scotspencer/E+ via Getty Images

Intro

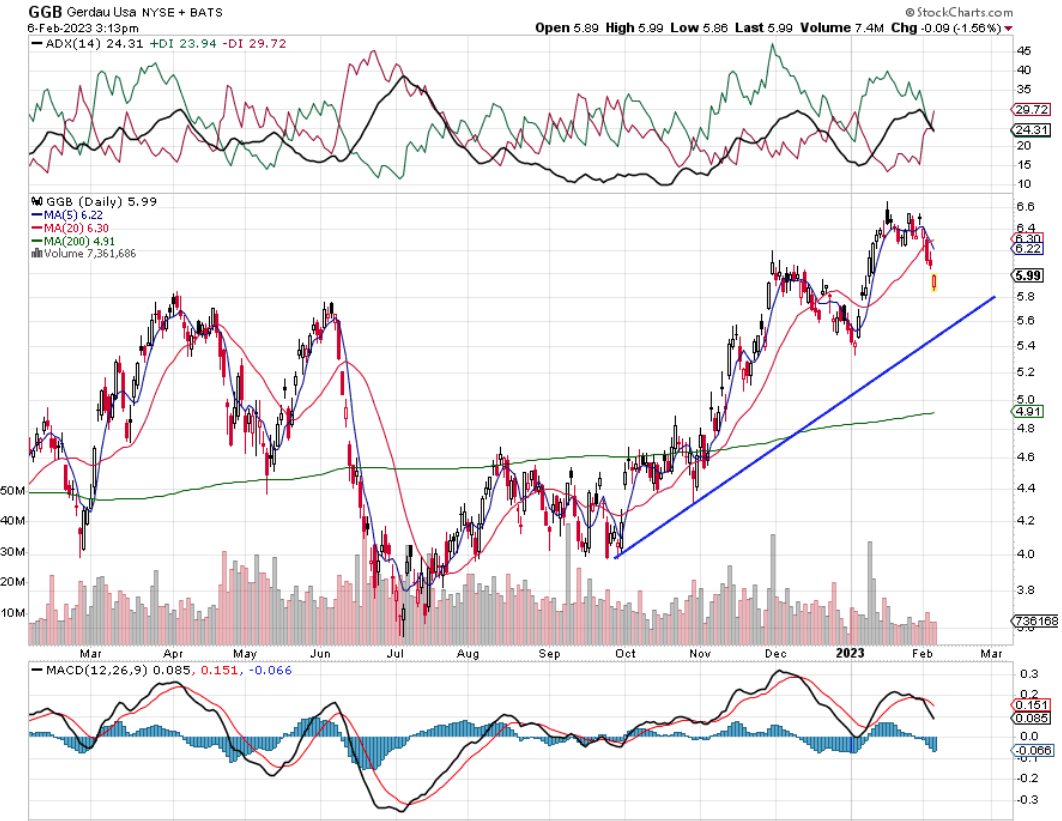

If we pull up a chart of Gerdau S.A. (NYSE:GGB), we can see that the steelmaking company looks to have topped out at least temporarily. However, the stock’s rising 200-day moving average as well as its recent pattern of higher lows and higher highs leads us to believe that downside risk is limited here. In fact, when one studies the numbers and recent earnings reports, the sustained pattern of higher lows and higher highs that we have basically seen since early 2020 are aligned with how the company’s fundamentals have been improving. The financial performance of the first three quarters of this fiscal year was the best in Gerdau’s history and if cash-flow trends (Which we will get into) are anything to go by, we expect to see gains continuing for some time.

Furthermore, despite Gerdau’s very strong start to 2023, shares continue to trade on the cheap. The company’s trailing price-to-sales ratio comes in at 0.64 and price to book ratio comes in at 1.11. Suffice it to say, given Gerdau’s valuation and the money it is making at present, we recommend that investors do not become overly concerned with Gerdau’s forward-looking expected growth rates.

Gerdau Technical Chart (Stockcharts.com)

Solid Cash Flow Generation

If we just take the recent third quarter and how cash flowed through the company, we see that Gerdau generated over $600 million of operating cash flow of which close to $200 million was used for capex purposes. The three main priorities from a capital expenditure standpoint are competitive raw materials procurement, tailoring production to customer demand, and being able to offer an increasing amount of value-adding products to the mix over time.

However, what about the remaining $400 million approx. of free cash flow which was generated in Q3? This cash (after capex was spent which is essentially funds to maintain or upgrade the business) continues to be used to improve Gerdau’s position for the better. Approximately, $222 million was paid to investors in the form of dividends in Q3, $112 million of stock was repurchased and close to $25 million was put toward the company’s debt load. All three of these actions benefit shareholders as Gerdau’s forward dividend yield now comes close to 11%, EPS continues to rise due to a lower share count and Gerdau’s liabilities continue to come down.

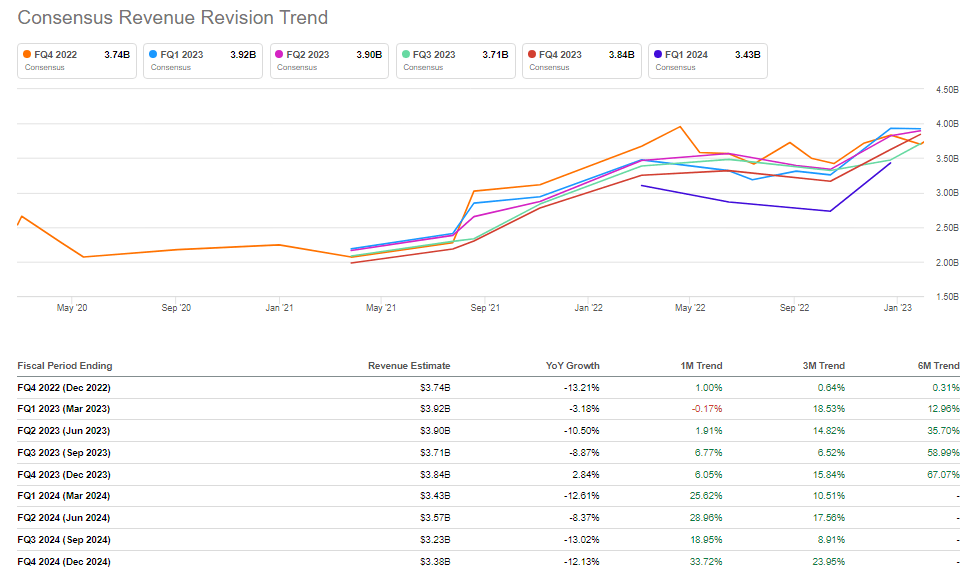

Suffice it to say, the lower the stock’s valuation and the healthier the company’s debt profile, the less downside risk will be inherent in this play when the eventual downswing occurs. In saying this, the forward-looking revenue estimates for example as we see below remain encouraging despite the negative rolling quarter top-line growth which is expected in Q4 and beyond in fiscal 2023.

Gerdau Consensus EPS Estimates (Seeking Alpha)

Strategy

So here is how we see a potential investment in Gerdau at this moment in time. Being a low-priced stock (Approximately $6), investors have the opportunity to buy an asset that is currently paying out a double-digit dividend yield. Furthermore, despite the fact that the stock’s implied volatility is well below average in GGB at present (39.5%), this stock is optionable which means investors can also bring down their cost basis through repeated covered call writing. At the end of the day, GGB offers income-orientated investors the opportunity to buy an income-generating asset at a very attractive valuation.

Suffice it to say, given the cyclical nature of the steel industry, reinvesting that dividend as well as potentially writing covered calls against long positions makes sense in order to keep on reducing that cost basis (Which lowers risk) in an environment where earnings are expected to contract next year. The dividend remains well covered (42% Payout Ratio) and no technical damage has yet to be inflicted on the technical chart.

Conclusion

Therefore, to sum up, due to the cyclical nature of the steel industry, we view Gerdau as more of an income play at this stage. Although shares continue to make higher lows and higher highs on the technical chart, the market remains well-clued into future demand and how earnings will be affected as a result. However, aggressive income-orientated investors can use the dividend as well as covered call writing strategies to bring down the cost basis in a significant manner. Let’s see what Q4 brings. We look forward to continued coverage.

Be the first to comment