Baiploo/iStock via Getty Images

Dear Investors,

The stock market was down 19% this year. High inflation caused the central bank to raise interest rates to attempt to bring it in check, and those higher interest rates rippled through the economy and asset prices.

I did not do a good job picking stocks this year, and our equity investments are down ~25-30%. The one area that helped us somewhat is that I kept a more conservative mix between equities and government bonds than normal, so most portfolios are down ~20-22%.

In this letter, I’ll discuss my primary mistake for the year – buying growth stocks at the wrong time – and how that has led to poor results and missed opportunities. I’ll also examine the performance of the companies that we currently own, the current market environment, and how I’m attempting to position us to achieve our long-term goals.

A Year of Missed Opportunity

Looking back on 2022, it strikes me as a year of missed opportunity. It should have been a great year for us. While the stock market as a whole was down significantly, if you look under the hood, the stronger companies that I prefer to invest in have generally done well while the more speculative ones that we avoid have done the worst. That should have been an environment amenable to my style of investing, and the results from this year should have been good.

We didn’t outperform this year, like we should have, because over the past couple of years I slightly changed my investing style right at the wrong time and made some avoidable mistakes.

Over my career, I have tended to buy stocks where a good portion of the future return would come from the cash flows that those businesses are currently earning. In financial lexicon, those would be considered “value” stocks. I would try to make sure that these businesses were durable and would be able to reliably increase their earnings over time, but few of them would be characterized by high expected growth.

From when we started investing together in 2012 until last year, that style of investing had performed okay when done correctly, but investors who bought companies with strong expected future growth had generally done phenomenally well. Our results up to that point had been good, but they could have been much better if I had been willing to pay higher prices upfront to buy some of those faster growing companies that had performed so well as a group.

Late last year and early this year, for the first time in seemingly forever, the stock prices of some great growth companies dropped meaningfully from their highs. I was excited as I thought some of these stocks offered good long-returns from those levels, and we could finally own more in the way of growth stocks, which had driven such great performance.

I invested some of our available cash into these growth stocks based on my estimation of their ability to generate good returns over the next 5-10 years, but I got the timing wrong. These stocks have gone down materially since my initial purchases, and we have underperformed for the year largely because of those decisions.

Long-Term Performance Record

If I rewind back to the end of 2019, we had been investing together for 7 years, and over that time we had outperformed the stock market by roughly 3% per year after fees and taxes. After mediocre years in 2020 and 2021, and after a poor year in 2022, I have given away all that outperformance, and our equity portfolios have now performed roughly the same as the stock market since inception 10 years ago.

When I started managing money professionally, I hoped and expected to do better than this, and I admit to being frustrated at my performance over the past three years.

2022 has been especially difficult as the mistakes I made were psychological – chasing the hot thing after it had dropped a little bit. Over the course of my career, while I have made mistakes, I have usually avoided that one. I didn’t learn a new lesson this year. I did something I know I shouldn’t do. The lesson is just that it’s easier to make this mistake than it seems.

Missed Opportunities and Mistakes

The silver lining, to the extent that it exists, is that these mistakes didn’t permanently derail any of our financial goals.

I do financial planning with all of you, and my biggest focus every time we do that exercise is to make sure that any money that you’re going to invest in the stock market with me is money that you don’t need for a long time. There is always risk lurking in stocks, and I never want any of you to be in a situation where you’re forced to sell your stocks after a year in which we’ve lost money, thereby turning temporary losses into permanent ones.

As most of you know, I tend to be a quite conservative financial planner, recommending large cash cushions for your family and/or business needs, keeping that money safe and liquid, paying down debt balances, and only marking the remainder of your money as available to invest in stocks. I hold some cash even in that remainder, as an extra fail-safe. A year like this, when the stock market is down significantly and I also have a bad year, is why I advise you all in that way – none of you are forced to sell your stocks and crystalize your losses.

This planning lets us focus on the long-term with the money that you all have invested with me, and as I often write in these letters, our long-term investment results will mostly be a function of the performance of the businesses that we own. I paid too-high prices for some investments late last year and this year, but if those businesses do well over time, we can still make reasonable returns on those investments.

While it is true that the poor performance this year is less costly given our long time horizons, that fact is not a let-off. We are still worse off for me having made the decisions I did.

A few investments are down ~40-50% from my initial purchase price. Let’s just say for simplicity that I bought 1 share of something at $1 and it now trades at $0.50. If this is just a temporary blip and the price goes back to $1 relatively soon, then it is true that we didn’t lose any money. But if I had been more patient, I could have kept the money in cash, bought 2 shares at $0.50 each, and we would end up with $2 and a very nice gain.

At the very least, even if the current drops in prices on our investments are temporary, buying them at $1 and seeing the price drop to $0.50 is a significant missed opportunity. However, if the market is pricing the stock correctly and it’s truly worth $0.50, then that’s a bad mistake and we’ve permanently lost money. As I’ll describe in the next section, I believe that most of the companies that we’ve lost money in are still poised to perform well over time and that the prices will recover. I wish I’d been more patient in buying them.

It is true that the stock market is volatile, individual stocks more so, and that these things can be difficult to predict. And if you can’t predict where stock prices will go, then how could you expect to never buy something that has a significant, if only temporary, drawdown?

Part of my job is to understand where prices of individual stocks might go in certain circumstances. Some stocks will be much less volatile than others. Some will react worse in certain economic environments. I knew that growth stocks will perform poorly in a period of rising interest rates. Last year, I also knew that at some point, interest rates would need to increase and that would surprise the market. Buying too many growth stocks and watching them drop in value like this was completely predictable.

Trading Activity, Our Current Portfolio, and Business Performance

After discussing generalities, it will be helpful to look at the specific issues in our portfolios.

I will first look at the stock returns and business results of the companies that we have owned for at least two years, which have done reasonably well as a group even with a couple of business-specific challenges.

After that, I will look at the newer investments into growth companies that I’ve spent most of this letter discussing. These are the investments where we have lost money.

Consistent with last year’s letter, I’m going to keep this discussion relatively short in the main letter and put more detail in a technical appendix at the end of the letter. This section will provide a good summary for how our businesses performed in 2022 and how that performance affected their returns for the year. If you have some understanding of financial terms, then the technical appendix will provide more insight.

Let’s first look at the results of these businesses that we’ve owned over longer time periods:

Our largest position, Constellation Software (OTCPK:CNSWF), was down 16% in 2022. Constellation continues to consistently execute its playbook of running its large stable of software companies well, generating lots of cash, and using that cash to acquire more software companies and drive earnings growth. This year, Constellation showed an impressive ability to significantly increase its acquisition spend while still generating the great returns from these acquisitions that it has seen historically. Even during a year where the business performed very well, the stock is down somewhat, but its excellent execution means that it has outperformed most of its peers.

Transdigm’s (TDG) stock returned 1% this year as the company continued to execute well and generate profits even with still depressed travel demand. Earnings have risen well above their pandemic trough and are slated to keep increasing as long as air travel continues to normalize back to pre-pandemic levels.

Berkshire Hathaway (BRK.A, BRK.B) returned 4% this year as the company continues to create value consistently and conservatively. Berkshire should continue to be a relatively safe way to make a good long-term return.

This year, Charter (CHTR)has been our largest loser among our longer-held investments, with the stock down 48%. The company’s performance this year has been adequate, with our share of earnings rising, but the outlook for the next few years has clearly deteriorated compared to what investors were expecting last year, which has deservedly sent the stock lower.

Charter is a great business with the best bundled offering of home internet and mobile phone service of any carrier, which is what initially attracted me to it. However, there has been plenty of new competition from two areas – some companies are building more fiber internet in direct competition with Charter’s internet offering and due to new technological advancements, wireless phone companies can now also offer home internet connectivity.

In my estimation, Charter will still be able to grow over time, even with this increased competition. If it does continue to grow, today’s prices will prove to be very cheap given the significant cash flows that the company generates.

That being said, the future outlook is more uncertain than it was last year, and there is a world where all of this incremental competition impairs Charter’s profitability and its value.

There is uncertainty and risk in every potential investment. My job is to only buy an investment when the risk/reward skews favorably and to diversify enough that a bad outcome in any one place doesn’t ruin the whole portfolio. I believe the current risk/reward here is, in fact, quite favorable, but I’ll continue to closely monitor the situation to make sure that our entire portfolios aren’t harmed too much if some of the risks play out.

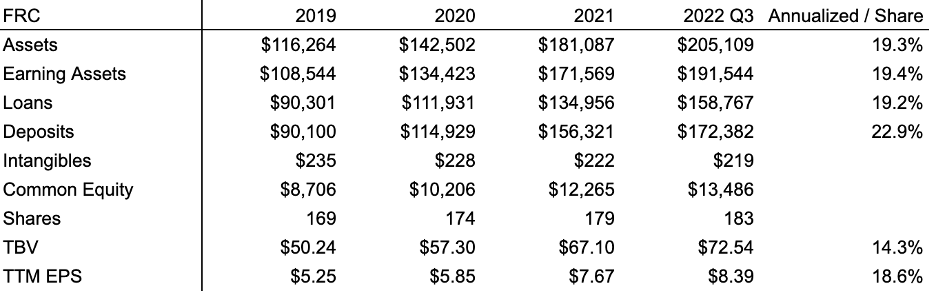

First Republic Bank (FRC) has also grown well this year, increasing its deposits, earning assets, loans, and earnings. However, the stock is down 41% as the near-term outlook for earnings is challenging.

Normally, banks benefit when interest rates go up because interest rates that the banks earn on loans increase while rates that banks pay on deposits increase much less, thereby increasing margins. First Republic, in contrast to a normal bank, caters exclusively to high-net-worth clients with large deposit balances. When interest rates go up, it’s easier for these clients with large deposits to move that money into higher-yielding alternatives. First Republic has had to pay more to its depositors than I anticipated to keep those deposits, and those increased deposit costs will hurt margins and earnings next year.

Unlike Charter, this is not a long-term competitive issue. First Republic might be able to earn somewhat less than I thought in higher interest rate environments, but the outlook for the company is still bright and the bank should be able to continue to grow over the long-term. The stock’s performance this year is mostly a function of an expensive valuation coming into the year paired with these near-term challenges.

I will briefly touch on a few of our smaller positions. Enterprise Products Partners (EPD) returned 19% this year as energy stocks performed well along with oil prices. Visa (V) and Mastercard (MA) each lost 3% and outperformed most other high-quality growth names as increased worldwide travel boosted high-margin cross-border spending, which translated to strong revenue and earnings growth. S&P Global (SPGI) lost 28% as its core credit ratings business has slowed due to higher interest rates. This is to be expected from time to time as this business is cyclical, but we have done well over the life of our investment as I initially bought shares at an attractive valuation.

Looking at these businesses that we’ve owned for longer periods as a group, it was hardly a perfect year especially given the challenges in cable, but it would have been a pretty good one. The equities would have outperformed the stock market in aggregate and the large cash balances would have contributed to even smaller losses for our portfolios.

Let’s now look at the newer positions that mainly drove our struggles for the year:

We have owned Google (GOOG, GOOGL) for 3 years, but I’m going to put it into this “new investments” section as I’ve added money to it consistently throughout this year, and we are down on those purchases.

Google had a mixed year with good revenue growth in its core ads business but lower margins leading to roughly flat earnings. Investors’ main worry with Google is that in the case of a likely recession next year, Google’s earnings will potentially drop by a significant amount.

These worries, along with the macro environment, have sent the stock down 38% for the year. Importantly, if we look longer-term, the outlook for the next 5 years is roughly unchanged compared to a year ago, and if that outlook comes to fruition, shares should prove to be quite undervalued today.

Amazon (AMZN) has had a difficult year, with excess cost in its retail business and slowing growth in its cloud infrastructure business leading to a 49% decline in its stock. The issues at Amazon are similar to Google in that investors are mostly worried about what the next 1-2 years look like.

In its retail business, Amazon ramped investment during the COVID pandemic as they tried to ensure that they had enough capacity to deliver goods to consumers during a time of rapidly accelerating demand. As these pandemic effects waned this year and consumers shifted to more normal spending patterns, ecommerce growth has slowed significantly and the company has had excess capacity and excess costs, pushing down its profits.

Importantly, the retail business is still growing, they are taking steps to adjust their cost structure, and I’d expect Amazon to match demand with capacity at some point soon, although it’s impossible to predict exactly when. At that point, it should start to generate healthy profits.

Amazon’s cloud infrastructure business, AWS, had another good year with strong growth, margins, and earnings. Even so, the stock has gone lower as expectations for growth have slowed materially next year due to lower overall software growth and a weakening economy.

Current issues aside, I still have high confidence in Amazon’s retail business and in AWS over the long-term. They are both profitable, growing, durable, high-quality businesses. It might take some time for these issues to improve but once they do, we should do well owning shares.

Radius Global Infrastructure (RADI)has had a mixed year. The company has two main parts of its business – it owns ground leases that sit underneath cell towers, and it employs a large investment organization that finds and purchases new leases.

The real estate portfolio has performed as expected this year, growing rents and starting to see a nice boost in its growth rate from its inflation-linked escalators. The investing organization has also done well, deploying significant sums into new leases at attractive prices.

Radius’s stock fell 27% last year as the valuations of the leases that it owns are highly influenced by interest rates, with higher rates resulting in lower valuations. Additionally, given these lower valuations, for its investing arm to keep creating value net of its ongoing costs, it will need to buy new assets at lower valuations than it has traditionally bought them. The company will need to prove it can achieve this next year.

I bought a few other growth stocks in smaller size last year and early this year – Match Group (MTCH), Microsoft (MSFT), and Facebook (META). I recognized my mistake early on in Match and Microsoft and sold both for minimal losses. We unfortunately still own Facebook, which has been a clear mistake with the stock down 65%. The initial valuation was reasonable, but the company’s earnings have fallen precipitously as competition has hindered revenue growth and the company has been slow to address costs. The position is now very small but given the abysmal performance it deserves a mention.

Outlook

I wrote an investor update at the end of Q2 2022 that went over the current environment and our positioning in detail. The whole discussion still applies, and it’s a message worth repeating, so I’m going to reprint it here:

Economic Environment

I don’t usually write about macroeconomics in my letters because the macroeconomic environment is impossible to predict, so there’s not much use talking about it. I repeatedly stress that my goal is to structure our investments so that we will survive through any type of weak macroeconomic period, even if I can’t predict when we’ll get one.

All these things are still true, but right now we are already in a weak macroeconomic period, which I think necessitates a discussion of how that changes my investment process and what might happen if things bet better or worse from here.

The current economic environment, frankly, does not look good. We have had high levels of inflation this year, which usually means that the economy needs higher interest rates to force inflation down to lower, more sustainable levels. Higher interest rates, in turn, almost universally reduce the value of cash flowing assets like stocks, bonds, and real estate. Interest rates have already risen sharply this year in reaction to the high inflation numbers, causing stocks to go down 20% year-to-date, and US bonds are even down 10%. (note written at the end of the year – stocks finished the year down 19% and US bonds finished down 13%)

It is the central bank’s job to try to reduce inflation by slowing down the economy while not slowing things too much and putting us into a recession. There are, broadly, the three different paths that the economy could take over the next few years:

- Fed hikes interest rates too quickly, slows the economy too much, and we enter a recession quickly

- Fed hikes just enough, the economy gets a “soft landing” with low inflation and no recession

- Fed doesn’t hike enough over the next 1-2 years, inflation stays elevated, and the fed is forced to hike interest rates significantly at a later date, likely causing a very deep recession

If we get scenario 2, then everything is great and stocks probably do quite well from here. Even option 1 would not be so bad. Stocks could have more downside if we enter a recession, but it isn’t likely to be too deep, and stocks are already down significantly from their highs.

Scenario 3 is certainly the worst as it would lead to much higher interest rates and almost certainly an eventual deep recession. Because of this, if we continue to see high inflation, the market will expect even higher interest rates and stocks are likely to keep falling.

How Are We Positioned?

We have always been positioned to survive an inflationary period. That being said, we are long-term investors, not traders. I have set up your portfolios to survive a period of higher inflation and lower stock prices by holding some excess cash, trying to avoid the companies that will be hurt most by inflation, and owning some companies in sectors that should benefit somewhat.

Importantly, as economic variables are almost impossible to predict, I will not be speculating with your money to try to profit based on where I think the economy will go. I will not be selling all of your stocks because I think the economic environment looks weak. I will not be betting against stocks or buying risky options that would pay off if inflation stays high but that would lose money if inflation comes down. My goal is not to predict specific economic environments and make money by speculating on the outcomes but to make sure that our portfolio will survive any tough periods so that we can earn good returns over the long-term.

This discussion of survival is not idle talk. There are plenty of funds that are already down 50% or more this year and many more that will be down much more than that if we get sustained inflation. I consider it my top priority to make sure that we don’t suffer huge losses well in excess of those sustained by the stock market as a whole. It can be difficult or impossible to recover from these types of losses.

We will continue to own good businesses that will survive a tough environment. If inflation continues to go higher and markets go lower, our stocks will almost certainly go down and we will likely lose more money, at least in the short-term. Over time, however, the strength of the businesses we own should deliver strong results. And we have more cash to buy stocks if prices do continue to go lower.

Conclusion

2022 has been a difficult year. Stocks have seen large losses due to higher interest rates and elevated inflation. The environment is still risky, and the path of inflation will likely decide where asset prices go over the course of 2023.

I compounded the losses by making mistakes and buying too many growth stocks late last year and early this year. I believe that over the long-term, those investments will generally work out, but buying stocks only to see them go down 40-50% is a mistake even if prices do recover.

Even with those mistakes, we currently own a portfolio of strong businesses. As a group, the stocks have fallen enough that at this point I think they look very attractive. Many of them have fallen because of short-term worries while the long-term fundamentals are still intact. If they can execute over the next 3-5 years like I think they can, then our returns from here should be quite strong.

My goal is to protect and grow your capital over the long-term. I am not rushing to try to make your money back as quick as possible. I am doing what I always do – trying to find simple, profitable investments and structuring them to limit our true long-term risk. With better execution on my part in the future, we should be well on our way to a second decade of profitable investing.

Technical Appendix

In this section I’ll go over the business results at our larger investments. I’ll share some thoughts on past performance of these businesses, valuations, and future expectations.

Constellation Software

Constellation had a good year, with typical organic growth and a large increase in acquisition spend, although that increase was mostly due to one very large deal.

Constellation mostly buys smaller companies, with most below $10mm in purchase price and the vast majority below $100mm. Last year they bought Allscripts, a healthcare focused software company, for $670mm and have put ~$400mm of equity into the deal. It’s still early, but as of last quarter annualized EBITA was $144mm, which gives them a ~25% levered FCF yield. I’ve always hoped that Constellation could eventually start to do bigger deals at good returns, and if this deal continues to track well, it would be a positive indicator that they can do many more of these deals over time. If they can close more large deals, that would be additive to my valuation of the company. For now, I’m cautiously optimistic and I hope to see more big deals in the future as a further proof of concept.

Last year I wrote that at 34x run-rate FCF, Constellation was at the expensive end of its historical range, although given what I expected on M&A, margins, and growth, that we should still get decent returns (say 10%+) over time. After a good year of earnings growth and a 16% loss on the stock, the valuation has reset to 27x and is much more reasonable.

Transdigm

2022 was a relatively uneventful year for Transdigm. EBITDA as defined was up 21% to $2.6B due to continued aerospace recovery and higher margins. The company paid out a small dividend and closed one deal for $437mm.

Expectations are for ~$3B in EBITDA next year, although I continue to expect higher numbers once we have a more full aerospace recovery. Based on pro-forma revenue of ~$6.1B coming into COVID (which includes recent acquisitions), along with a new margin profile given cost actions, I’d expect something like $3.5B of EBITDA if 2023 was a more normalized environment with flight activity at 90-100% of its pre-COVID trend. There is some upside to both revenue and EBITDA from these estimates given I didn’t assume any outsized pricing actions.

At $3.5B of normalized EBITDA, that would put shares at 15x EBITDA, at the low end of the company’s normal range. I would say it does deserve that slight discount given lower FCF conversion before EBITDA recovers fully along with a higher interest-rate environment.

Berkshire Hathaway

Berkshire had a decent year, without much truly of note. The equity portfolio lost money while the operating businesses performed well. Berkshire’s stock performed relatively well as it checked most of the boxes of factors that have outperformed this year – value, profitability, strong balance sheet, and good capital allocation.

Amazon

Amazon was our biggest loser for the year, and while it is perhaps no surprise that the stock is down given decelerating growth at AWS and reported losses in its retail segment, I believe that there is significant value here with the company valued at roughly $900B.

AWS had a good year, although its growth has started to markedly decelerate in the back half. It grew 32% YTD but exited Q3 at probably 25%, and the market expects further deceleration to perhaps high-teens for 2023. This deceleration has spooked investors, as Amazon shares have been under pressure since it released Q3 results and AWS’s deceleration.

For long-term investors, we really care about AWS’s ultimate size and margin profile. Growth should decelerate over time as the company gets larger and it gets closer to fully penetrating its end market. When thinking about this slowdown, we want to know if it is a structural slowdown or a cyclical one. Although you can never know for sure, the majority of the evidence points to a cyclical issue as growth rates for most cloud-based software providers have dropped in the back half of 2022 given the softening economy and businesses retrenching spend. AWS, additionally, is proactively working with customers to try to rationalize their cloud spend to save costs, which should lessen their growth in the current period although should also lead to better long-term outcomes.

Putting some numbers on AWS, if we assume high-teens revenue growth over the next 3 years, flat margins, a 20x FCF exit multiple, and discount that at 12% then AWS would be worth ~$600B. I believe that each one of those assumptions is conservative and AWS is likely worth ~$700-800B.

Amazon’s retail business is more complicated and difficult to analyze, as the company includes the financials of some of its money-losing growth projects in this segment. Even so, I believe it’s possible to put a reasonable range on retail’s value.

The number I care most about is retail gross merchandise value, which measures the dollar value of goods that is sold through Amazon’s website. While we don’t know GMV for certain, it is possible to estimate it. GMV grew from ~$325B in 2019 to ~$635B in 2021 and probably ~$675B in 2022. The company saw an unprecedented amount of growth from the COVID pandemic. As mentioned previously, Amazon made huge investments to increase capacity during the pandemic, and while sales have roughly doubled over a short amount of time, Amazon was prepared for even more growth, and so it currently has excess capacity and cost.

I believe that preparing for even more demand was in the best interest of its business long-term, as underestimating demand would hurt the trust that consumers have grown to put in it for fast, reliable delivery, and overestimating demand simply ends up with some excess costs for a relatively short period.

As it stands today, Amazon does have this excess cost in its cost structure, and so retail’s profitability has been lower than normal. This should be a relatively easy fix as they take steps to reduce capacity and further grow into the capacity that remains.

In a normalized environment, I believe Amazon retail’s earnings power is very high, likely with operating margins at perhaps 6-8% of GMV if they were running it to maximize current profitability. Even using 5% would give you a range of its value of ~$400-600B.

Putting it together, with conservative marks AWS is worth roughly $700-800B and retail is worth $400-600B, compared to a market value of $900B. Both businesses have deep, entrenched moats and given switching costs in AWS and terrific logistics and variety leading to convenience in retail, these businesses should be very durable over the long-term.

Google’s core business had a mixed year with decent revenue growth in its core business but with slightly lower margins year-over-year as the company has continued to aggressively hire employees.

If we zoom out to look at the past 4 years, then the lower margins appear less problematic:

Even with slightly lower margins year-over-year, margins are still up over the past few years, and revenue has grown at a strong clip over that time.

While Google has had some other minor positives this year – the cloud business growing 38% YoY with strong incremental margins and the company using all of its substantial FCF for share repurchases – the main driver of the stock has been the market’s worry over revenue and costs in its core business next year.

With the economy slowing, many are expecting Google’s revenue to fall next year. Furthermore, management has indicated that it will continue to invest in incremental headcount even in a weak revenue environment. If revenue falls while costs increase, earnings could contract materially.

A drop in earnings next year is certainly a risk to the stock short-term, but I care more about the long-term outlook. Margins could certainly be down in any one year, but Google has proven that it can easily operate at mid 30s operating margins in its core business, and I would expect its business to return there over time. I would also expect some revenue growth over the next few years, even if it’s much lower than it has been in previous years.

Shares currently trade at 13x trailing core earnings + net cash + 4x cloud sales, so if we get some revenue growth over the next few years along with reasonably good margins, the returns should be good from here.

First Republic Bank

As noted above, First Republic has continued to grow assets, loans, deposits, and earnings at a good rate, but interest rate dynamics are very likely to hurt its earnings next year.

Here’s a look at its important metrics over the last 3 years:

Per-share growth metrics have been very strong across the board, and credit quality continues to be pristine.

As noted previously, the issue is that First Republic is writing new loans at relatively low spreads to treasury bond rates, and given its customers tend to have large deposit balances, it’s being forced to pay quickly increasing rates on its deposits. That dynamic will likely lead to much lower net interest margin and earnings next year.

First Republic could lessen the pain to its earnings next year if it decided to rein in growth somewhat, as it is the marginal deposits that they’re attracting at very high rates via CDs. But the culture of the bank is to pursue good customers and profitable growth, even if it hurts short-term results. This strategy has worked well for the company in the past and I believe that it’s still the right strategy for this environment, as even with lower earnings they can still finance this growth accretively.

Radius Global Infrastructure

Radius has performed about as I would have expected since we’ve owned it – rent growth has increased from around 2% initially to 4.3% last quarter as the company is benefiting from its predominantly inflation-linked escalators. Radius has also deployed almost $700mm (including all corporate SG&A costs) into acquisitions at a fully burdened going-in cap rate of 5.6%.

When I initially bought shares and interest rates were very low, I estimated fair value for Radius’s assets was probably somewhere around a cap rate of 4% given low churn, inflation-linked escalators, and their triple net cost structure. With rates higher now, I’d say fair value would be lower, maybe around a cap rate of 5%. With 2-3% rent growth and 50% LTV debt at a cost of 6%, that would generate 8-10% IRRs at a constant multiple.

I initially bought shares at a going-in cap rate of ~5% during a period of lower rates. I earlier said I overpaid for Radius, even though we bought shares at what I still believe was a discount to fair value at that time. I say this for two reasons. The first is because increases in interest rates would quickly lower my fair value estimates, and I would expect higher rates at some point so shouldn’t have anchored to the low prevailing rates at the time. The second is that Radius is exactly the kind of stock that will be volatile – it’s small, has significant hedge fund ownership, has leverage, and requires funding for its growth program. With these stocks, you can almost always afford to be patient and purchase shares at discounted valuations. If I had exercised some patience, we would have been able to buy a lot of stock at a large, obvious discount to the value of the real estate this year when the stock price was low.

As I write this, Radius trades at a cap rate of ~5.6%. If we just owned the portfolio of assets and cash flowed them, the results would be very likely to be good over time. We do, however, need to include the impact of the asset-purchasing platform.

The full SG&A burden for the company runs at $50mm / year. Radius has been buying $400-500mm of real estate per year at going-in cap rates in the mid 6%’s, excluding this $50mm of SG&A spend. When fair values were around 4%, the accretion math was clear – $400mm spent at cap rates of 6.5% yields $26mm in rent, which is worth $650mm at a cap rate of 4%, so the $250mm in value creation dwarfs the $50mm of SG&A expense.

However, with fair values now at cap rates of roughly 5%, the math gets a little tighter. I am hoping to see going-in cap rates on acquisitions going up along with higher rates, but last quarter cap rates went down to 5.8%. If you run the same math with $400mm spent at 5.8% with fair value at 5%, then the value creation net of SG&A rounds to $0.

When I initially bought Radius, I had such a scenario where they don’t create any incremental value with acquisitions in mind. The whole reason for Radius to be public is for it to be able to finance growth accretively. If it is unable to do so, it is very likely that they will sell the company to a private buyer. Rumors of a sale have already started, but we’ll have to wait and see if anything comes of them.

The scenario where we would lose is if Radius is buying assets at barely any spread to fair value, the corporate level SG&A is higher than this meager value creation, and the company remains public so that the asset-purchasing platform bleeds money out of the returns from the underlying real estate. Although this could happen, I believe shareholders would force the company’s hand into a sale in this scenario, which should give us upside from today’s levels.

Charter

There is not much to add to what I said about Charter above. The company trades at a very low multiple of normalized levered FCF, so if it can manage to grow EBITDA a little bit over time then the returns to the equity will be very strong. If competition leads to customer losses and/or lower pricing, and that leads to lower EBITDA, then Charter will be forced to use much of its free cash flow to reduce debt and returns to the equity will not be good.

There are plenty of reasons for confidence – ARPU lower than peers, a strategy based on customer growth and high penetration, incremental contributions from its mobile business, and relatively low-cost speed upgrades – but the effects of incremental competition can be unpredictable.

The best way to sum up Charter is that in my eyes, the expected value as a probability weighted distribution of its value in these expected scenarios is quite a bit higher than its current price, but it is a high variance situation. At current share price levels in the low $300’s, I have some comfort that even in a case where Charter loses internet subscribers or is forced to lower pricing and EBITDA contracts, I would get a value for the company somewhere around where it currently trades. It is always dangerous to be too precise with these calculations, but this is some evidence that the upside case would lead to very high returns and some of the downside cases would lead to okay results.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment