hallojulie

The initial 2022 bearish thesis

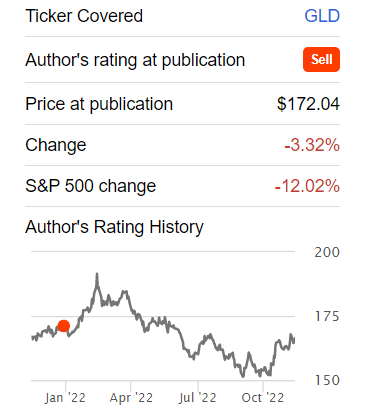

I recommended a sell for gold (NYSEARCA:GLD) on January 21st, 2022. But, this trade was all over the place, currently down 3.32% from the price at publication.

Seeking Alpha

The bearish thesis at the time was as follows:

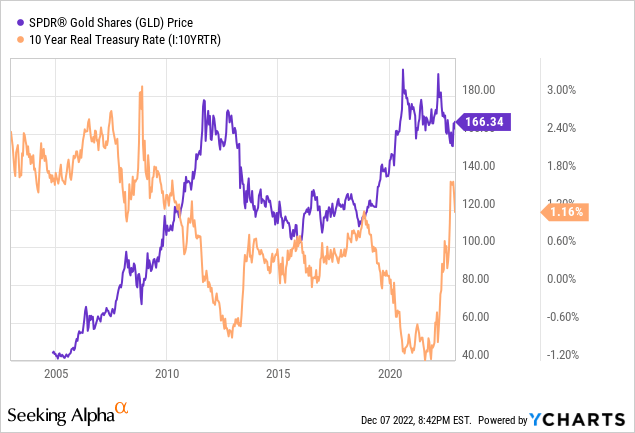

“Real interest rates have been rising since January 2022 (from below -1% to -0.60%) and it is likely that real rates will continue to rise and turn positive in the near future – as the nominal yields rise due to quantitative tightening. As a result, given the historically almost perfect negative correlation between the real interest rates and gold, gold is likely to fall.”

The real interest rates really spiked in 2022 from -1% to above 1.7% just recently – this was a correct call. However, in March of 2022 the geopolitical risk sharply increased as Russia invited Ukraine – boosting the appeal of gold as a hedge against heightened geopolitical situations and caused the spike in price – this was completely unexpected in early January of 2022.

Yet, I maintained the short recommendation expecting that the rising real interest rates would prevail and cause lower gold prices in 2022 – despite the geopolitical situation. In fact, gold quickly reversed the gains, and the downtrend continued as expected – until early November when the counter rally started and eroded most of the gains from the short side.

The 2022 bearish thesis was an obvious macro trade – historically rising real rates cause lower gold prices. In addition, the rising US real rates generally cause a stronger US Dollar, and the rising US dollar (DXY is up 10% YTD) also contributes to the falling gold prices.

The 2023 outlook for gold

So, what’s the outlook for gold for 2023? Gold is not an obvious short as a macro trade at this point. As the chart below shows, the real rates have risen close to the 1.8% level, which is the lower level of the early 2000s range. I addition, the US Dollar has also strengthened substantially in 2022, and the future gains are limited. So, is now a good time to buy gold?

I will take the “novel” macro approach introduced by the Fed Chair Powell to discuss the gold outlook for 2023. Specifically, during his speech at the Brookings Institute, Powell admitted that:

The truth is that the path ahead for inflation remains highly uncertain. For now, let’s put aside the forecasts and look instead to the macroeconomic conditions we think we need to see to bring inflation down to 2 percent over time.

I think the truth is that the direction for the price of gold in 2023 is highly uncertain, but I can identify the macroenvironment that would turn me bullish and bearish on gold in 2023.

The bullish macroenvironment

- Have to see the early indications of a deep recession and a severe financial crisis.

- For the resumption of the longer-term uptrend in gold, the Fed has to stop with the QT, and it has to restart the QE program. It’s very simple, the real rates have to turn negative for gold to significantly rise, which requires the 2008-like and the 2020-like monetary policy stimulus, and thus a deep recession with a financial crisis.

- Obviously, the Fed would also sharply lower the interest rates towards the 0% level in such macro environment.

- The Fed accepts the higher inflation target

- In a situation of a deeper recession and still persistently higher inflation (above the 2% target) the Fed shifts focus from inflation to growth, and effectively abandons the 2% target.

- Have to see the early indications of the US Dollar’s vulnerability as the reserve currency

- The global geopolitical environment, which includes the de-globalization trend, is bullish for gold if it appears the US is somehow losing its’ economic, political, and military global supremacy. The US Dollar would sharply depreciate in such environment.

- The runaway inflation expectations, or the increase in long-term breakeven inflation, would also reflects the uncontrolled de-globalization with spikes in commodity prices and supply-chain disruptions.

- The US fiscal deficit is bullish for gold if there are indications that rising interest rates are making the interest payments unsustainable, the global demand for US Treasuries sharply falls, and the US government is pushed into an “experimental” fiscal/monetary policy mix.

- The US internal political divide gets even more extreme leading to the 2024 election, contributing to the potential US diminishing global leadership position.

The bearish macroenvironment

- The real interest rates continue to grind higher

- The real rates were generally equal to the inflation expectations prior to the Fed’s QE experiments starting in early 2000s. Now that the Fed is trying to reverse the QE with the QT, it’s reasonable to expect that the real rates will continue to rise to the 2-2.5% pre-2008 crisis level and equal the long-term breakeven inflation expectations.

- The Fed holds interest rates high for longer

- The Fed increases the interest rates to 5-5.50% level, which does not cause a deep recession, and thus, the Fed is not forced to immediately cut interest rates.

- Even if the US recession is deeper, the inflation remains persistently above the 2% target, and the Fed is unable to lower interest rates.

- The US continues winning the de-globalization fight

- The US-China decoupling has so far resulted in a much weaker China. De-globalization will make the winner and losers, and the ability of the US to efficiently re-shore the supply-chains would continue to boost the US dollar.

- The US is also emerging as the winner in a proxy Ukraine-Russia war, and the Russia-China alliance is more likely to crack before the NATO alliance cracks.

Implications

We are facing a very uncertain macro environment in 2023. How deep will the widely expected recession will be? How is the Russia-Ukraine war going to progress? How is the US-China decoupling continuing to evolve?

Trading gold based on individual forecasts of the outcome of these events could be a fool’s game. Gold trades based on collective sentiment, and thus, in such an uncertain environment, it is necessary to consult with the technical picture.

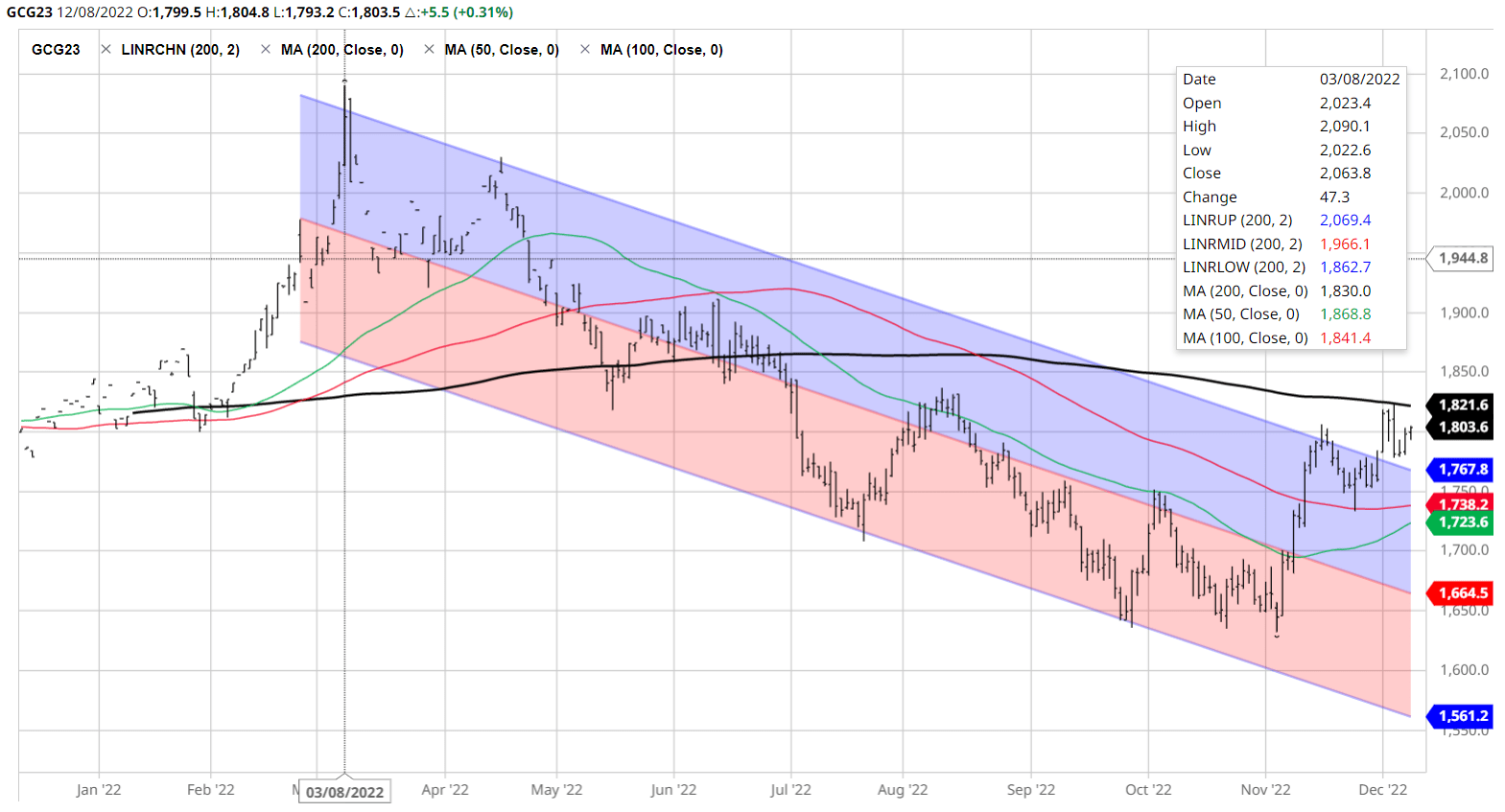

Gold has been in a downtrend since the March 2022 spike due to Russian invasion of Ukraine. The downtrend reflected the rising real interest rates and the stronger US Dollar in 2022. So, as long as the downtrend is in place – that’s the theme.

Gold found a very strong support at the 1650 level (150 on GLD), and it’s currently in a counter-trend rally at the key 200dma resistance and top of the downtrend channel.

The recent counter-rally has been based on the expected Fed pivot, in response to the downside surprise in the CPI, and the expectations of covid-reopening in China. These events caused a weaker US Dollar and boosted gold. The real rates fell from 1.7% to 1.2%.

In my opinion, the current counter-rally is unsustainable because it’s based on a US soft-landing expectation and a stronger global growth led by China. It does not fit the bullish macro environment described in this article.

Yet, gold above the 200dma is a buy due to the collective sentiment – especially if there is some data point in favor in support of the breakout. The stop loss order should be below the 200dma.

However, at that point, gold could be a short given that the current counter-rally is unsustainable and the prevailing downtrend. The stop-loss should be above the 200dma.

Barchart

From the trader’s point of view, gold is at the crossroads, with the possible short position entry right near the top of the channel and significant short-term profit opportunity as gold revisits the 1650 level. Also, there is a potential long position entry as the prevailing downtrend is broken and gold likely revisits the previous highs.

From the investor’s point of view, gold is not an obvious macro trade/hedge in 2023 yet, and it is likely that gold will be in a narrow range until the fundamentals shift, one way or the other.

I would say the most important fundamental variable to follow in 2023 is the Fed’s commitment to the 2% inflation target. Any hint that the Fed would allow a higher inflation target would significantly boost gold. I will update on this as it happens.

At this point, I am neutral on gold.

Be the first to comment