Sundry Photography

Introduction

Chips are a new commodity in today’s world, and many semiconductor companies are taking advantage of them. ASML (ASML) develops machines that can produce chips; it is considered the leader in developing chip machines because it has a monopoly on them.

Chip designers like Broadcom (NASDAQ:AVGO) aim for maximum efficiency in all aspects of a chip’s operation, from power consumption to thermal management. The design is then sent off to a chip manufacturer like TSM (TSM), where it is manufactured. With a $530 billion market size and a projected 12% CAGR, the semiconductor industry is a major economic force.

In terms of revenue, Broadcom ranks as the sector’s fourth-largest player. The company digital and analog semiconductors and interfaces for networking equipment, SOCs for hard drives and offers enterprise software.

The company is riding the wave of Apple’s (AAPL) popularity as Apple is its largest customer, but it risks losing Apple as a customer because of the intense competition in the market.

A Bite Of An Apple

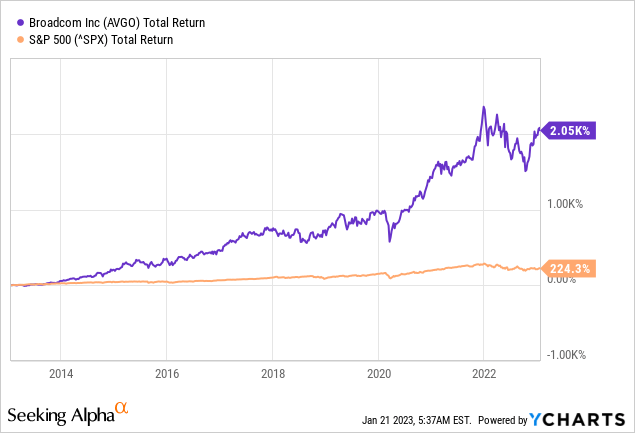

Sales of Apple products have risen sharply over the past decade as more users prefer the Apple ecosystem to that of Android (GOOGL)(GOOG) and Microsoft (MSFT). With Apple as Broadcom’s largest customer, Broadcom has seen strong growth in revenues and profits along with growth in sales of Apple products. The stock price has risen along with the strong earnings growth, with total returns averaging 36% per year over the past 10 years.

Now that Broadcom’s customers want to develop their own chips, the company is exposed to greater risks.

About 20% of Broadcom’s revenue comes from Apple, which makes it Broadcom’s most important customer. Apple has the financial resources to design its own chips, which will reduce costs and could boost product performance.

Apple has announced that by 2025, they will no longer use the Broadcom chip that manages Wi-Fi and Bluetooth connectivity. Apple itself is developing a similar chip with the same capabilities and plans to use it in its devices by 2025. Broadcom faces a significant threat from Apple’s plans to develop its own chips.

Since Apple has announced that it will create its own Wi-Fi and Bluetooth chips, Broadcom can expect less revenue from Apple. However, Broadcom will still supply Apple with components like RF chips and wireless charging module chips.

Earlier, Apple abandoned Intel’s (INTC) chips in its products. But looking back at the introduction of Apple’s M1 chip, several reports noted that Apple’s silicon is 3.5x faster than Intel’s top chips. So yes, it was to be expected that Apple would switch to making its chips in-house. But the risks to Broadcom remain high.

Broadcom’s CEO remains optimistic because Broadcom has the most advanced technology on the market. Hock Tan, CEO of the firm, wrote the following:

And we’re still very, very well positioned in our product line — in those few product lines that are, I call it, almost franchise in our North American customers. And this is Wi-Fi, Bluetooth, this is RF front end, and this is touchscreen controllers, high performance, mixed single. And that’s — we can only — and that’s all we focus on because these are areas where we are the best, we believe we have the best technology and delivering value to our customers. There’s no reason to find something else where you’re not the best and hope to gain share from someone else. I could apply the same to my competitors in their thinking.

In addition, Apple is also developing a combined chip that combines Wi-Fi, Bluetooth and a cellular modem in one chip. This means there is also significant risk to QUALCOMM (QCOM), which is the main supplier of cellular modem chips for Apple devices.

Designing chips is a difficult process because each chip has unique characteristics. Since Apple has already tried (and failed) to design Qualcomm’s own cellular modem chips, I don’t think Apple will design all the chips itself.

Every chip has its own design tricks, and Apple isn’t really in the business of designing chips. Intel similarly attempted but failed to create 5G cellular modem chips. When Intel halted its own efforts to develop a 5G cellular modem chip, Apple purchased the team and their assets.

In contrast, Qualcomm has spent over a decade perfecting the 5G standards and the technology that will power its 5G modems, and it has had unrivaled success in developing and commercializing previous generation cellular modems.

I seriously doubt that Apple will design all its chips in-house due to the wide variety of design requirements and manufacturing processes required for each type of chip.

Let’s go back to Broadcom. Apple has contracted Broadcom to create their RF chips and wireless charging module chips for the coming years. So how difficult is it to develop these chips? According to a document provided by Texas Instruments (TXN), the following problems can arise during the design of RF chips:

- High EMI

- Reduced antenna efficiency

- Failed government certifications

- Excessive power consumption

Quoted from Texas Instrument’s document:

A critical aspect of regulatory certification is EMI emission testing. Throughout the design process it is imperative that a system meets these requirements to receive approval from regulatory agencies such as the Federal Communications Commission (FCC) in the U.S., the European Union’s CE or Japan’s TELEC. Unfortunately, this can be difficult to achieve as expensive testing equipment costs more than $100,000 and outsourcing can range between $1,000 to $2,000 per hour.

Once designers are confident that an RF design will pass certification testing, it must be submitted to a government-approved lab-where additional fees are incurred. The total cost of certification varies by application, but typical estimates range from $30,000 to $50,000 and requires approximately six months.

Another problem that often arises during RF development is design failure. The cause might be insufficient wireless connectivity range, impaired throughput or any other metric that didn’t meet system specifications. Whenever a performance problem is discovered, extensive testing and debugging must then be done to determine the root cause, again adding more costs and delaying time to market.

Thus, I highly doubt that Apple will produce Broadcom’s RF chips internally due to the complexity of their design. When it comes to Broadcom’s wireless charging module chips, I haven’t been able to determine if they are challenging to design.

Although Broadcom (and other chip designers) faces competition from its own customers, investors must accept this risk. Broadcom stands to lose 20% of its revenue if Apple goes ahead with plans to develop all of Broadcom’s chips in-house.

I believe that Broadcom will still retain at least a portion of the 20% of its revenue that comes from Apple.

Broadcom operates in a strong growing market as total addressable market is expected to expand at a CAGR of 12% over the next few years. Broadcom provides semiconductor solutions for the powertrain, ADAS, infotainment system, and body electronics of electric vehicles, so the industry’s demand for chips is expected to rise in tandem with the booming EV market. The future looks promising for Broadcom.

Dividends And Share Repurchases

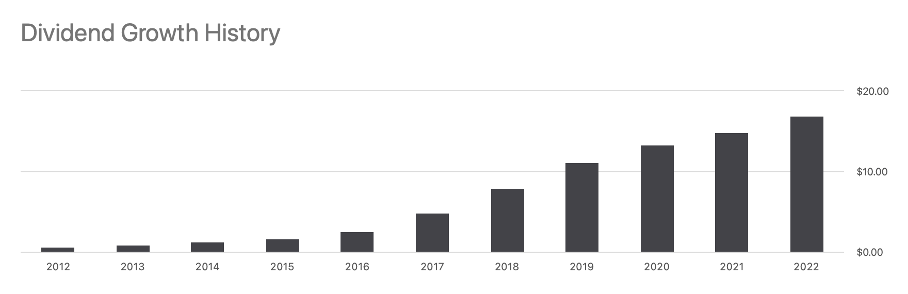

Broadcom’s growth over the past decade has been substantial, and the company has been rewarding shareholders with a large portion of its cash flow. The dividend per share has increased due to rising free cash flow and due to share repurchases. Average annual dividend growth of 41% has taken the dividend per share from $0.61 in 2012 to $18.40 in 2022. The dividend yield is 3.3% at the current share price.

Dividend growth history (Seeking Alpha AVGO ticker page)

Broadcom is returning a lot of cash to its investors. The vast majority (94%) of the $16 billion in free cash flow generated in 2022 was distributed to shareholders as dividends and stock buybacks. The dividend payment will rise from $3.3 billion in 2018 to $7 billion in 2022.

With a repurchase yield of 4.2%, the $8.5 billion spent on stock buybacks in 2022 is impressive. The remaining balance of the company’s share repurchase authorization as of today is $13B. This equates to a yield of 5.4% on share repurchases at the present time.

Broadcom’s cash flow highlights (SEC and author’s own calculations)

Broadcom’s free cash flow is higher than its total return to shareholders, so the company can afford to pay dividends and repurchase shares indefinitely.

Broadcom’s Stock Looks Attractive

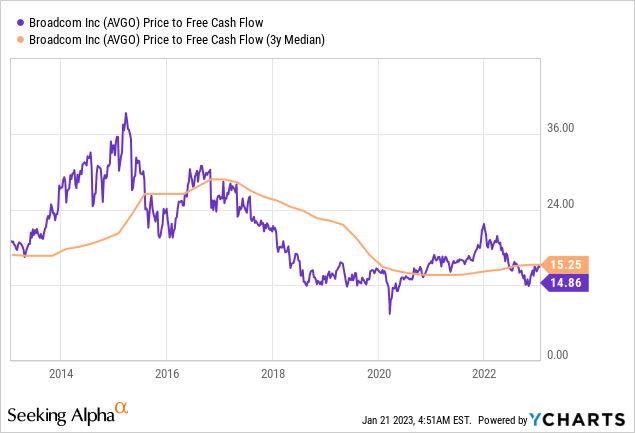

At last, the stock’s worth is assessed. Given the extremely high free cash flow margin (49%) I opt for the price to free cash flow. The ratio of the company’s current price to its free cash flow (14.9) is more attractive than its historical value of 15.3 (also from a valuation perspective).

In the coming years, EPS growth to the mid-teens is projected. Because sales of semiconductors typically fall off sharply toward the end of a business cycle, there are still some risks associated with the company. Micron’s (MU) sales have varied over the years, and now analysts predict a drop of nearly 50% for the current fiscal year.

Both Broadcom and Micron are semiconductor industry players, but Broadcom is in a different niche than Micron. Over the past decade, Broadcom’s sales have remained relatively stable, falling by only a fraction of what Micron’s have.

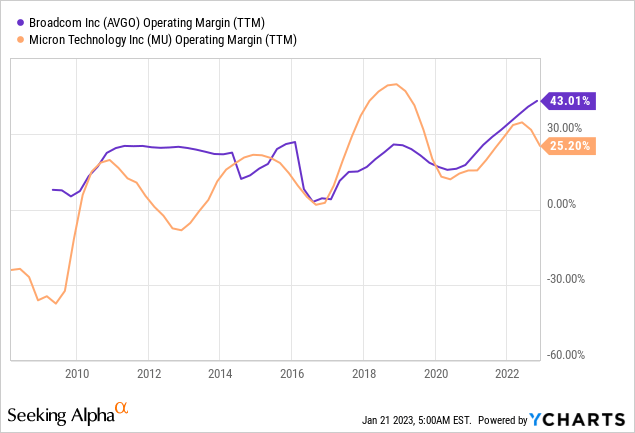

We use the operating margin to identify fluctuation in earnings. The margins today are at an all-time high, as can be seen in the chart below. Over the past 13 years, the operating margin has consistently been positive, with 2009 and 2016 being the worst years. However, Micron has had negative operating margins in both 2009 and 2012 because of its increased overhead expenses. Investing in Micron is likely riskier than in Broadcom.

Conclusion

There are plenty of options for investors looking to put their money into the semiconductor industry. Broadcom is well-positioned in a sector where the total addressable market is expected to increase by 12% annually over the next few years as semiconductors have become increasingly important in recent years.

Broadcom is a market leader in communications chips, making it a key supplier for Apple. Broadcom has seen healthy revenue and profit growth thanks to Apple, its largest customer. This also poses a risk because Apple will now design its own Wi-Fi and Bluetooth module chips.

Some have speculated that Apple will replace all Broadcom chips in its products, but I do not believe this is the case. Broadcom’s RF chips are very complex, making it challenging for Apple to develop them in-house. Because of this, Broadcom will only lose some of Apple’s revenue.

Broadcom is an efficiently run business. Over the past decade, Broadcom’s profit has been consistently high and growing. Although operating margins are currently at record highs, they have not been negative for quite some time. The stock’s dividend is rising, and the stock’s price is favorable compared to historical figures.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment