Evgen_Prozhyrko/iStock via Getty Images

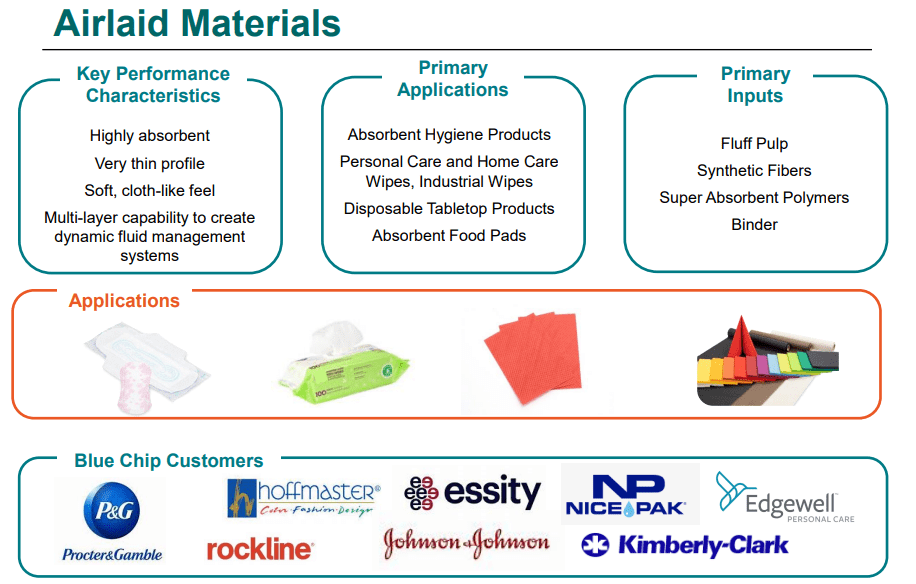

Glatfelter Corporation (NYSE:GLT) manufactures engineered materials used by global corporations in high-profile consumer and industrial products. The items here include composite fibers for tea bags, single-serve coffee containers, and specialty laminates. The company also produces “Spunlace” as a non-woven fabric with applications for baby wipes, skincare, and even cleaning supplies. There are also “Airlaid” materials that are highly absorbent with a cloth-like feel found in hygiene products.

The setup with the stock follows what has become a familiar story with the company facing significant inflationary cost pressures in 2022 hitting earnings beyond slowing sales amid the challenging macro backdrop. Indeed, GLT is down a horrific 80% over the past year with concerns regarding its liquidity which forced a dividend suspension back in Q2.

That being said, an ongoing restructuring including efficiency efforts and price hikes is expected to set to drive margins higher as a tailwind for improving earnings. We see 2023 as a make-or-break year for the company with several uncertainties but ultimately some room to turn cautiously bullish on the stock highlighting a turnaround strategy. While certain segments have underperformed, Glatfelter maintains some strong points in its operating trends supporting a more positive long-term outlook.

GLT Key Metrics

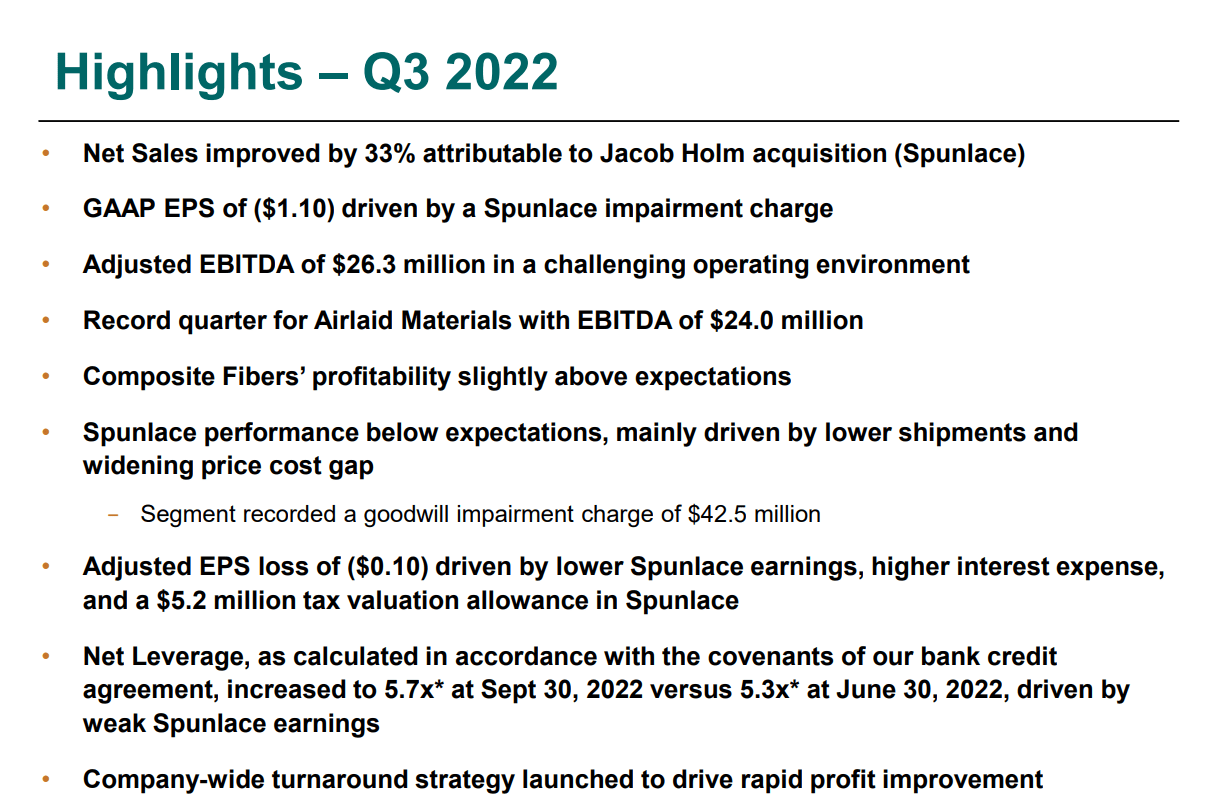

The company last reported its Q3 earnings in November with a headline EPS loss of -$0.10 which reversed a profit of $0.21 in the period last year. Top line revenue of $372 million was up 33% y/y, although the context is the contribution from the company’s 2021 acquisition of “Jacob Holm”, a specialty Spunlace manufacturer marking the company’s entry into the segment. At the same time, the deal has largely disappointed thus far evidenced by a large impairment charge of $42.5 million to the unit reflected in the GAAP loss of $-1.10. Total organic sales volumes are lower.

source: company IR

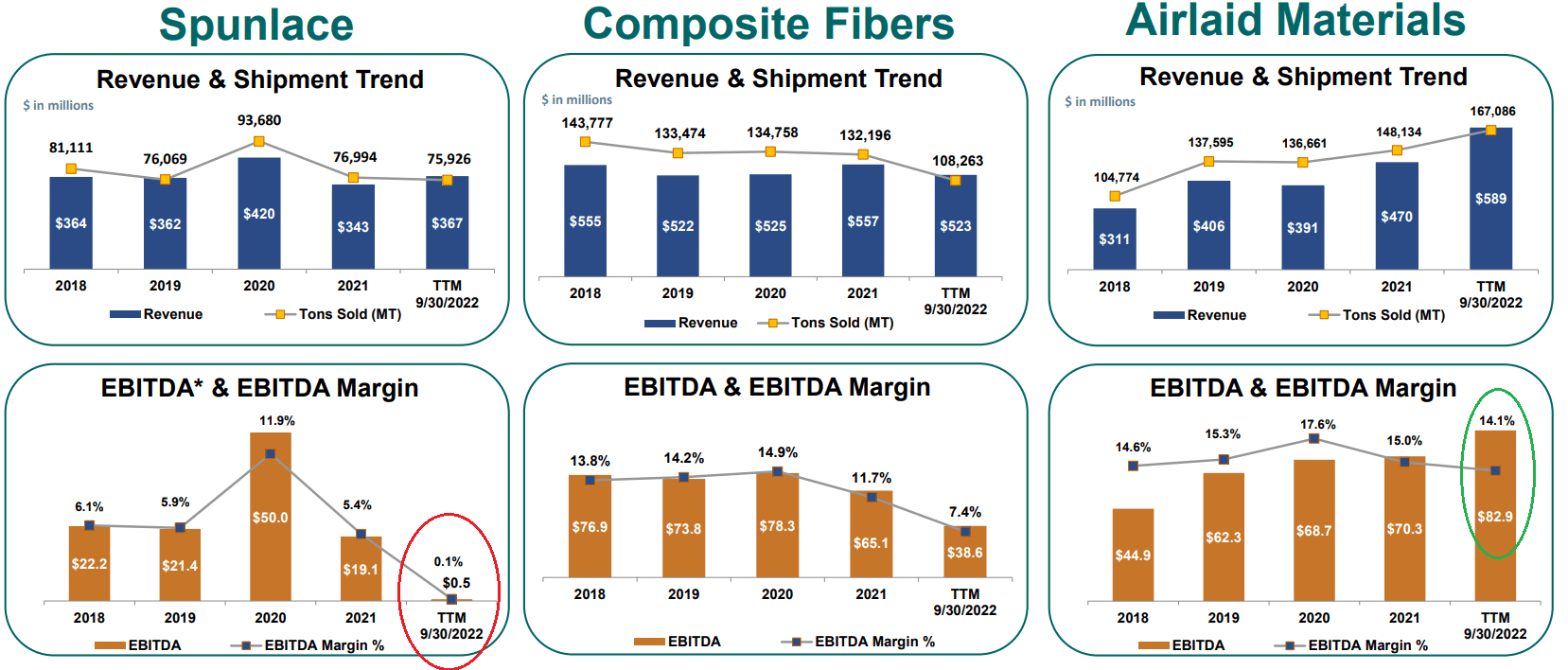

From the graphic below, one takeaway is that the core Airlaid materials group has been a strong point with sales up over the past year driving a record level of segment EBITDA at $82.9 million in the trailing twelve-month period. Part of the momentum reflects a contribution from the company’s other 2021 acquisition of “Mount Holly” with solid demand in North America.

On the other hand, the Spunlace segment is the weak point with a collapse in the EBITDA margin to just 0.1% over the last year through the end of Q3. Management explains a widening cost gap with the company stuck fulfilling a large contract at a fixed-price even as supply chain disruptions added significantly to costs. The company also faced labor market challenges at North American manufacturing sites adding to expenses. Separately, Compositive Fibers shipments have also been weaker with a direct impact from the Russia-Ukraine conflict limiting shipments in the region.

source: company IR

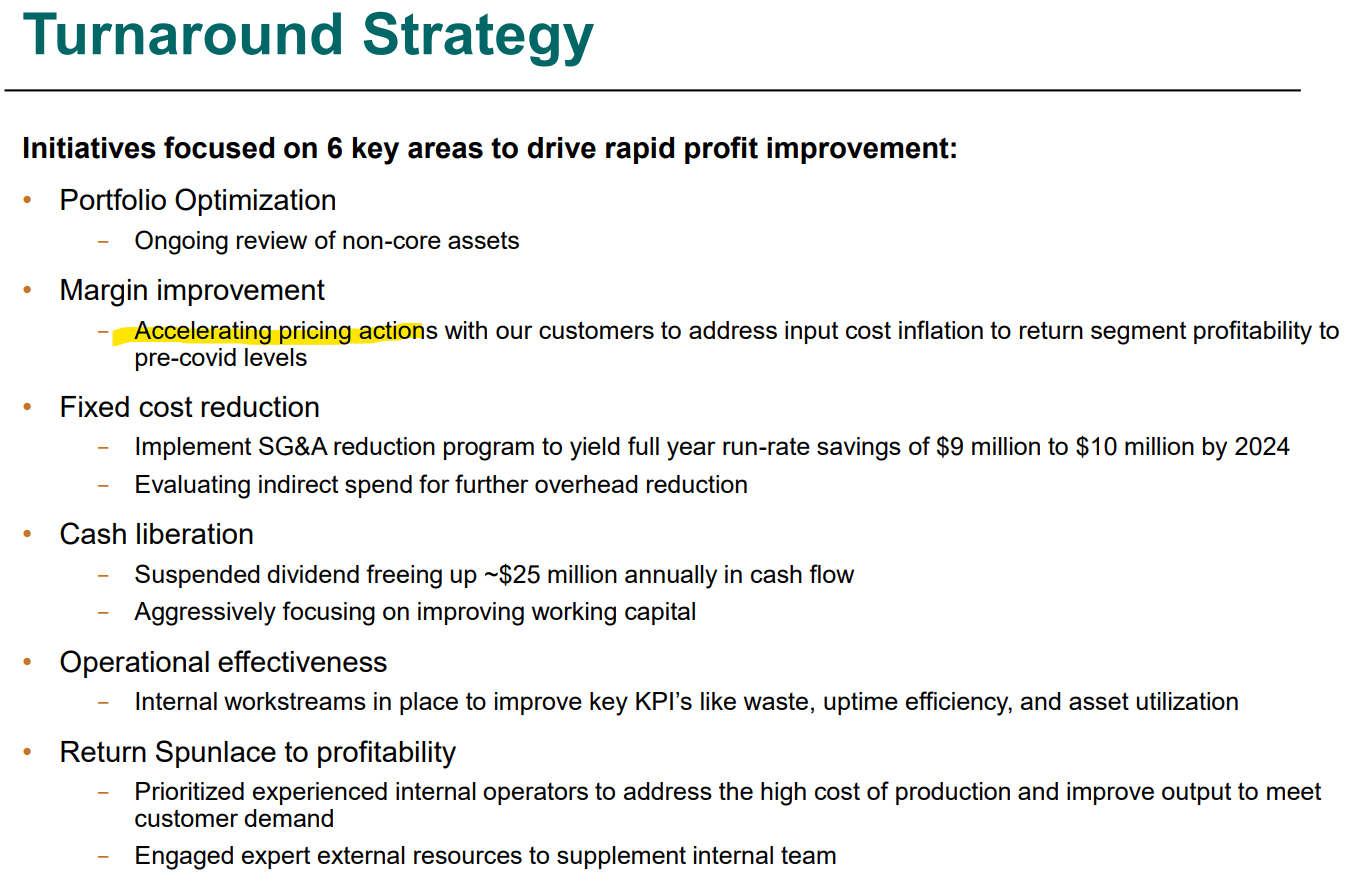

To address the challenges, management is moving forward with various initiatives to reclaim higher profitability. In addition to the dividend cut last year, the plan includes optimizing the product portfolio, capturing operational efficiencies, and targeting upwards of $10 million annually in fixed-cost savings by 2024. For us, the area that stands out is the use of accelerating pricing hikes going forward.

Again, the sense we have is that Glatfelter sort of fell behind the curve in 2021 and into 2022 by not raising prices fast enough in response to input cost inflation. Into 2023, the expectation is that existing customer contracts will be renegotiated and some of these efforts will add to the top-line momentum over the next few quarters expected to support higher margins.

source: company IR

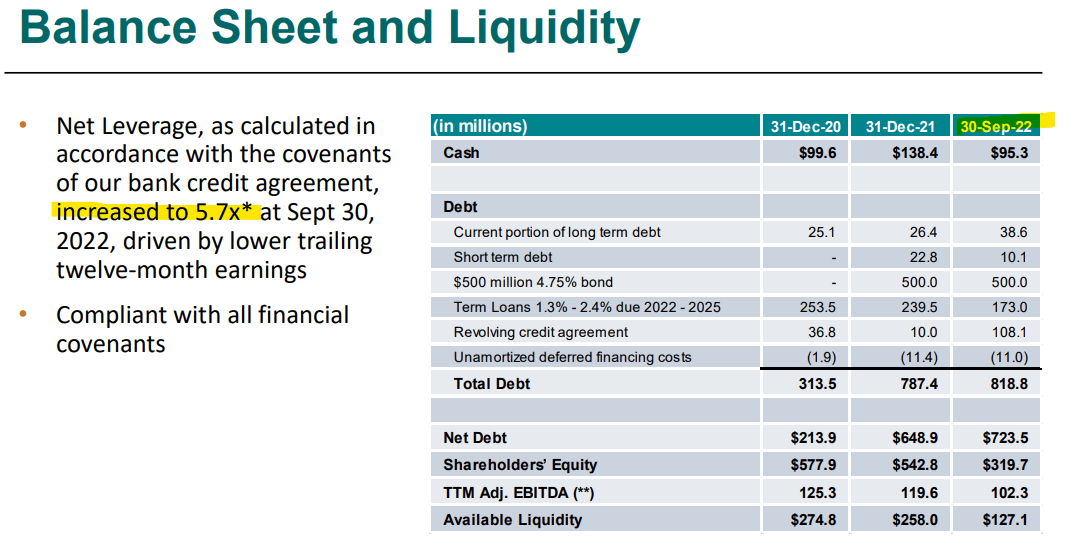

Putting it all together, operational trends leave a lot to be desired but are otherwise stable. The bigger crutch for Glatfelter comes down to its highly leveraged balance sheet, which ended the quarter with $819 million in total debt against $95 million in cash.

While management confirms the 5.7x net leverage ratio is compliant with existing loan covenants, the long-term solvency and the weight of nearly $5 million in quarterly interest expenses help to explain the stock price performance over the past year.

Comments during the last conference call suggested an outlook for EBITDA between $23 million and $26 million for the yet-to-be-reported Q4. This level tracks similarly to Q3 but the expectation is to capture some stronger financial momentum through 2023. The way we see it, there is room to manage the situation, but it will be important for earnings and cash flow to improve sooner rather than later.

source: company IR

What’s Next For GLT?

Beyond the turnaround strategy initiatives, the other side to the discussion is the relief the company may benefit from easing inflationary cost pressures as a broader macro trend. Lower energy prices, in particular, compared to the first half of 2022 will not only cut logistical costs but also limit expenses related to electricity at the company’s factories. All these tie into a roadmap where stronger margins going forward can add to profitability and help improve the company’s balance sheet position.

Keep in mind that much of the debt is related to strategic acquisitions that have proven to be successful at least on the Airlaid materials side. Avoiding new types of deals in the near term can add to financial flexibility. Overall, this is a case where the company’s segment leadership and global logistical network including industry relationships work in its favor to provide a sense that recovery is possible.

The list of “blue-chip” customers across consumer staples and healthcare giants reflects the value of the business and its specialized products but also highlights some of the exposure to broader cyclical trends. Most companies have seen softer demand while citing macro headwinds, which remain a risk for Glatfelter in a scenario where global economic conditions deteriorated further.

source: company IR

GLT Stock Price Forecast

Balancing our positive view of the company, our outlook for the stock considers that we’ll need to first see some evidence the turnaround strategy is working. We rate GLT as a hold, which means it’s probably too late for long-term investors to sell, while there doesn’t appear to be a good near-term catalyst for shares to break out higher. Any financial turnaround will likely take several quarters to confirm success.

Seeking Alpha

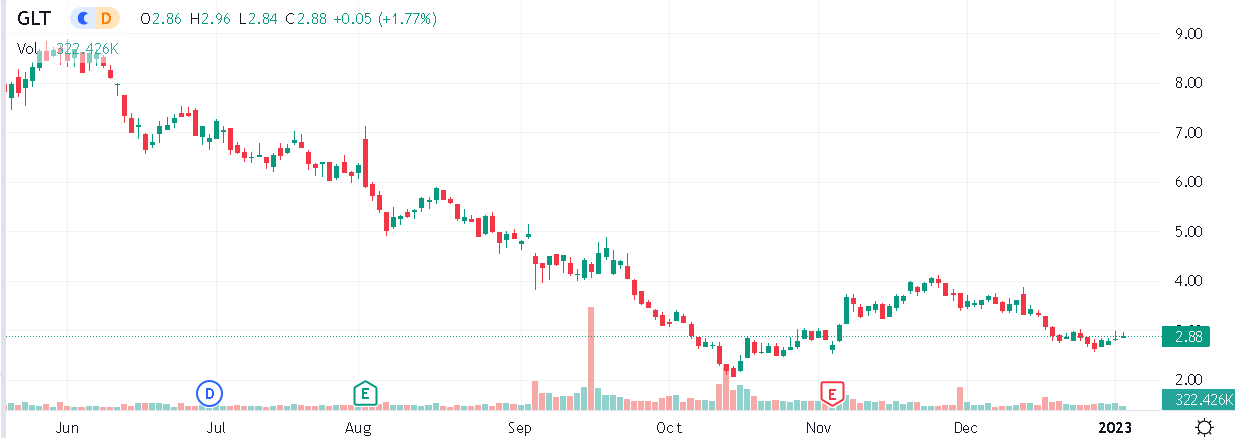

Looking at the chart, it’s encouraging that shares have rallied from their lows in October. Holding the $2.00 level of technical support will be critical for the bulls to maintain some momentum. To the upside, GLT will need to climb above $4.00 as a technical buy signal, nearly 40% higher than the current level. The base case is an expectation for volatility to continue. Again, a wait-and-see approach on GLT is likely the most prudent course of action.

The biggest risk here is that financials continue to underperform, while recurring negative cash flows would force the company to consider a new capital raise as dilutive to existing shareholders. Into the Q4 earnings set to be released on February 3rd, monitoring points will be any sign organic sales are stabilizing along with the adjusted gross and operating margin. A positive 2023 guidance from management would go a long way to help the stock climb higher.

Be the first to comment