Chunumunu

Thesis:

GameStop (NYSE:GME) took the investing world for a run with its epic short squeeze in January of 2021. While the market has seen short squeezes occur in the past, GameStop’s was fueled by an internet community looking to stick it to hedge funds. All the more interesting, GameStop’s backers have been relentlessly holding their positions, some with tempting amounts of profit. Regardless, I personally believe GameStop is not poised well for the current market conditions looming and ahead. Rising interest rates, high inflation, and overall economic turmoil likely won’t bode well for this meme stock. I covered GameStop back in May using technical analysis, predicting the stock was headed down. However, GameStop didn’t have the stiff macro headwinds that it’s facing now. This article will cover the additional catalysts weighing on GameStop stock, and why I believe the stock isn’t far from trading at penny stock price levels.

Interest rates, inflation, and a struggling economy:

Interest rates have already hit the broader market quite substantially. The federal funds rate has jumped from a target rate of 0% – 0.25% to 3% – 3.25% in an effort to counter 40-year high inflation levels. As a result, the Dow Jones is down roughly 20% from previous market highs. GameStop hasn’t had a great year by any measure; however, the stock is only down roughly 10% from its candle close this January around the $27 price level.

It’s worth noting the Fed is planning to hike rates upwards of 4.75% by the end of 2022, with plans to reach the 5% early in 2023. The idea is that higher rates will reduce consumer spending, in turn reducing the demand and price of consumer goods (inflation). However, inflation levels are still north of 8%, even as rates continue to rise. The inflation crisis in the current market is more severe than I think a lot of people realize. Covid-fueled stimulus and quantitative easing flooded capital into the markets while the Fed kept rates on the floor as the market was flourishing. This flooded the market with capital and access to very cheap borrowed capital, resulting in massive consumer spending. This spending created high demand and high prices. Furthermore, the market was hit with global supply chain disruptions, exacerbating price hikes. Next thing we know, stimulus checks have been spent and the Fed starts hiking rates rapidly. This is where the economic turmoil comes in, as consumers are struggling on the capital front while the cost of consumer goods have skyrocketed.

This is all terrible for those long on GameStop. To start, GameStop sells consumer goods, which are now highly priced and less frequently bought. This is particularly alarming considering GameStop’s goods would be considered more of a luxury item (gaming and entertainment). The GameStop bulls will tell you sweet tales of GameStop’s emergence in the Non-Fungible Tokens (NFTs) market, however, I wouldn’t be sold too quickly. There are numerous big players in the NFT market, and sources reflect NFT prices have dropped between 70% and 92% since March of this year. If GameStop’s business model wasn’t bad enough for you as is, the company’s saving grace lies in a market where prices are down upwards of 90%. Keep in mind, NFTs are considered to be far more volatile than the likes of the Crypto market’s best projects like Bitcoin and Ethereum. It’s worth noting both Bitcoin and Ethereum are down roughly 72% from all-time highs.

In short, GameStop is operating a dying business model to begin with. That business model gets even worse when factoring in the economic turmoil that is currently plaguing consumers and businesses. The company’s transition to a market that is down 70% across the board really shouldn’t provide much optimism either. Aside from the meme soldiers with an undying ambition to stick it to hedge funds, GameStop is simply dead money.

A quick look at GameStop’s financial instability:

GameStop’s books reflect a dying business after it has been given the financial equivalent of a heart, brain, and lung transplant. The company is still operating at a loss, with its trailing twelve-month (TTM) net income sitting at ($519.50) million. To better emphasize that statement, TTM free cash flow sits at ($876.40) million. GameStop was actually free cash flow positive on a TTM basis for the quarter ending in April of 2021 with $86.10 million. The company’s free cash flow has dropped over 1,000% since its short squeeze. GameStop’s price to book is sitting just north of 5.6, indicating GameStop bulls are willing to pay nearly six times the value of shareholder’s equity for a stock that is exponentially losing more money each quarter. In short, there is simply no indication that GameStop is doing anything successful on a business front. Sure, I understand wanting to stick it to hedge funds; however, how long can this game be played? This stock is providing more risk to the retail investors backing it than any institutional hedge fund abroad.

My prediction for GameStop (technical analysis):

I’m going to provide my technical analysis prediction for GameStop moving forward. I don’t like to use technical analysis for common stocks, however, considering GameStop trades against all fundamentals, I will do so here.

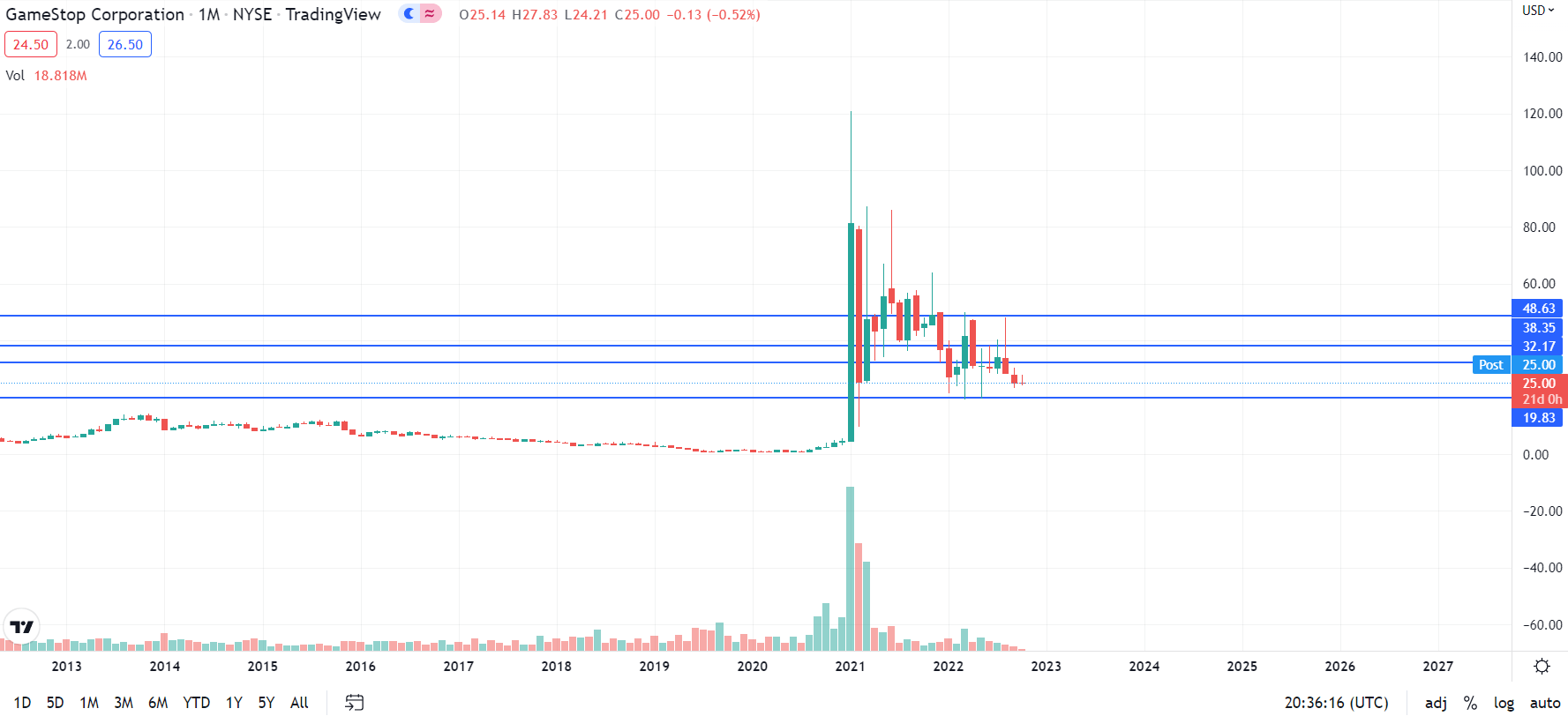

GameStop Support Levels (tradingview.com)

GameStop has formed a massive descending triangle pattern since reaching its all-time high in January of 2021. More importantly, in my opinion, is how GameStop continues break critical levels of support, with the most critical level approaching. Should GameStop break below the $19.83 level, there are only two more levels—$10 and $5—before the stock will be headed to price levels under $1. Considering the current state of the economy and GameStop’s inability to achieve any financial success, I believe the stock is on its last legs.

While many of GameStop bulls want to hold out as long as possible, I do believe the temptation to take potential profits will overpower the will to stick it to hedge funds. Especially, when considering many GameStop bulls may need to sell positions to help their own financial positions amid economic uncertainty. Sadly, I believe many positions in GameStop are at a loss and held with hopes of another short squeeze. Most of success stories heard with GameStop are of traders that SOLD their positions for massive gains. The ideology of ‘diamond hands’ appears to be harming those with either minor gains and/or now losses.

There is far more against GameStop stock than just hedge funds: Economic turmoil, market psychology, and the basic fundamentals of finance. GameStop has been trending one direction (down) since its massive price spike last year, and it doesn’t look like that’s going to change any time soon. In fact, GameStop’s decline began well before it was facing a slew of headwinds with inflation, interest rate hikes, and a struggling economy. All indications point to GameStop being on a fast track to the penny stock label. I believe the economy and broader market will be facing headwinds well into 2023. That said, I believe that GameStop will fall to price levels below $10 in the next year.

Conclusion:

In conclusion, I don’t see the GameStop charade lasting much longer. The investors that succeeded knew the nature of a short squeeze and made massive profits. Many others appear to be living on a prayer. A short squeeze can only go so far, and GameStop’s was substantial. The hope of a $10,000 per share of GameStop was simply unrealistic. Reddit’s meme army did stick it to the hedge funds; many of them were forced to close shorts and realized massive losses. Current short interest is less than 20% of shares outstanding currently. When the squeeze occurred, short interest was over 100% of shares outstanding. GameStop is facing significant headwinds with no optimism in sight. I believe GameStop is headed towards price levels below $5 per share (penny stock price range) and rate it a sell.

Be the first to comment