ShyLama Productions

While most oil stocks have rebounded in the last month as oil prices increased, Canadian companies with high share of heavy oil into their production mix have struggled. One of those is Gear Energy (TSX:GXE:CA)(OTCQX:GENGF), which I covered before. Since then, the shares have fallen, yet the 2023 outlook looks promising. At the current share price, Gear Energy’s gross dividend yield is more than 11% and looks sustainable at WTI prices above US$80/barrel. Shrinking of the discount of Western Canada Select (WCS) to WTI oil could be a major catalyst for the stock. The difference may narrow in 2023, especially towards the end of the year when the completion of the Trans Mountain Pipeline is expected.

Recent performance

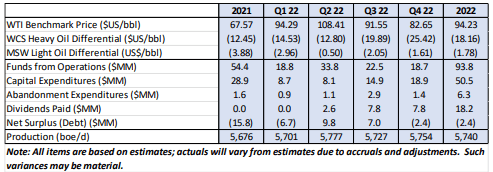

In its December update, Gear Energy provided the picture at the end of 2022. Production in Q4’22 was 5,754boe/day, which was pretty much flat compared to the previous quarters of 2022. While the Q4’22 official statement is not out yet, clearly the company got hit pretty hard by a widening of the WCS heavy oil discount to WTI to over US$25/barrel.

2022 highlights (Gear Energy)

The cash flow hit by this was partially offset by lower capital expenditures, which came at CAD$50.5M – a lot lower than the CAD$64M as previously indicated. At the same time, monthly dividend payments of CAD$0.01/share continued, which resulted in approximately CAD$7.8M of cash outflow. As a result, Gear Energy ended the year at a very small net debt position of CAD$2.4M. Note, that as of Q3’22 the company had tax pools of CAD$623.8M, which indicates at least few years without cash outflow related to taxes.

2023 guidance

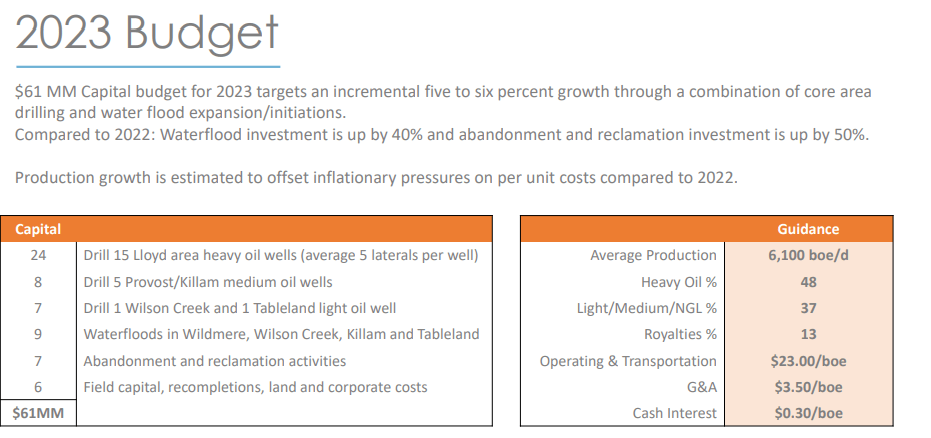

In the latest corporate presentation, management provided its 2023 budget and guidance. Production is expected to increase around 6% YoY to 6.1kboe/day with heavy oil having the biggest share of almost half of the amount. OPEX and transportation costs are expected to come at CAD$23.00/barrel. I find this a little ambitious, given that in Q3’22 those costs were CAD$24.83/barrel, so a little bump in the actual number won’t be surprising. CAPEX for the year is projected at CAD$61M, which would be 20% increase on the actual one from 2022.

2023 budget and guidance (Gear Energy)

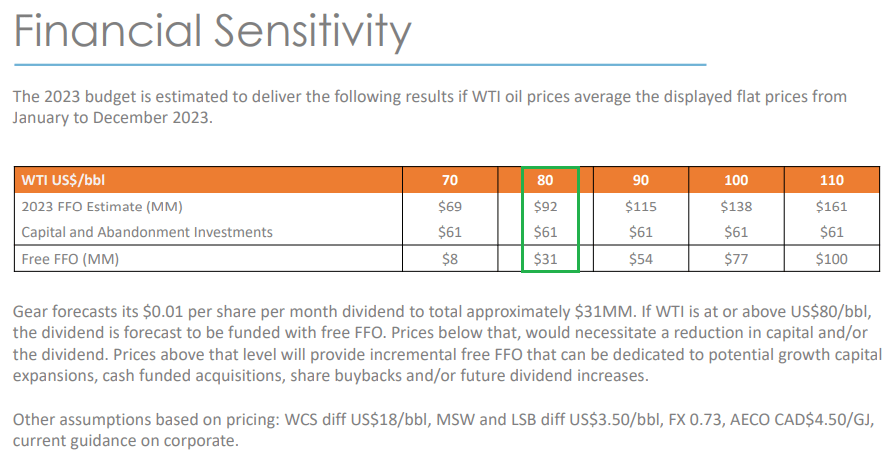

In turn, given the expense and production guidance, management has provided a sensitivity analysis of the cash flow situation under different WTI prices. Given that the continuation of the monthly dividend payments will result in a CAD$31M cash outflow for the whole year, the price of WTI should be at least US$80/barrel in order for the distributions to be entirely covered by cash flow generation.

Cash flow sensitivity to WTI prices (Gear Energy)

An important assumption of the cash flow guidance is a WTI-WCS price differential of US$18 on average for the year. Given that the figure in Q4’22 was more than US$25, this may be a challenge. So in order for that to be offset, WTI prices should be more in the US$84/barrel range to meet the cash flow guidance. Of course, given the solid financial position of the company, a small amount of the dividend distribution could be met by debt (only a short-term solution) or a small decrease of CAPEX.

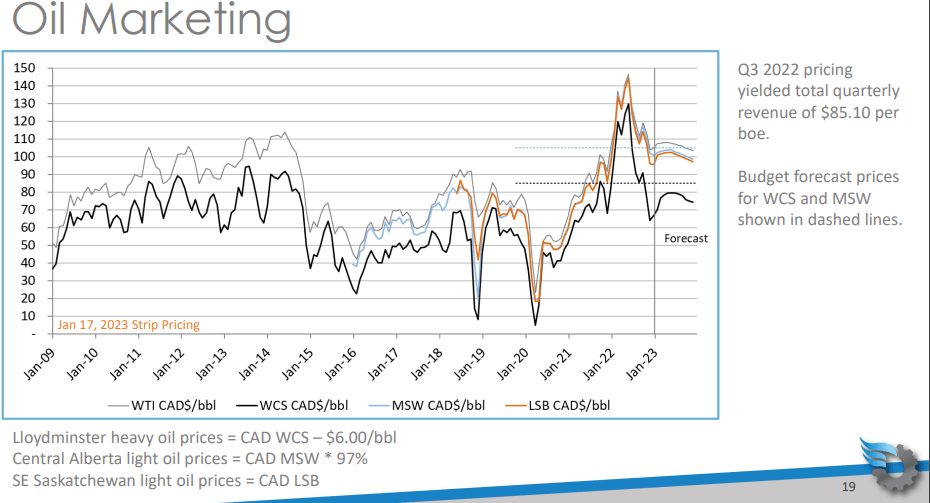

The WTI-WCS price differential

The large discount of Canadian heavy oil to WTI is a serious burden for Canadian oil producers, that have large share of heavy oil in their production mixes. Gear Energy is not an exception to this. While the widening of the spread could be partially attributed to the unprecedented release of over 180M barrels from the US SPR, therefore reducing refinery demand for Canadian oil, the spread remains wide even after the SPR drawdown finished.

WCS-WTI price differential (Gear Energy)

The key to the high spread is not enough pipeline capacity from Canada to the US. Low levels of the Mississippi River, used as an alternative transport route, exacerbated the issue of the limited pipeline capacity. The issue of the pipeline capacity and its potential solution was laid out perfectly by Michael Fitzsimmons in his recent article “The Trans Mountain Pipeline Expansion Will Benefit Cenovus”. The mentioned Trans Mountain Pipeline is expected to be completed towards the end of 2023 and be fully operational in early 2024, which could be a serious factor in WCS-WTI spread normalization.

Valuation discussion

Despite the high WCS-WTI spread, at the current WTI price environment of US$80+ per barrel, Gear Energy seems capable of maintaining the monthly dividend of CAD$0.01/share. When comparing the annual expected payout under this policy to the current share price, the dividend yield would be over 11%, which is one of the highest in the energy sector. Recent insider activity indicates, that some insiders were still buying into Q4’22, despite the widening of the WCS spread. Indeed, the Chairman sold a significant block of shares, but this could be for cash needs, not because of doubts in the company’s future. Overall, insider ownership is quite high at 8% (11% fully diluted), which is also a positive sign.

A potential shrinking of the WTI-WCS price differential, which I see as quite possible especially towards the end of 2023, could be a serious catalyst for this stock. Meanwhile, shareholders could be paid a gross annualized yield of 11+% to wait, which seems like a good deal.

Risks

The biggest risk for Gear Energy naturally is a decline in oil prices or further widening of the WCS discount. However, I don’t think a decline in oil prices is likely as explained in this article. When it comes to the WCS-WTI spread, it’s already very wide, so in case of further widening some companies may reduce supply, to meet the logistical constraints and shrink the spread. That won’t be easy though, given that there are many Canadian oil companies, making coordination challenging.

Takeaway

Gear Energy seems like a well-managed company with transparent and shareholder-friendly management. While the WCS-WTI price differential widening is burdensome for the company, the issue should be resolved by the end of 2023. Meanwhile, Gear could be paying monthly dividends yielding 11+% on an annual basis, making it attractive for income oriented investors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment