ASKA/E+ via Getty Images

Newsflash: the Bank of Japan did not intend to tighten monetary policy last week. The BoJ did not even intend to signal tightening. While the BoJ made its ongoing, accommodative stance, plain and clear in several ways in its statement on monetary policy, financial markets got distracted by the widening of the interest rate band. In an economic speech on Monday titled “Toward Achieving the Price Stability Target in a Sustainable and Stable Manner, Accompanied by Wage Increases“, Governor Kuroda Haruhiko uttered a one-sentence follow-up to clarify the BoJ’s actions last week. Haruhiko plainly said, “these measures have been implemented to conduct monetary easing in a sustainable and smooth manner while taking into account the transmission of monetary easing effects, including to corporate financing; this is definitely not a step toward an exit” (emphasis mine).

This declaration followed specific details explaining why the BoJ felt compelled to widen the interest rate band. As explained last week, the BoJ became concerned with some dysfunction along the yield curve. Haruhiko gave a specific example this time around:

“For example, interest rates of bonds with 8-9 years of maturity had been higher than those of bonds with 10-year maturity, and a price gap had been observed between spot and futures markets. In addition, while the yields for on-the-run issues of 10-year JGBs [Japanese Government Bonds], which are eligible for fixed-rate purchase operations, had been at 0.25 percent or lower, issues of 20-year JGBs with a residual maturity of 10 years were traded at a higher interest rate.”

JGB yields serve as reference rates for corporate bond yields, bank lending rates, and other funding rates. The small dysfunction in the JGB yield curve was cascading into widening spreads in the corporate bond market. The BoJ worried that if “market conditions persist, this could have a negative impact on financial conditions such as issuance conditions for corporate bonds.”

Later in the speech, Haruhiko added for emphasis: “the Bank will provide its utmost support by firmly maintaining accommodative financial conditions” (emphasis mine). The BoJ did not include such emphasis in its policy statement last week.

The market seemed to (reluctantly) get the point. The Invesco CurrencyShares Japanese Yen Trust (NYSEARCA:FXY) lost 0.4% on the day.

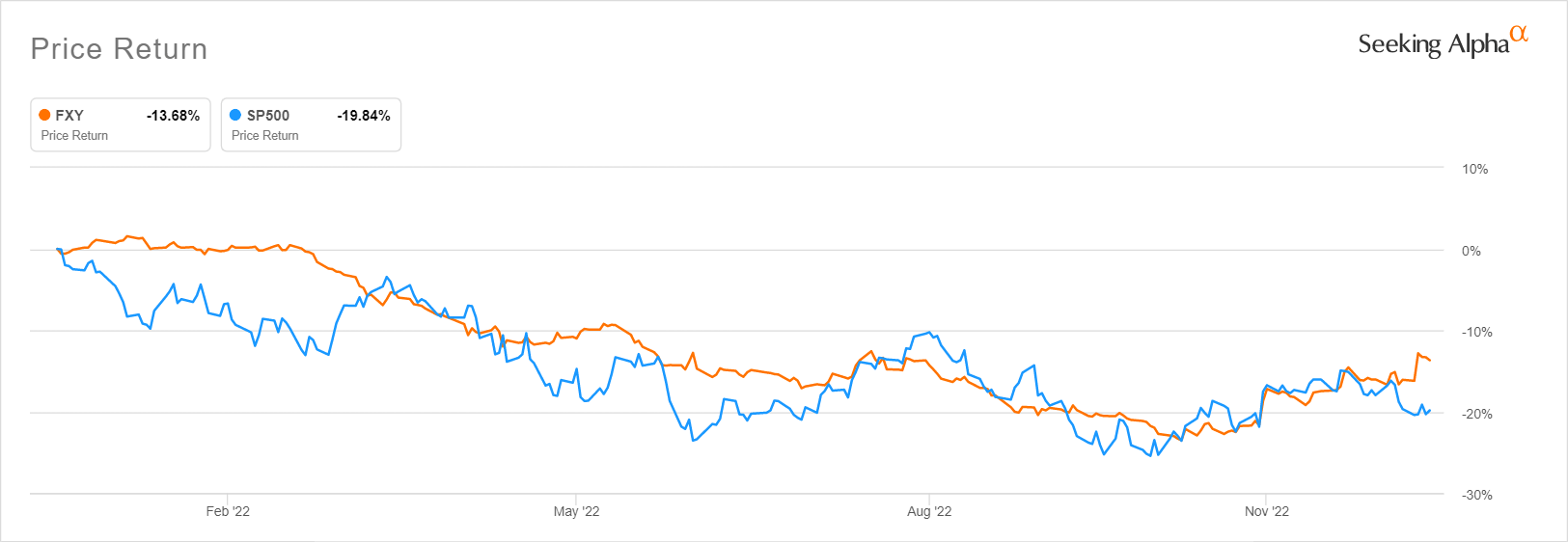

The recent strength in the Invesco CurrencyShares Japanese Yen Trust (FXY) has setup the currency ETF to outperform the S&P 500 this year and next. (Seeking Alpha)

Of course, this pullback is tiny compared to FXY’s 4.1% gain last week in the wake of the BoJ’s statement. Still, the move seems to confirm the upward momentum is over now. However, I remain bullish on the yen and will accumulate on this pullback. I am not bullish because I anticipate that the BoJ will imminently tighten monetary. Instead, I am seeing Japan’s economic advantage in 2023 that could drive incrementally more interest in the Japanese yen.

Everything the Bank of Japan says projects a 2023 where Japan’s economy will out-perform its economic peers. That economic performance will make the yen attractive by itself. Any overshoot in inflation that causes the BoJ to actually take baby steps toward policy normalization will act like a currency bonus.

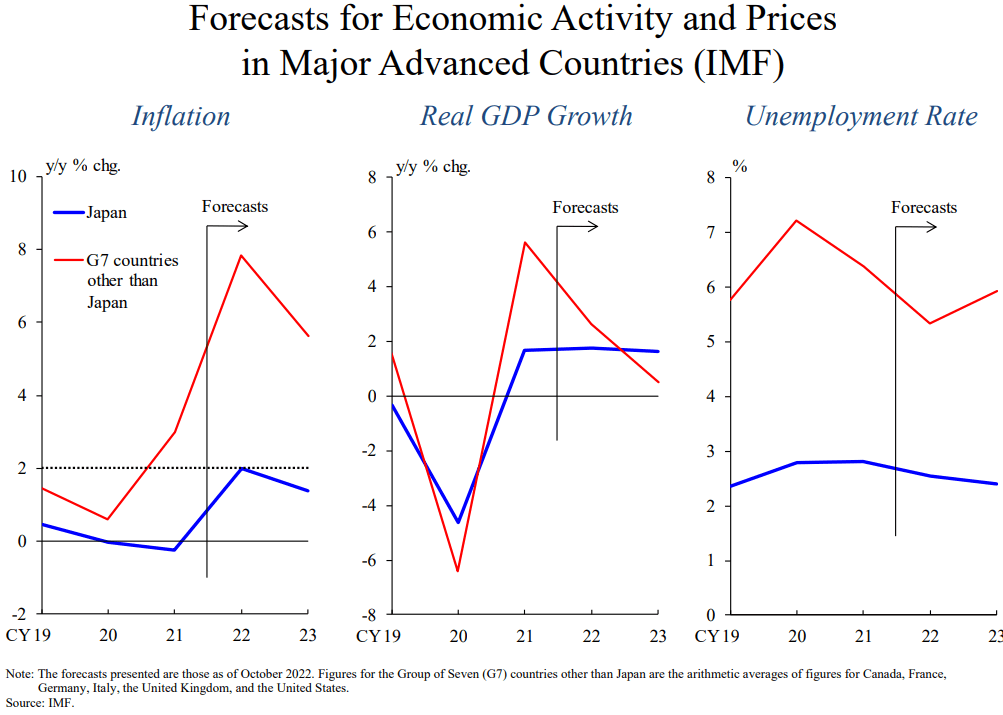

While the eurozone may suffer negative growth, and the U.S. will be lucky to escape with flat growth, the BoJ projects a strong 2023. Japan’s relative advantage in inflation, growth, and unemployment is summarized in these charts from Haruhiko’s speech:

the IMF expects Japan to outperform the G7 in 2023. (Bank of Japan)

Haruhiko explained the anticipated economic divergence: “This is largely due to the difference in the timing of the economic resumption from the pandemic and to the fact that, unlike in the United States and Europe, accommodative financial conditions have been maintained in Japan…The driving force behind the pick-up in the economy has been the recovery in services demand, which is associated with the resumption of economic activity, and the virtuous cycle in the corporate sector from profits to investment.”

Japan’s recovery lag comes from the yet to be unleashed, pandemic-related pent-up demand and accumulated savings in the economy. An increase in the labor supply has also added more aggregate income into the economy that in turn will feed into consumption. Next year’s labor-management wage negotiations may deliver a 3% hike in wages, which is higher than in the past, but not so hot to trigger a wage-price spiral. These wage gains will replace higher input costs as the price supports that have helped Japan elevate out of deflation.

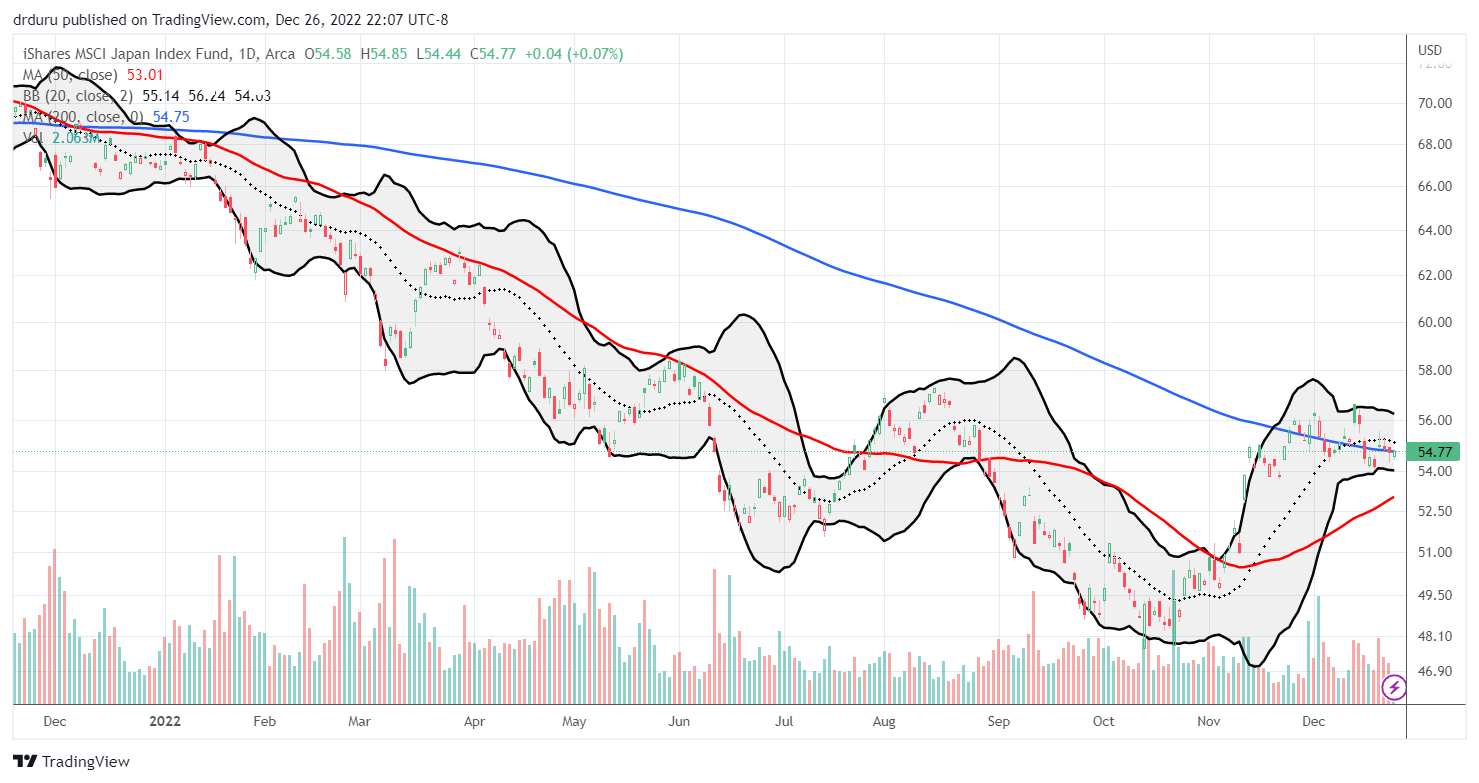

Perhaps 2023 will be the year of Japan. If so, iShares MSCI Japan ETF (EWJ) should be an even better trade than FXY. EWJ is currently flirting with a breakout above its 200-day moving average (DMA). EWJ is down 18% year-to-date and 26% off last year’s all-time high. Japan looks set to outperform next year if forecasts play out as expected.

After a rough year, the iShares MSCI Japan ETF (EWJ) is finally flirting with a bullish 200DMA breakout. (TradingView.com)

Be careful out there!

Be the first to comment