InfinitumProdux

Thesis

Genco Shipping & Trading Limited (NYSE:NYSE:GNK) stock has been battered over the past three months as it fell nearly 50% from its June 2022 highs to its recent September lows. Despite distributing robust dividends, GNK’s YTD total return fell into the negative zone, at -1.33% (as of September 13’s close).

Hence, it has been a remarkable fall from grace from the surge in optimism on GNK in early 2022, as the global supply chain snafu unwound dramatically. Moreover, China’s recovery from its worst COVID lockdown in Q2 and worsening recessionary concerns have intensified the near-term headwinds on leading dry bulk shipping companies.

However, we deduce that the “massacre” seems to have reached highly pessimistic levels. Also, we gleaned that GNK has likely bottomed out, given its spectacular collapse from June highs. The price action on iron ore also suggests that it could be bottoming out on a long-term basis.

Management’s commentary from its Q2 earnings also corroborates our conviction that Genco’s growth cadence should improve through FY23. However, we believe that Genco needs to go through this significant digestion to de-risk its valuation, as it laps highly challenging comps from FY21, coupled with the heightened recessionary risks exacerbated by a hawkish Fed and a worse-than-expected CPI print for August.

But, we think the destruction in GNK looks near to completion. Therefore, we postulate it’s appropriate for investors to consider adding exposure at the current levels, capitalizing on the highly pessimistic sentiments.

We rate GNK as a Buy.

GNK’s TCE Growth Has Normalized Dramatically

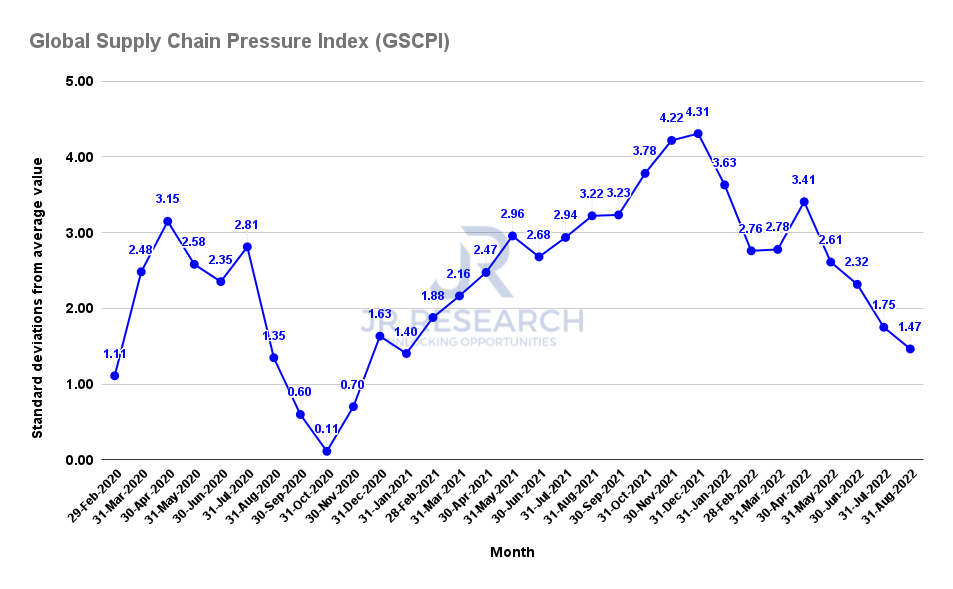

Global Supply Chain Pressure Index (Federal Reserve Bank of New York)

As seen above, the New York Fed’s GSCPI has continued to fall steeply through August as the pressure on the global supply chain and port congestion continued to ease further.

Notably, it has already moderated to levels last seen at the start of 2021, as the supply chain snafu normalized. It has also coincided with raised recessionary fears, triggered by an increasingly hawkish Fed. Given yesterday’s higher-than-expected CPI print, the market expects the Fed to delay tapering its hawkish stance. The market is also pricing in a 36% probability (as of September 13) of a 100 bps hike, which stoked fear in the broad market decline on September 13.

Despite that, GNK held its September lows robustly (which we will discuss in the price action segment), which corroborates our conviction that the market has de-risked its valuations substantially.

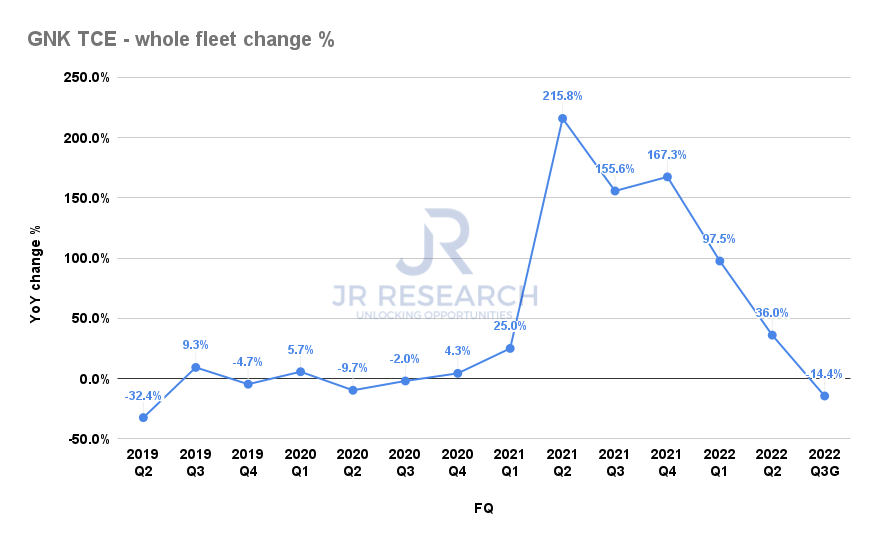

Genco TCE – whole fleet change % (Company filings)

In addition, the growth in Genco’s whole fleet time charter equivalent (TCE) rates has also fallen markedly through Q2, as it posted its second consecutive quarter of sharply lower growth metrics (up 36% YoY).

Notably, Genco’s Q3 TCE guidance indicates that its TCE growth could fall into the negative territory (down 14.4% YoY) as it laps highly challenging FY21 comps amid near-term macro headwinds. Hence, we believe the battering by the market from its June highs is justified, as it correctly anticipated the near-term challenges facing Genco and its dry bulk peers.

Despite that, the company remains highly confident in its medium- to long-term outlook. Its low newbuilding order book, coupled with record low industry-wide metrics, suggest that Genco and its dry bulk peers should weather the near-term demand and pricing dislocation well as the economy improves.

Moreover, coupled with stricter environmental regulation, we believe it bodes well on the demand/supply dynamics that should underpin a robust and stable TCE outlook moving forward.

Genco Is Well-Positioned To Ride These Headwinds

While still hampered by its property market malaise and weak consumer spending, we believe it’s reasonable to expect an improvement in China’s economy over 2023/24.

The Chinese government has been proactive in implementing its infrastructure stimulus to boost spending. Bloomberg reported that several local governments have followed up with implementation policies in line with the central government’s guidance.

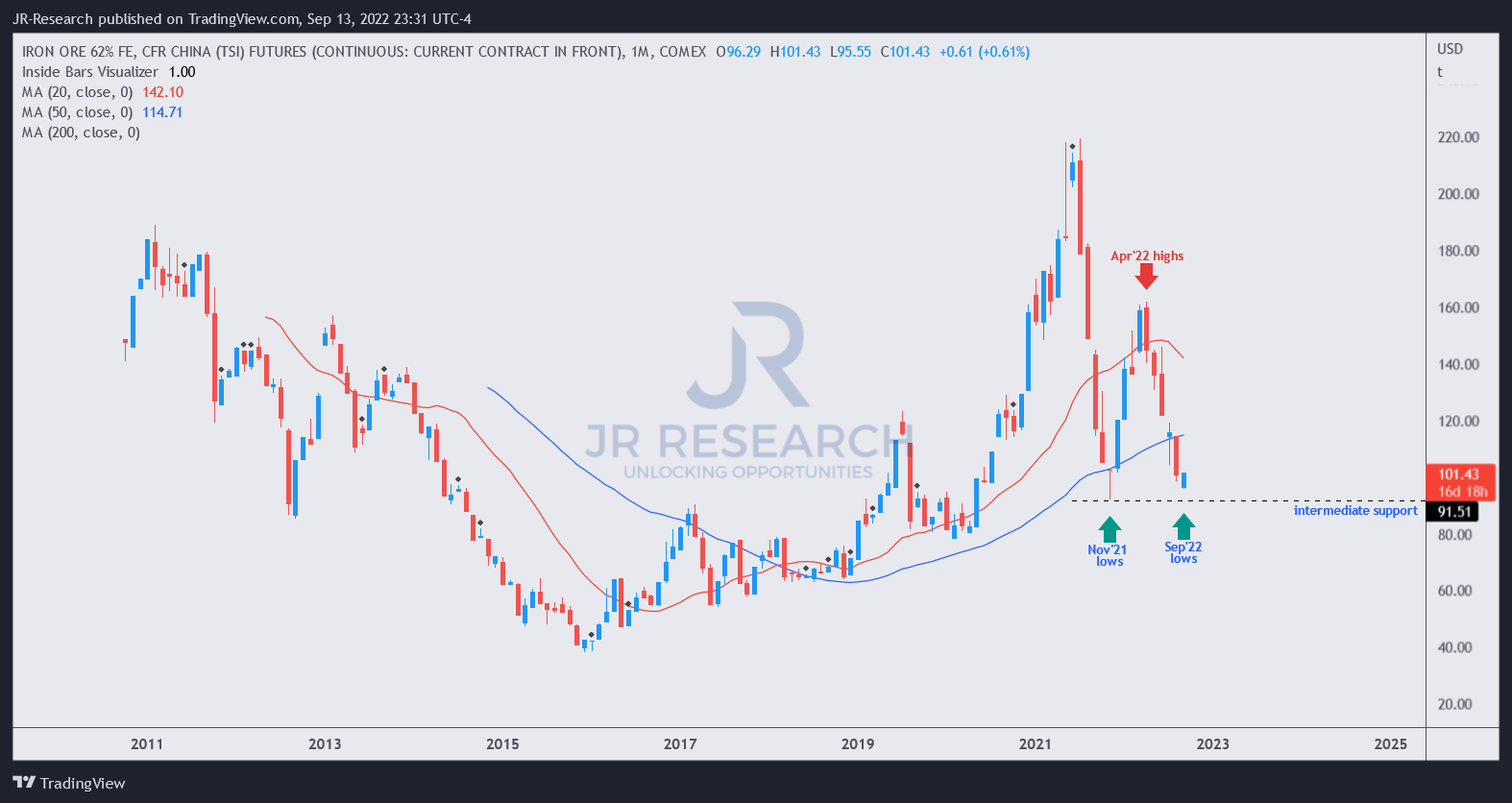

Iron ore futures price chart (monthly) (TradingView)

Furthermore, we posit that iron ore futures appear to be bottoming out on its long-term chart. As a result, it should remove a critical impediment to the commodity exporters. It’s also in line with Genco’s commentary, as it highlighted optimism from its iron ore customers for H2’22 and beyond. Therefore, we believe the headwinds seen in H1’22 should stabilize moving ahead, helping GNK to find robust support at the current levels.

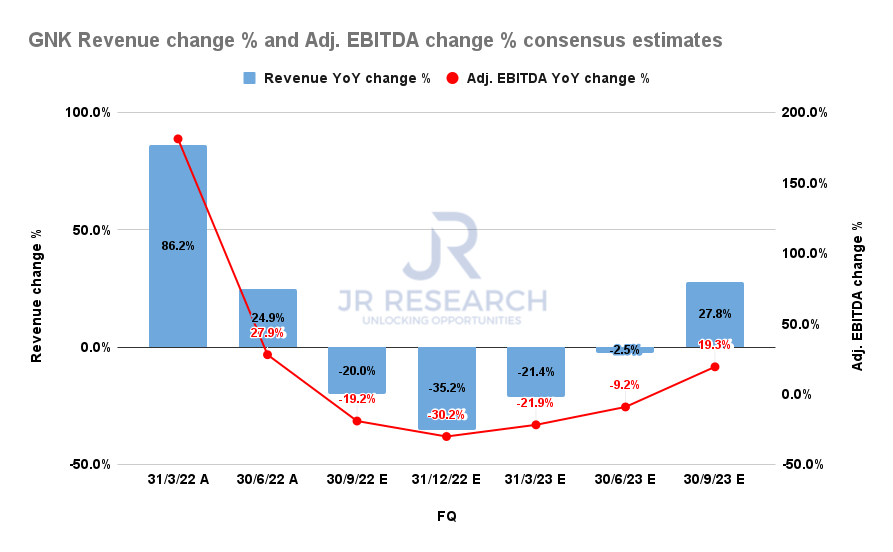

Genco revenue change % and adjusted EBITDA change % consensus estimates (S&P Cap IQ)

Therefore, we are confident that the consensus estimates (bullish) are credible, as it projects Genco’s revenue and adjusted EBITDA growth to reach a nadir in Q4’22 before recovering through FY23.

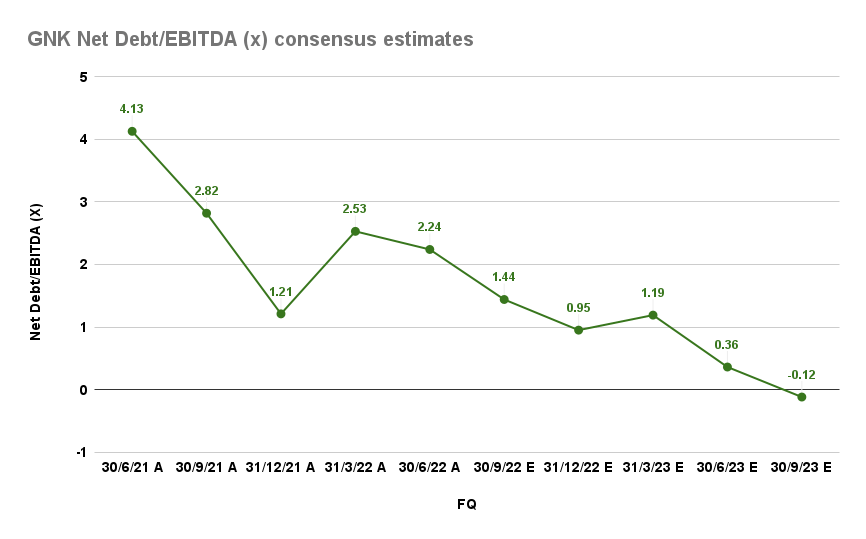

Genco Net debt/EBITDA ratio consensus estimates (S&P Cap IQ)

Moreover, Genco has been highly disciplined with its capital allocation priorities, as it continued to pay down debt with its robust earnings. Management expects to reach a neutral net debt position by the end of FY23, in line with the Street’s estimates.

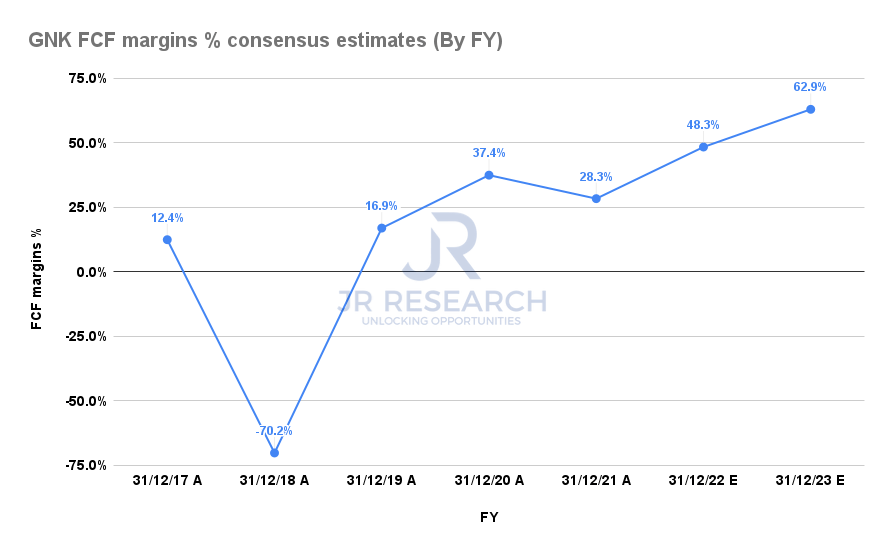

Genco FCF margins % consensus estimates (S&P Cap IQ)

As seen above, Genco’s free cash flow (FCF) margins are also estimated to continue improving as it pays down debt over time. Therefore, we believe it should underpin its valuation robustly as investors become more confident in the company’s financial strategy.

Moreover, management is confident that the robust improvement in its financial position should continue to drive the sustainability of its dividend strategy and help re-rate GNK in the medium term.

Is GNK Stock A Buy, Sell, Or Hold?

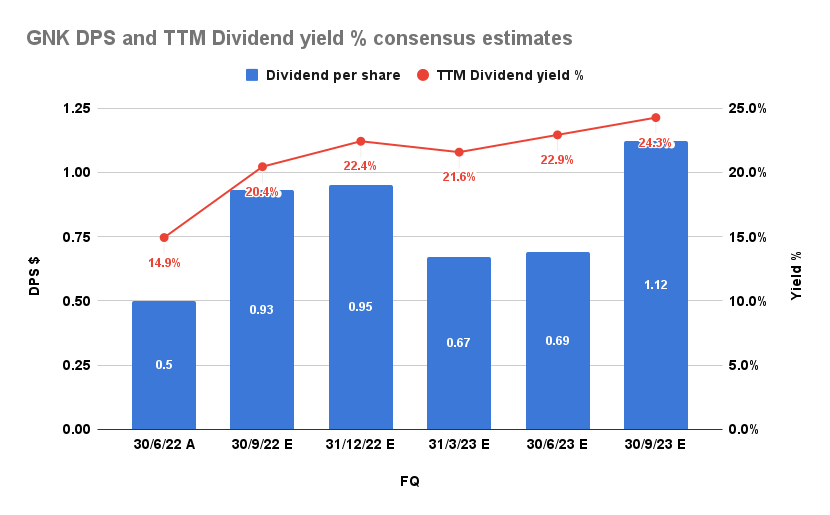

Genco DPS and TTM Dividend yield % consensus estimates (S&P Cap IQ)

Management is confident that Q3’s dividend payout will be higher than Q2’s payout. The consensus estimates project that Genco’s Q3 dividend could amount to $0.93 per share, equivalent to a TTM dividend yield of 20.4%.

Importantly, the company’s improved cash flow fundamentals should see GNK maintaining its robust dividend yields through FY23, helping undergird its valuation.

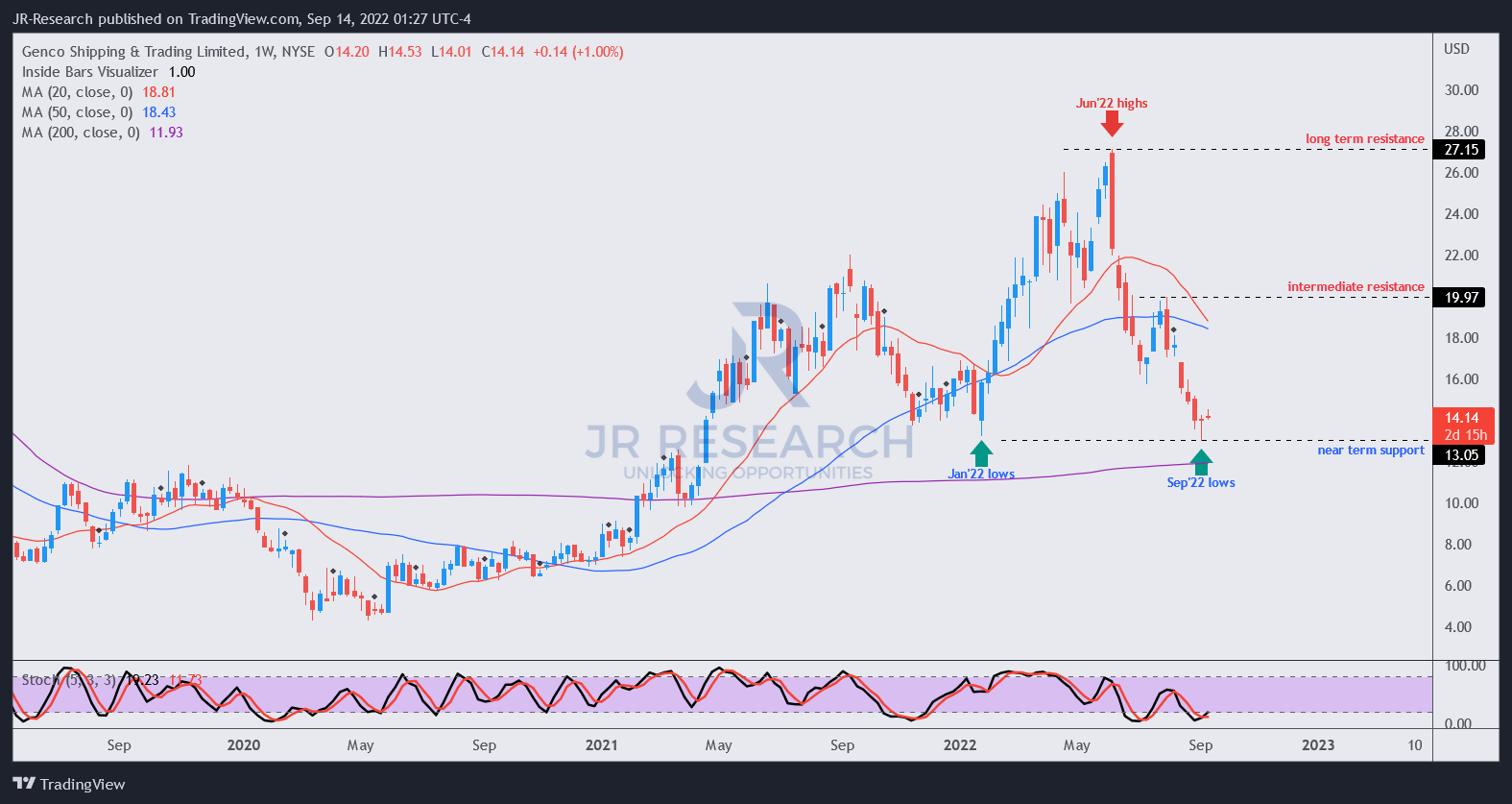

GNK price chart (weekly) (TradingView)

Furthermore, we gleaned constructive price action on GNK’s medium-term chart, suggesting that it has likely bottomed out.

As seen above, GNK’s recent lows last week coincided with the robust support level formed by its Jan 2022 lows. While the de-rating from its Jun 2022 highs is justified to de-risk its near-term headwinds, we believe the sentiments have turned overly pessimistic. Furthermore, the CPI headwinds yesterday have not impacted its recovery cadence.

Therefore, we believe investors should capitalize on the fantastic opportunity to add exposure. Accordingly, we rate GNK as a Buy.

Be the first to comment