Victor Fraile/Getty Images Entertainment

Overview

G-III Apparel Group, Ltd. (NASDAQ:GIII) is a textile company that designs, sources, and markets apparel for men and women in the U.S. and internationally.

The company has two operating segments: Wholesale Operations and Retail Operations. GIII sells various products including outerwear, dresses, sportswear, swimwear, women’s suits, and women’s performance wear; women’s handbags, footwear, small leather goods, cold weather accessories, and luggage.

The company also markets apparel and accessories under its proprietary brands, including DKNY, Donna Karan, Vilebrequin, Eliza J, Jessica Howard, Andrew Marc, Marc New York, Sonia Rykiel, Black Rivet, G-III Sports by Carl Banks, and G-III for Her.

In addition, GIII also has licensing deals with well-known brands such as Calvin Klein, Tommy Hilfiger, Karl Lagerfeld Paris, Levi’s, Guess?, Kenneth Cole, Cole Haan, Vince Camuto, and Dockers. The company also has licensing deals with many popular sports leagues, including the National Football League, Major League Baseball, National Basketball Association, and National Hockey League, as well as 150 U.S. colleges and universities.

The company sells its products through multiple channels, including department, specialty, and mass merchant retail stores. The company also sells its products online. G-III is headquartered in New York City and was founded in 1956.

Performance

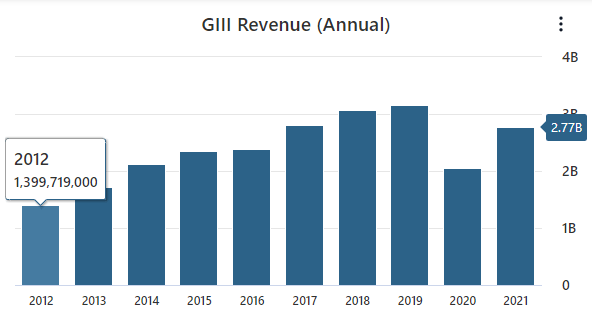

GIII has established a nice track record of revenue growth over the past decade. For fiscal 2021 the company reported $2.7 billion in revenue which represents an exceptional 34% growth year over year. Over the last ten years, GIII has almost doubled its revenues, growing 92% during the period. It’s impressive how consistent the company’s revenue growth has been over the last ten years as it only reported an annual revenue decline once during 2020, when revenue dropped -34% as the business was hit hard by the pandemic.

Data by Stock Analysis

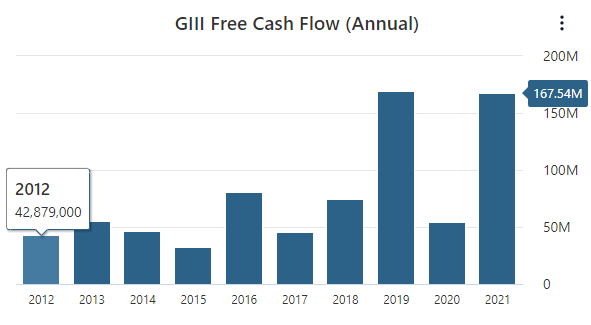

In terms of free cash flows, GIII has also established a nice track record of growth however the company’s free cash flow growth has been much more inconsistent. In 2021, the company reported $167 million in free cash flows representing 206% growth year over year. This outstanding growth is due to a relatively easy comparison since 2020 free cash flows were heavily influenced by the COVID-19 pandemic. Overall, the company has grown free cash flows by almost 300% over the past ten years.

Data by Stock Analysis

In addition, GIII is also reported high returns on invested capital as it’s averaged over a 17% ROIC over the last decade. However it’s important to note that from 2012-2015 the company averaged a much higher ROIC of 26%, therefore GIII’s profitability has been declining in recent years. Today, GIII is not achieving higher returns on equity than its peers, it’s ROE lags behind the sector median by -10.76%.

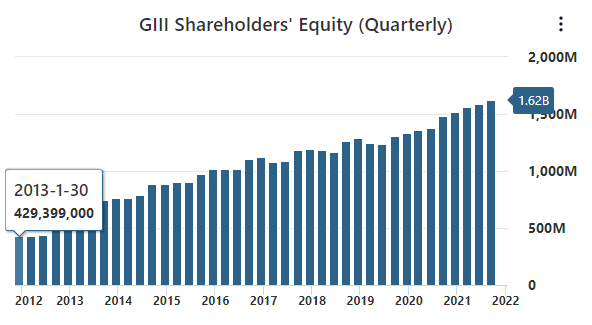

Turning to the company’s balance sheet, GIII has done an excellent job of increasing shareholder’s equity, which currently stands at $1.6 billion. The company has increased shareholder’s equity at a steady pace, recording an impressive overall growth of 478% over the past 10 years. The company also sports a current ratio of 3.09 and debt-to-equity ratio of 0.69 therefore the company is backed by a strong balance sheet.

Data by Stock Analysis

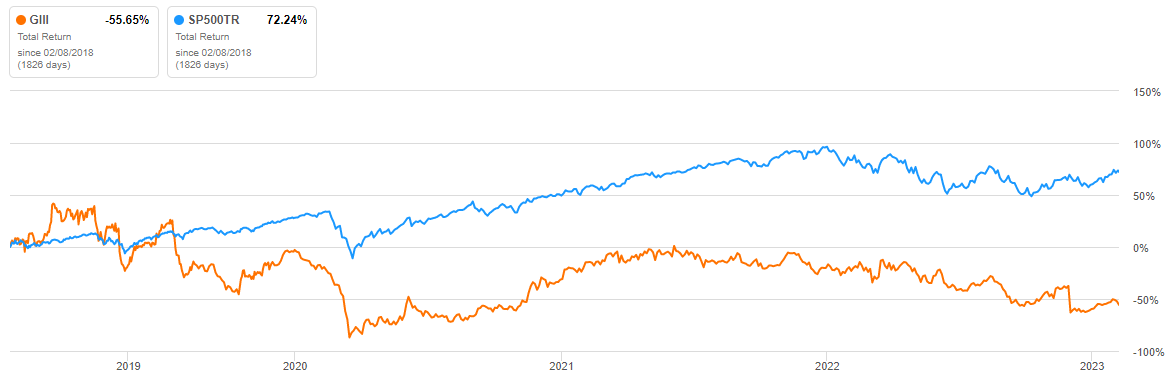

Overall, the company has demonstrated a strong history of financial success. However, this impressive performance has not translated to shareholder gains. The total return of the S&P 500 has significantly outperformed GIII over the last five years, 72% gain to -55% loss. This poor performance is making many GIII shareholders question if the company can turn things around.

Data by Seeking Alpha

Outlook

A substantial portion of GIII’s revenue comes from the sales of licensed products from the Calvin Klein and Tommy Hilfiger brands. During the nine months ending October 31, 2022, sales from these brands made up approximately 48.2% of our overall revenue. In 2022, they accounted for 50.7% and in 2021, they made up 53.5% of the company’s revenue. It can’t be understated how much these two brands mean to GIII.

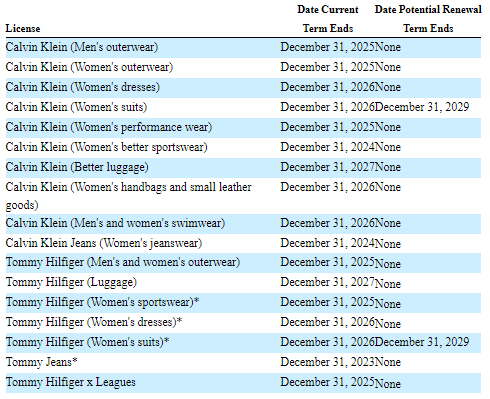

PVH Corp. (PVH) owns the Calvin Klein and Tommy Hilfiger brands and it plans to start making these products on their own when the licensing deals with GIII expire. The licensing deals are broken down by category with the earliest licenses expiring on December 31, 2023, and by year end 2027 most of the licenses will have expired. See below for a breakdown of the expiration dates.

Data by GIII 3Q22 10Q

If GIII cannot significantly boost sales of its other products or secure replacement licenses from different brands, then not renewing the agreements with Calvin Klein and Tommy Hilfiger will lead to a substantial drop in sales. The company is working on ways to grow its existing brands, both owned and licensed, by expanding into new categories, regions, and digital platforms. GIII is also looking for growth in new areas, like creating its own brands, growing in Europe, finding new licensing deals, and acquiring more businesses.

This is an ongoing situation, and more will come from GIII’s management regarding how they will make up for the loss of Calvin Klein and Tommy Hilfiger. GIII’s current Chairman and Chief Executive Officer remains optimistic about the future and had this to say during the company’s most recent earnings call.

We have found the most difficult component in building a new brand is finding the right people. We have that done. We have the right people. There is not one bit of change that needs to be made. Scouting for talent in this environment that’s acclimated to the culture that we have, that will remain the same, and it will be reinforced with brand ownership.

On a positive note, for shareholders, in March 2022, GIII’s board of directors decided to increase the number of shares the company can buy back to 10 million. From January to October 2022, the company bought back 811,874 shares for $16.6 million. As of December 1, 2022, the company still has the authority to buy back over 9 million shares which represents nearly 20% of the remaining 47 million total shares outstanding.

Valuation

To estimate GIII’s intrinsic value, a comparative and discounted cash flow (“DCF”) analyses will be used. The comparative analysis will consist of taking the highest, lowest, and median price-to-book value ratios the market has paid for GIII over the past five years and multiplying them by GIII’s current book value. As a bonus, the current sector median price to book value ratio of 2.35 will also be applied to GIII’s current book value for an additional valuation.

| Scenario | P/BV | Current Book Value | Intrinsic Value Estimate | % Change |

| Bear Case | 0.1674 | $34.16 | $5.72 | -61.60% |

| 5Y Median P/E | 1.026 | $34.16 | $35.05 | 135.38% |

| Bull Case | 2.226 | $34.16 | $76.04 | 410.68% |

| Sector Median Valuation | 2.35 | $34.16 | $80.28 | 439.13% |

On a comparative analysis, GIII has a wide range of scenarios that can play out. Investors could realize a substantial 410.68% return if the market were bullish and applied the 2.226 P/BV ratio, seen in 2018, to the company’s current book value of $34.16. On the downside, investors could realize a significant -61.6% loss if the market were to value GIII at the 5-year low P/BV seen in 2020.

The most likely scenario is the base case, which is based on the 5-year median P/BV ratio. This base case scenario would result in a 135.38% return for investors. The final scenario which is based on the sector median P/BV results in another substantial 439% gain. Altogether, this comparative analysis indicates that GIII is significantly undervalued as of now.

Turning to the discounted cash flow analysis, the starting point will be the average of the last five years of free cash flows, which is $102 million. The growth rate is difficult to predict with the loss of Calvin Klein and Tommy Hilfiger business in the coming years. To be conservative a 0% growth rate will be used over the next ten years. Therefore, this DCF will assume that in ten years GIII will earn 38% less free cash flows than the company earned last year.

Following the 10th year, a 2.5% growth rate will be used into perpetuity to determine the terminal value. A discount rate of 10% will be used, representing my personal required rate of return. With these inputs, the DCF analysis estimates GIII’s intrinsic value is $23.33, representing an upside of 56% from the company’s current share price. Therefore, this DCF analysis confirms that GIII is significantly undervalued at its current share price.

Author’s Work

Takeaway

GIII has established a solid track record of growing revenues, free cash flow, and shareholder’s equity. Still, it faces a new challenge as it will lose the Calvin Klein and Tommy Hilfiger business, which make up roughly half the company’s sales. However, this has already been priced in as the company’s stock has lost roughly a third of its value since announcing that PVH will not renew the Calvin Klein and Tommy Hilfiger licensing agreements as they expire over the next few years.

With GIII’s stock currently trading at less than half of its book value, the company resembles a modern-day cigar butt stock, the kind of stock that a young Warren Buffett bought at the beginning of his career. Yet the company is not overburdened with debt and is not burning through its free cash flow. A comparative and DCF analysis confirm that GIII is oversold and offers investors a significant upside. Now is an excellent time to start building a position in GIII.

Thank you for reading!

Be the first to comment