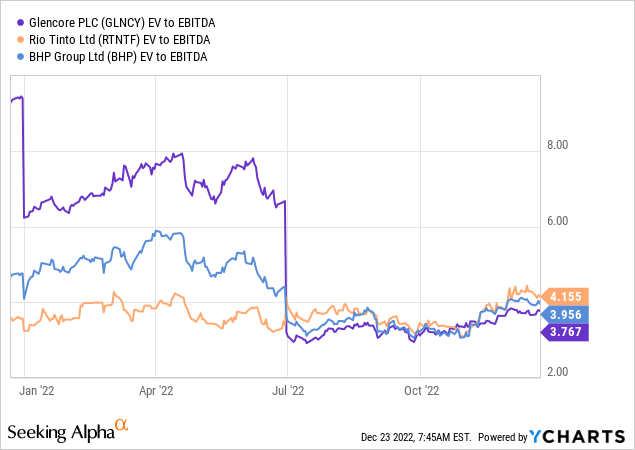

While these new developments could delay a credit rating upgrade anytime soon, the long-term equity story remains attractive. Glencore continues to boast a diversified portfolio positioned to capture the near-term outperformance in coal, as well as long-term electrification tailwinds via copper and nickel. Thus, even if the strong free cash generation in coal normalizes lower over time alongside energy markets, this gap should be more than sufficiently replaced with cash flow growth from copper and nickel. Net, I feel comfortable underwriting a future re-rating at the current relative EV/EBITDA discount; the high-single-digit % dividend yield means investors get paid to wait in the meantime.

Production Guidance Down; Capex Up

The key read-through from Glencore’s latest investor update is that it wasn’t spared from the rising capex trend across the global miner universe. While some increase was anticipated pre-event due to the ramped-up de-carbonization efforts, the extent of the latest guidance increase was a surprise at $6bn for FY23 (vs. $4.7bn prior).

Alongside the higher capex, production guidance was lowered across key divisions. Of note, copper output targets through FY25 suffered cuts, primarily due to Katanga, where FY23/24 will see a disappointing ~205kt of copper output before ramping up to ~255kt from FY25 onwards. The coal production guidance through FY25 was similarly lowered, though this was down to the scheduled closing of three mines during FY23/24. With several zinc mines also approaching their end of life, the updated zinc output guide was adjusted to reflect a steeper near-term production decline.

Glencore

A Uniquely Positioned Portfolio for the Near and Long Term

Still, there were silver linings from the investor update. For one, Glencore reiterated that commodity markets remain underinvested and de-stocked ahead of strong demand tailwinds. Given its unique portfolio mix comprising a balance of thermal coal and leading positions in high-growth metals like copper and nickel, the company is well-positioned to ride out the cycles. Case in point – Glencore’s coal franchise has provided a useful buffer in H2 against commodity headwinds from China’s slowdown and broader macro concerns. With the impact of continued supply tightness in coal set to be further amplified by a demand upturn from the ongoing energy crisis globally, higher for longer prices should continue to benefit Glencore.

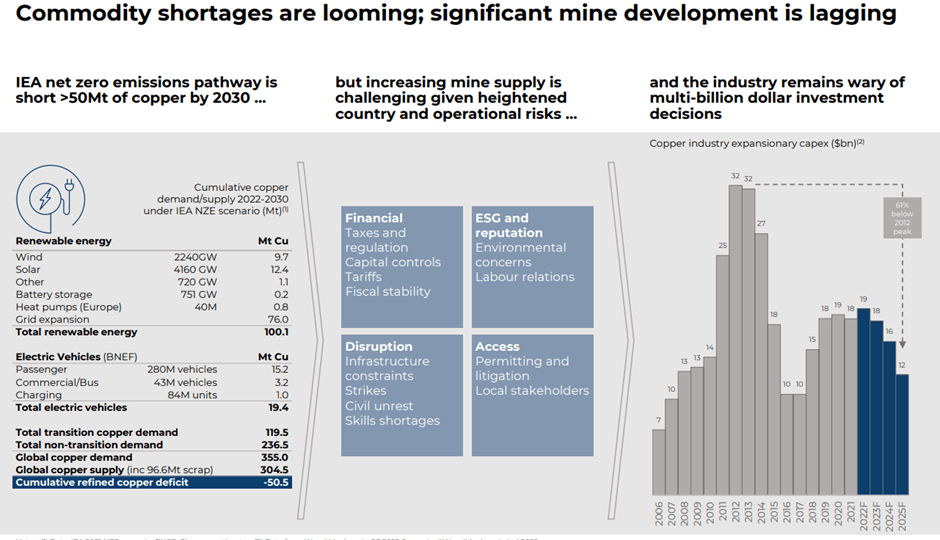

On the other hand, Glencore also has a rich mix of battery metals in its portfolio, including copper, nickel, and cobalt. Its leadership position across these metals positions it well for secular growth in EV production and the broader transition to a greener economy. Traction thus far has been strong – the company has already secured supply agreements with General Motors (GM) and Tesla (TSLA). Expect more orders ahead, given the favorable demand/supply balance. Management offered some useful statistics to support this view as well – per the event slides, relative to ~355mt of copper demand over the next eight years from renewable energy and EVs, global mine supply stands at ~305mt, implying a significant ~50mt cumulative deficit.

Glencore

Capital Allocation Tilted Toward Growth

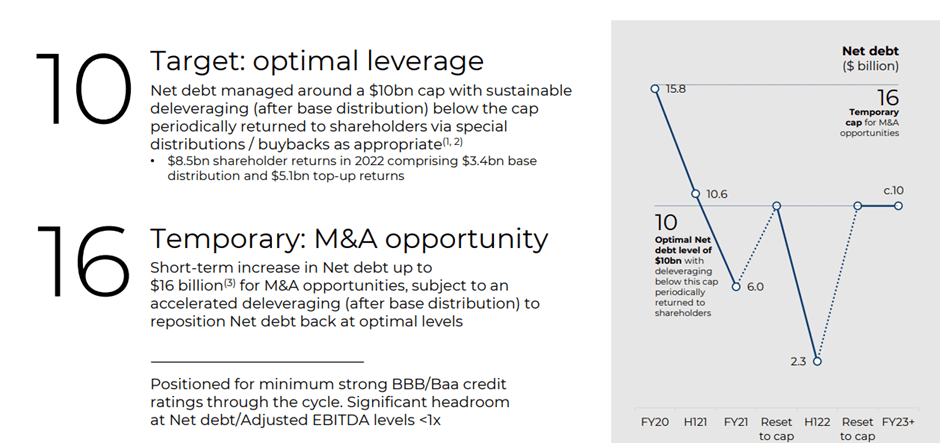

Despite the production cuts, Glencore appears to have shifted its strategic messaging away from portfolio streamlining and excess capital distributions toward growth. Supporting this view is the discussion of greenfield project development and the potential optionality. Plus, the M&A flexibility has also been expanded, with management now guiding toward a higher (albeit temporary) $16bn net debt tolerance for transactions.

Glencore

While the prospect of inorganic growth bodes well for the P&L, more capital deployment could see any rating upgrades being delayed. For context, Glencore had been well on its way to a single-A rating (vs. BBB+ currently), given its quality revenue and EBITDA profile, as well as declining net debt position. That said, the strong cash flow and net debt cap remain intact, so continued improvement on the ESG front (now a key rating criterion) could still drive an upgrade catalyst in the coming months.

Look Past the Bearish Investor Update

Even with the lower production, higher capex, and lower free cash flow guidance disclosed at this month’s capital markets investor event, Glencore remains relatively well-positioned for cash returns through the cycles. In the near term, coal tailwinds will be key – in a tight market where energy demand is outstripping supply, Glencore’s coal capacity should benefit from elevated prices for the coming quarters. While bears will point to an eventual downcycle in coal, Glencore’s unique portfolio skew toward copper, cobalt, and nickel give it valuable exposure to secular growth trends such as electrification.

Yet, Glencore stock trades at an undemanding ~3x EBITDA, a double-digit % FCF yield, and offers a well-covered high-single-digit % dividend yield as well. With any stock-specific overhang from regulatory investigations also resolved and the company maintaining a minimal net debt position, the risk/reward seems compelling here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment