Back in January, I posted on SA that Sierra Oncology (NASDAQ:SRRA) had bucked the biotech bear market trend with the release of some unexpectedly positive data from its lead candidate Momelotinib (“MMB”) – an oral JAK inhibitor – in Myelofibrosis (“MF”).

Momelotinib is designed to treat patients with MF who also suffer with anemia – a common side effect of treatment with other JAK inhibitors approved for MF, such as Incyte’s (INCY) Jakafi, which earned $2.13bn of revenues last year.

Momelotinib achieved statistically significant benefits in total symptom score, anemia and splenic response compared with the steroidal therapy danazol for patients previously treated with an approved Janus kinase (JAK) inhibitor in its 195-patient, Phase 3 MOMENTUM trial, meeting all endpoints, and as I wrote at the time:

It has been clinically proven that patients with MF who also have anemia have a lower chance of survival than those that don’t, hence, it seems Sierra may have a chance not only of securing approval for Momelotinib as a second line therapy – perhaps less than 12 months from now – but also of positioning the drug as the new standard of care in MF treatment.

Analysts forecast peak sales as high as $1.7bn for Momelotinib, which has succeeded where other therapies could not in a notoriously difficult to treat disease, and that seems to have been enough to persuade the Pharma giant GlaxoSmithKline (NYSE:GSK) to part with $1.5bn to buy out Sierra and add Momelotinib to its late stage pipeline.

Sierra has not yet submitted its New Drug Application (“NDA”) for Momelotinib – a drug that it acquired from Gilead for an upfront payment of only $3m in 2018, after the Pharma abandoned development of the drug – despite its showing outperformance in anaemic patients against Jakafi in a Phase 3 study – owing to its failure to match Jakafi in Total Symptom Score (“TSS”).

Gilead’s loss has been very much Sierra’s gain – Sierra had been struggling somewhat prior to January’s data, and the company had completed a 1:40 reverse stock split in January 2020, but since reporting the trial success, its share price had climbed from a price of $15.5, to $38, before the GSK news sent the share price soaring to a high of $55 at market close Thursday, and a market cap of $1.3bn.

This is therefore a great deal for Sierra and its shareholders, since the biotech – which made a net loss of $94.6m in FY21, and reported a cash position of $105m, may well have struggled to take on Incyte and Jakafi even with a superior record in anaemic MF patients, and may not have had the funds to conduct further trials and push for a label expansion into first line therapy.

The mood amongst GSK shareholders may be different, however. Since there is little point buying Sierra shares at the present time – they are unlikely to budge from their current price unless the takeover looks to be in doubt for any reason – in the rest of this post I will examine the deal from GSK’s perspective, and the role it plays in management’s ongoing dispute, and attempts to appease, the activist shareholder Elliott Management, which has built up a multi-billion stake in the company.

Stagnant for 2 Decades, Elliot Capital Has A Plan to Revive GSK’s Share Price

According to TradingView, GSK’s share price hit its peak around 1998, of ~$70, but since 2010, it has rarely traded above $50, the last occasion being in 2014. At its current price of $46, GSK’s share price is +14% over the past 5 years, and +28% over the past year.

Elliot Management can arguably take some credit for the upturn in valuation over the past 12 months. The activist investor led by billionaire Paul Singer specialises in building positions in underperforming companies and agitating for change – previous companies targeted include the mining group BHP, and Alexion Pharmaceuticals, sold to AstraZeneca (AZN) last July in a $39bn deal – and now it is taking aim at GSK.

Under Emma Walmsley – who was promoted to the CEO position in 2017 after leading the company’s consumer healthcare division – GSK has opted to streamline its pipeline, searching for genuine “winners”, although these have been hard to come by, and elected to spin out its consumer health division, which is part owned by Pfizer (PFE) into a new entity, to be called Haleon.

In FY21, GSK earned revenues of $44bn, comprised of $23.1bn from its pharmaceuticals division, $8.9bn from its vaccines division, $1.83bn from “COVID solutions”, and $12.5bn from consumer health. Operating profit was $8.1, adjusted EPS $1.47, and free cash flow $5.8bn (all figures originally quoted in £, but adjusted to $ using xe.com).

Since Walmsley has taken over as CEO, GSK has reported revenues of $40.75bn, in 2017, $39.3bn in 2018, $44.7bn in 2019, and $46.6bn in 2020, whilst EPS grew from $0.48 in FY17, to $1.58 in 2020, before falling to $1.2 on a GAAP basis last year. GSK also pays a dividend of >$2 per annum, for a yield of ~4.5%. Market cap is ~$117bn.

These figures are by no means disastrous, but the lack of share price movement is clearly frustrating Elliott, who at one point called for Walmsley, who does not have a scientific background, having worked at L’Oreal for 17 years prior to GSK, to reapply for her job leading the pharmaceutical and vaccine divisions.

Ellliot’s first communication after taking a substantial position in GSK was a 17-page letter, in which the company suggested that:

GSK has an opportunity to generate up to 45% upside in its share price in the lead-up to its full separation, and much more in the years beyond

Elliott’s letter goes on to say that:

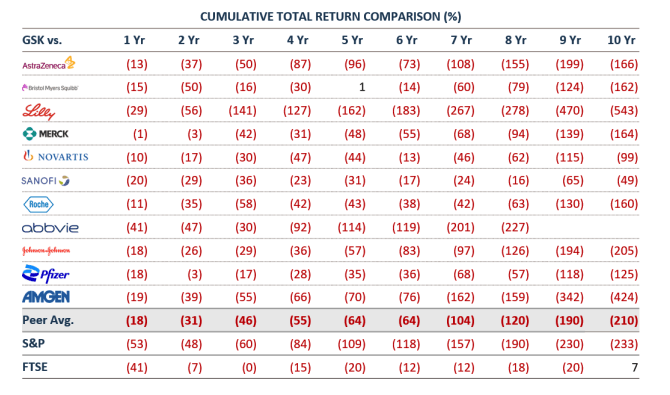

Despite the strengths of its people, its vaccines and its drugs, GSK has a poor record of execution and value creation. These shortcomings are clearly demonstrated in GSK’s share price, which has underperformed every single peer over nearly every conceivable timeframe. 1 Over the last ~15 years, GSK has dropped from being the third-largest pharma company to the eleventh-largest one. GSK’s share of total R&D spend has dropped by over 30%.2 These facts have led to scepticism about the Company’s future. In our view, this scepticism is inconsistent with GSK’s true potential

And shares the following chart:

GSK vs rivals – cumulative total return performance. (presentation)

Elliott wants to target growth of ~5% at a minimum and has approved of GSK’s decision to spin out its Consumer Health division, which contains brands such as Advil, Centrum, Sensodyne and Panadol, and generated $1.4bn of free cash flow in 2021, and $1.6bn in the prior year, according to a detailed February 2022 presentation.

Elliott has criticised GSK for paying too high a dividend, with uncertainty about rate cuts dissuading investors from building positions in the stock, and also the $5bn acquisition of Tesaro – developer of Zejula (niraparib), an oral poly ADP ribose polymerase (PARP) inhibitor currently approved for use in ovarian cancer in – in 2019, which they say cut the share price by 12% and is an example of poor management, as well as a lack of detailed planning for example within the HIV, division, and compared to rival Gilead Sciences, the $78bn market cap Pharma based in California.

A 5 point plan devised by Elliott for GSK begins with “Ensure the right leadership through the right process”, then Incentivise stronger performance and greater ambition”, improve profitability while investing more in R&D”, Display Openness to value-maximising pathways, and preserve vaccines and Pharma’s nimbleness”.

It may be worth noting that Elliott has in the past worked with both Alexion, acquired by AstraZeneca, and Allergan, acquired by AbbVie (ABBV), so it may not out of question that the firm will push for a sale of GSK’s business, which is an interesting prospect for the company, and for its shareholders.

GSK Management Responds, Including Via Sierra Acquisition & So Does Share Price – How High Can It Go?

In 2022 GSK has guided for:

growth in 2022 sales of between 5% to 7% at CER and growth in 2022 (on an ongoing business basis) and adjusted operating profit of between 12% to 14% at CER

and CEO Walmsley has commented that:

This is going to be a landmark year for GSK, with a step-change in growth expected and multiple R&D catalysts, including milestones on up to 7 key late-stage pipeline assets.

GSK’s forward Price to Earnings (“PE”) ratio is likely to be a little higher than its current one, given a shrinking net profit margin appears to be the forecast for 2022, but it is a competitive score anyway, as is a Price to Sales ratio of ~3.3x, which is below average for the Pharma sector, implying there is share price growth potential in play.

Last year GSK won approval for a new HIV drug, Apretude, a formulation of Cabotegravir, as the first long-acting injected option in the pre-exposure prophylaxis (“PrEP”) setting, and hopes that it can generate $2bn in peak sales, based on a second approval in combo with Johnson and Johnson’s (JNJ) Rilpirvine, via subsidiary business ViiV Healthcare. The new drug will compete against e.g. Gilead’s Truvada, which it has been judged marginally more efficacious than, and GSK’s hope is that many patients will prefer the less frequent dosing regime.

A second drug – Xevudy – was approved to treat COVID, although there are question marks over whether the drug is “fully active” against the BA.2 variant and its use has been halted in some states, and faces competition from the likes of Pfizer’s Paxlovid and Merck (MRK) / Ridgeback Pharma’s Molnupiravir. Still, sales are expected to reach $1.4bn this year, GSK believes.

A third drug approved last year, Jemperli – the seventh blocker of the protein PD-1 to be approved overall – in endometrial cancer is expected to deliver $2bn of peak sales, which will help GSK cushion the blow of an upcoming patent expiry of its leading HIV drug Dolutegravir, which makes nearly $5bn per annum for the company.

Again, it is not a bad performance from management, and by pushing through the Healthcare Division spin out – set to happen this year – and outlining her vision through a presentation at the JPM Conference, it may be that Walmsley is beginning to win Elliott over.

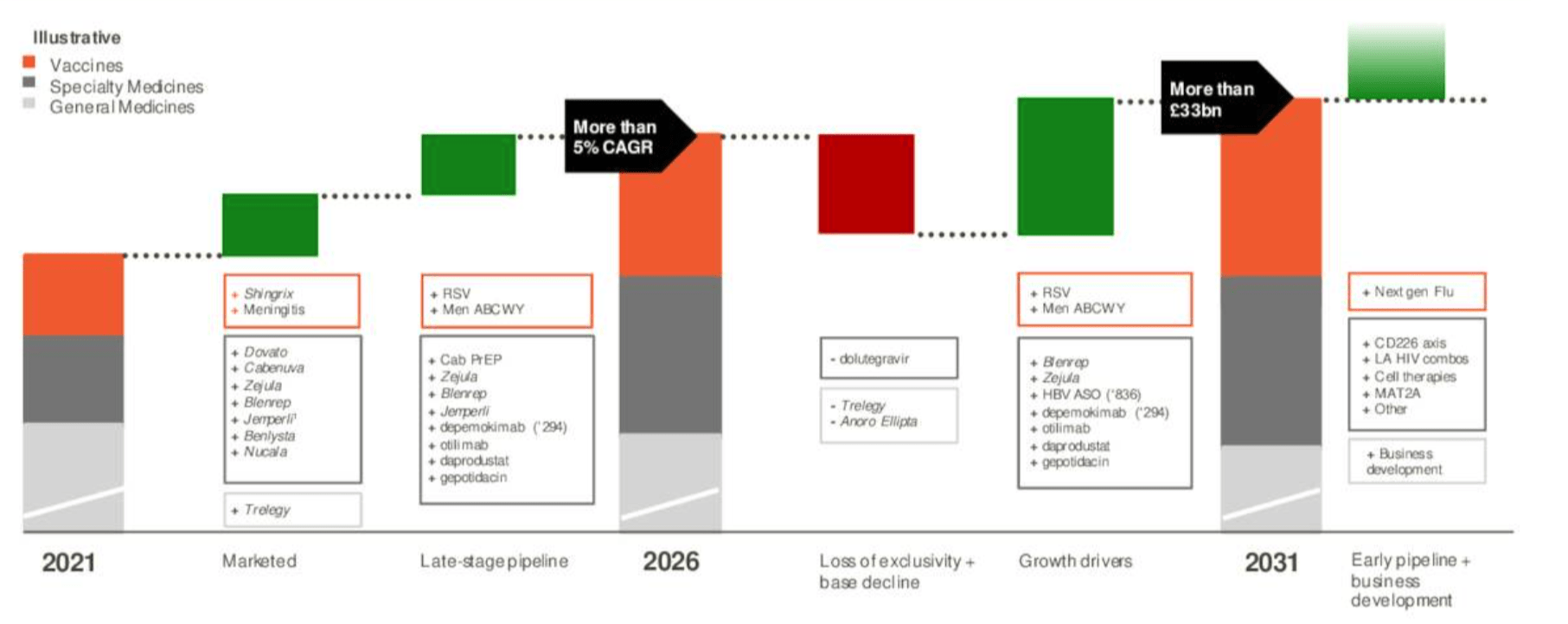

The plan is to get to $33bn sales by 2013 and there is a clear route to this, involving pipeline drugs – organic growth, in other words – as shown below:

GSK plans to reach $33bn revenues by 2031. (JPMorgan conference presentation)

Of course, there is no guarantee management will get there, but in terms of how specific GSK’s plans are, it reminds of both AbbVie and Bristol-Myers Squibb (BMY), who have outlined similar plans to compensate for drugs experiencing patent expiry – such as AbbVie’s Humira, and Bristol Myers Squibb’s Revlimid, by bringing through pipeline assets such as Skyrizi and Rinvoq, in AbbVie’s case, and e.g. Breyanzi, in BMY’s case, and another cell therapy, Abecma, targeting blood cancer.

Both AbbVie and BMY also completed major buyouts of rival Pharmas – Allergan, in AbbVie’s case, a deal worth ~$66bn, and Celgene, in BMY’s case, a deal worth >$70bn, and after an initial struggle, their share prices have been climbing – BMY after little or no movement in >5 years.

The prospect of M&A activity ought to be considered in relation to GSK in my view – a merger with HIV rival Gilead would make sense, for example, although that could be denied on anticompetitive grounds, or fellow UK based AstraZeneca, of perhaps teaming up with mRNA vaccine developers such as Moderna (MRNA) and BioNTech (BNTX) – GSK’s attempts to develop a COVID vaccine alongside French Pharma Sanofi (SNY) has been generally disappointing. M&A activity is picking up and after the separation of Haleon, GSK’s business is more streamlined, and cheaper to buy outright, with fewer complications.

Conclusion – The Activist Investor Elliott Likely To Be A Positive For GSK as Management Stands Up To The New Challenge

To summarise the above, Elliot Management’s interest in GSK ought to be able to continue to have a positive effect on GSK’s share price.

It has helped to encourage management to place its cards on the table and reveal where its growth is coming from after separating from the Consumer Healthcare division, which ought to be an interesting investment proposition for shareholders in the latter half of 2022 in itself.

The Sierra Oncology acquisition looks to be smart business based on paying $1.9bn for a company close to bringing a drug with ~$1.7bn peak sales expectations to market, and there is cash available for more M&A if necessary – GSK reported current assets of $18.6bn as of Q421, and has cashflow of ~$6bn per annum, although GSK does have $23.6bn of current liabilities also.

By most measures – PE and PS ratios, cash flow generation, net profit margins – GSK looks to be a favourable investment and there may be more to buying the company’s stock than a decent dividend and ~5% per annum growth potential. There is the spinout of Consumer Health, further pipeline progress, and perhaps even a sale or a mega-merger on the cards.

Elliott may push to reduce the dividend, and could be a little too short-term in the way that they view GSK, and how to maximise its potential – perhaps fattening the company up ahead of a sale is their main priority – but the majority of GSK’s business divisions appear to be performing well, which is encouraging.

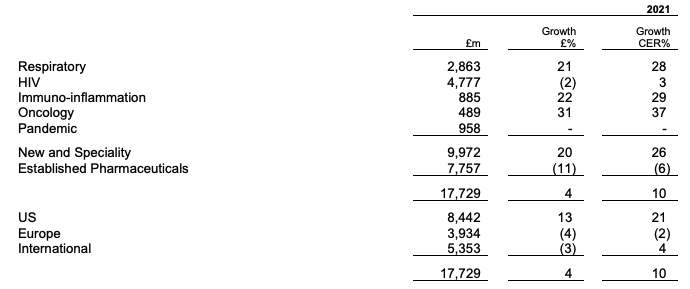

GSK by business division revenues. (presentation)

GSK by business division revenues. Source: GSK 2021 results press release.

The pharmaceutical sector has performed reasonably well over the past 12 months, while the biotech markets have been in turmoil with most companies delivering double-digit share price growth. GSK’s growth has been +22% – only Pfizer, Eli Lilly and AbbVie’s share price performance has been better – but I think there may yet be still to come from the stock, and would advise keeping a careful eye on its movement going forward in 2022.

It could either drop or surge after the split with Haleon, which ought to happen this year. If it is a drop, I would invest nonetheless, as that may be the last opportunity to acquire GSK stock <$40, and personally, I would consider an acquisition or merger price for GSK could be at a market cap valuation as high as $150bn, or <5x forward price to sales, or a premium of 28% to current share price.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment