Justin Sullivan

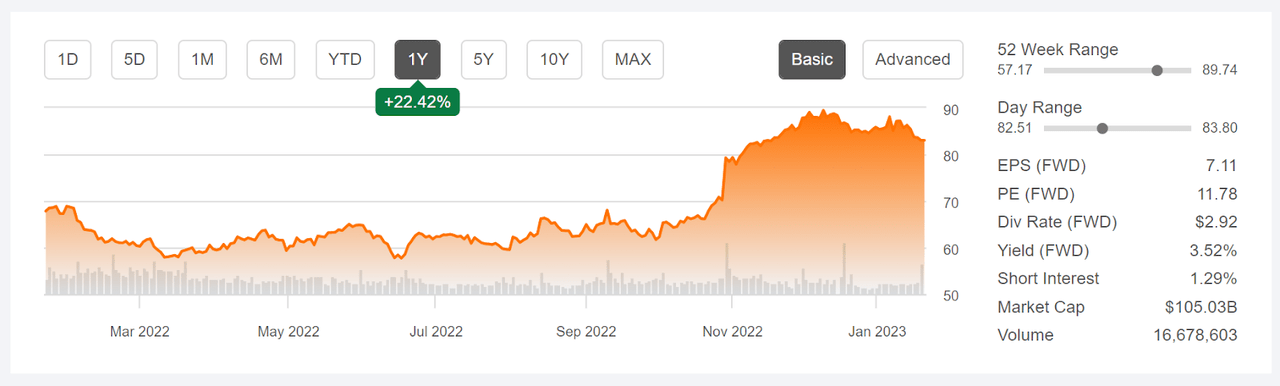

Gilead (NASDAQ:GILD) had little movement for most of 2022, but rallied substantially following strong Q3 results, reported on October 27th. Thanks to this surge, GILD has a trailing 12-month total return of 26.7%, as compared to 3.97% for the Healthcare Select SPDR (XLV) and 4.03% for the iShares Biotechnology ETF (IBB). GILD is the 15th-largest holding in XLV and the largest holding in IBB. The late-2022 rally makes GILD look fairly expensive, and RBC recently downgraded the stock to Sector Perform because of the higher valuation.

Seeking Alpha

12-Month price history and basic statistics for GILD (Source: Seeking Alpha)

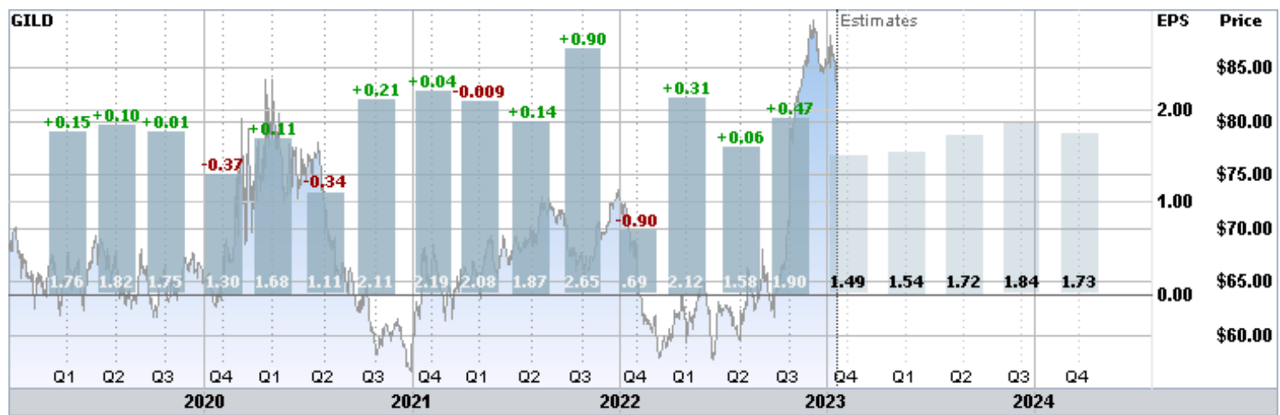

GILD’s earnings for Q3 of 2022 had EPS exceeding the consensus expected value by 33%. Sales of Veklury, an antiviral drug used to help COVID-19 patients, continued to be a big contributor. The company reported total product sales of $7 Billion for Q3, of which Veklury contributed $0.9 Billion. Sales of Veklury were lower than for the same period of last year, but revenues excluding Veklury were up 11% YoY. Sales of Biktarvy, a treatment for HIV/AIDS, totaled $2.8B, 22% higher than for Q3 of last year. The company recently announced a 5.9% price increase for Biktarvy. The company also reported a 16% gain in YoY sales of Descovy, a pre-exposure prophylactic (PrEP) drug that reduces the probability of contracting HIV from sex.

Longer-term, GILD’s earnings growth is expected to be fairly anemic. The consensus outlook for EPS growth over the next 3 to 5 years is low, at 2.97% per year and the company has a Seeking Alpha Growth Grade of F.

GILD reports Q4 results on February 2, 2023.

ETrade

Trailing (4 years) and estimated future quarterly EPS for GILD. Green (red) values are amounts by which EPS beat (missed) the consensus expected value

GILD has a forward dividend yield of 3.52% and trailing 3- and 5-year dividend growth rates of 5.0% and 7.0% per year, respectively. If we can extrapolate these dividend growth rates forward, the Gordon Growth Model would suggest that GILD can plausibly return a total of 8.5% to 10.5% per year. For context, the trailing 10- and 15-year annualized total returns for GILD are 10.0% and 10.38% per year, respectively.

I last wrote about GILD on June 22, 2022, about six months ago, when I changed my rating from neutral / hold to bullish / buy. At the time, GILD was trading at $59.93. From the market closing price on June 22nd, GILD’s total return (including dividends) is 37.6% vs. 6.7% for the S&P 500 (SPY). The Wall Street consensus rating was a buy, with a consensus 12-month price target that corresponded to an expected 12-month total return of 21%. The market-implied outlook, a probabilistic price forecast that represents the consensus view from the options market, was bullish to mid-January of 2023 and slightly bullish to the middle of 2023, with expected volatility of 27% (annualized). As a rule of thumb for a buy rating, I want to see an expected 12-month total return that is at least half of the expected volatility. Taking the Wall Street consensus at face value, GILD was well above this threshold. Even with the fairly high valuation and low longer-term growth expectations, I upgraded GILD to a buy because of the strong consensus outlooks from the Wall Street analysts and from the options market.

For readers who are unfamiliar with the market-implied outlook, a brief explanation is needed. The price of an option on a stock reflects the market’s consensus estimate of the probability that the stock price will rise above (call option) or fall below (put option) a specific level (the option strike price) between now and when the option expires. By analyzing the prices of call and put options at a range of strike prices, all with the same expiration date, it is possible to calculate the probable price forecast that reconciles the options prices. This is the market-implied outlook. For a deeper discussion than is provided here and in the previous link, I recommend this outstanding monograph published by the CFA Institute.

I have calculated updated market-implied outlooks for GILD and compared these with the current Wall Street consensus outlook in revisiting my rating.

Wall Street Consensus Outlook for GILD

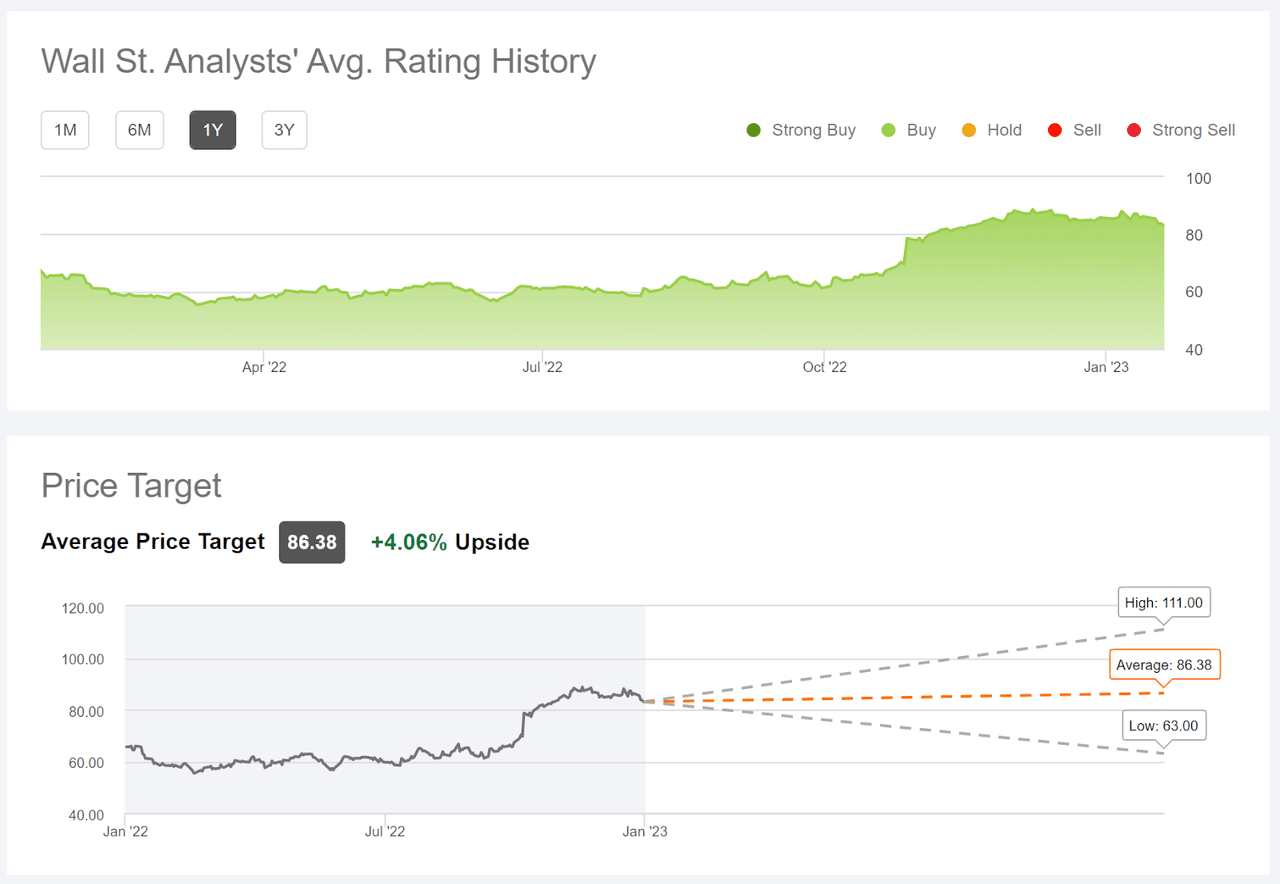

Seeking Alpha calculates the Wall Street consensus outlook for GILD using ratings and price targets from 29 analysts who have published opinions in the past 90 days. The consensus rating is a buy and the consensus 12-month price target is 4.06% above the current share price, corresponding to a total return of 7.58%. GILD’s strong rally has effectively priced in a lot of the potential upside for the year.

Seeking Alpha

Wall Street analyst consensus rating and 12-month price target for GILD (Source: Seeking Alpha)

Of the 29 analysts included in the consensus cohort, 18 assigned a hold rating, 3 gave the stock a buy rating, and the remaining 8 had a strong buy rating.

Market-Implied Outlook for GILD

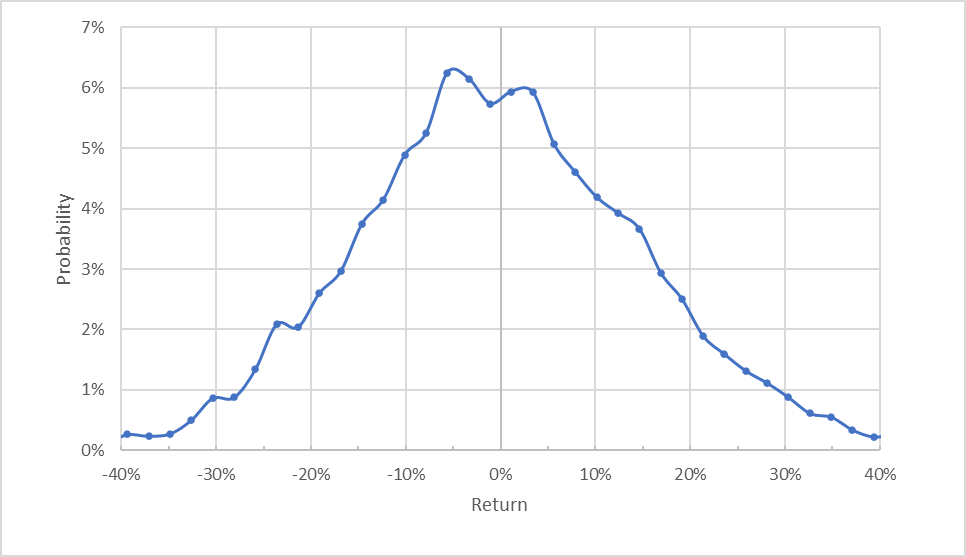

I have calculated the market-implied outlook for GILD for the 4.7-month period from now until June 16, 2023 and for the 11.8-month period from now until January 19, 2024, using the prices of call and put options that expire on these dates. I selected these specific expiration dates to provide a view to the middle of 2023 and through the entire year.

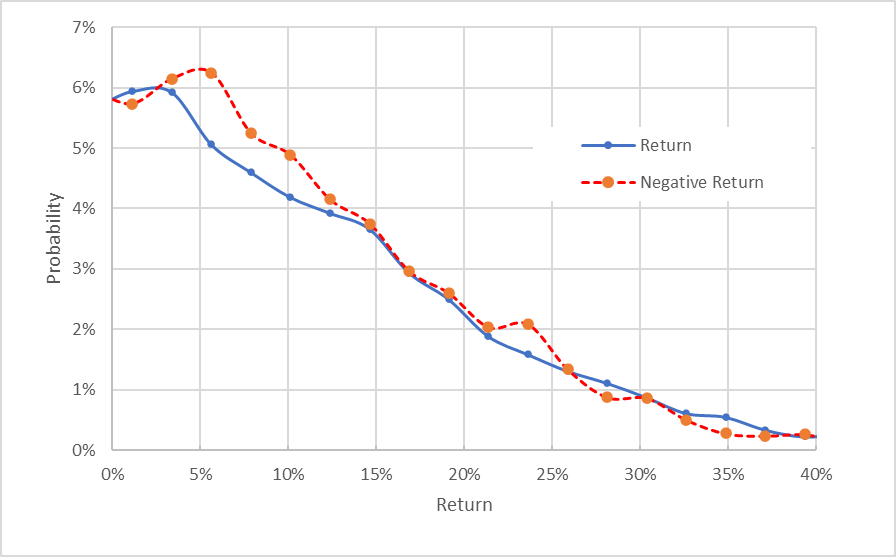

The standard presentation of the market-implied outlook is a probability distribution of price return, with probability on the vertical axis and return on the horizontal.

Author’s calculations using options quotes from ETrade

Market-implied price return probabilities for GILD for the 4.7-month period from now until June 16, 2023

The market-implied outlook is generally symmetric, with comparable probabilities of positive and negative returns of the same magnitude, although the maximum probability is slightly tilted to favor negative returns over this period. The expected volatility calculated from this distribution is 26.9% (annualized), very close to the expected volatility I calculated in June, 27%.

To make it easier to compare the relative probabilities of positive and negative returns, I rotate the negative return side of the distribution about the vertical axis (see chart below).

Author’s calculations using options quotes from ETrade

Market-implied price return probabilities for GILD for the 4.7-month period from now until June 16, 2023. The negative return side of the distribution has been rotated about the vertical axis

This view highlights the close match in the probabilities of positive and negative returns over much of the range of possible outcomes (the dashed red line is very close to the solid blue line over most of the chart), although the probabilities of negative returns are somewhat elevated for a range of the most-probable outcomes.

Theory indicates that the market-implied outlook is expected to have a negative bias because investors, in aggregate, are risk averse and thus tend to pay more than fair value for downside protection. There is no way to measure the magnitude of this bias, or whether it is even present, however. The expectation of a negative bias suggests a neutral interpretation of this market-implied outlook.

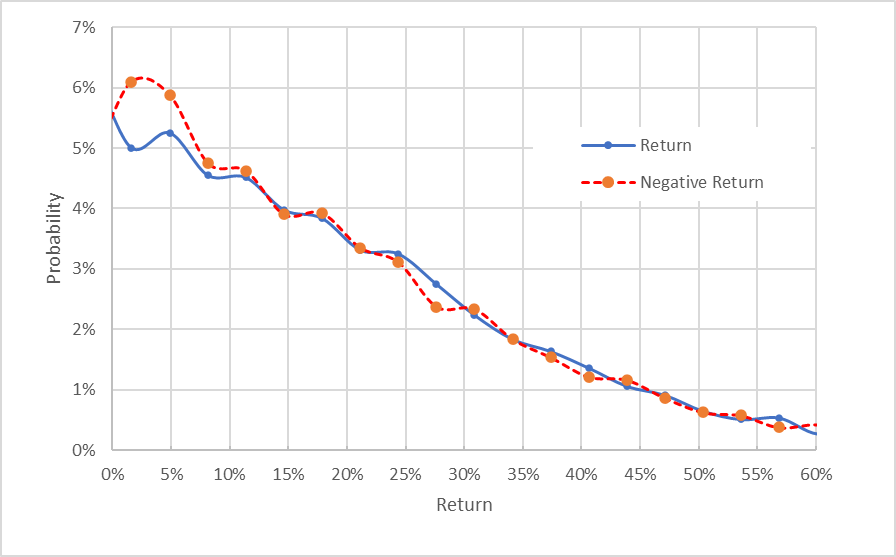

The market-implied outlook for the next 11.8 months exhibits an even closer correspondence between positive and negative return probabilities (the solid blue line and the dashed red line are right on top of one another over almost all of the chart below), although there is a very small region with higher probabilities of negative returns. The expected volatility is 28.3% (annualized). Because of the expectation of a negative bias, this outlook is best interpreted as predominantly neutral.

Author’s calculations using options quotes from ETrade

Market-implied price return probabilities for GILD for the 11.8-month period from now until January 19, 2024. The negative return side of the distribution has been rotated about the vertical axis

At that time that I pulled the options quotes used here, GILD was priced at $83.01. The bid price for a call option with a strike of $82.5, expiring on January 19, 2023, was $9.10. Buying the shares and selling this call, provides net income of $8.60, after accounting for the fact that the strike price is $0.49 below the current share price. Adding the expected $2.92 in dividend payments between now and January 19, 2024, the expected total income corresponds to an income yield of 13.9%. This covered call position means that you have sold off all of the potential upside over the next year, of course.

Summary

Gilead ended up delivering impressive returns for shareholders in 2022, although these gains only manifested fairly late in the year. The prevailing outlooks from both Wall Street and the options market were favorable for much of the year. With the substantial increase in the share price, however, the shares have priced in a lot of good news. The Wall Street consensus rating continues to be a buy, but the consensus price target implies a total return of 7.6%. This level of return is not very attractive for a stock with expected volatility of 27% to 28%. The market-implied outlook for GILD is predominantly neutral to the middle of 2023 and for the full year. I am changing my rating on GILD from bullish / buy to neutral / hold. Gilead has done a great job on multiple fronts, but the share price is too rich for me to assign a buy rating for 2023.

Be the first to comment