David McNew

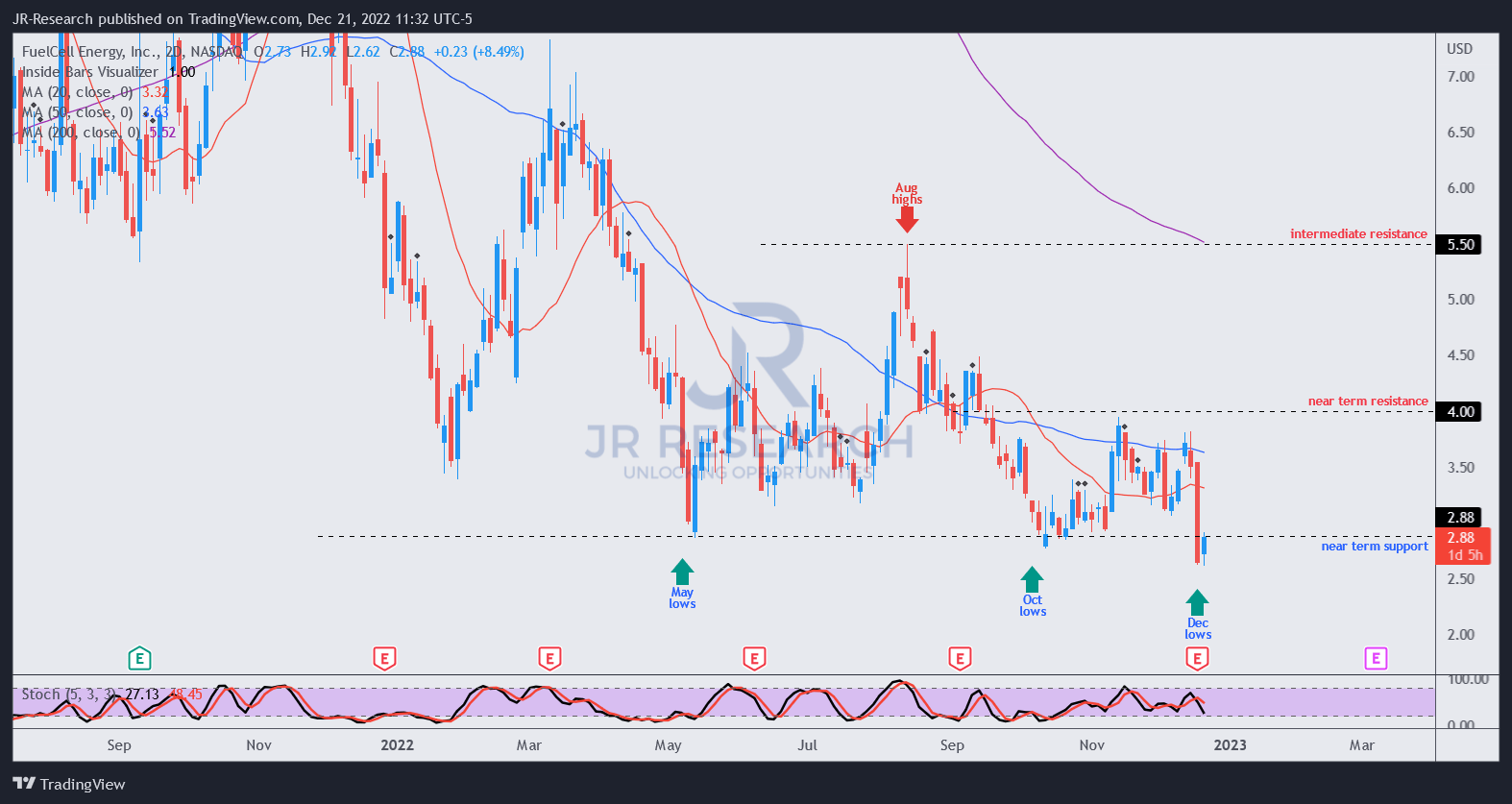

FuelCell Energy, Inc.’s (NASDAQ:FCEL) FQ4’22 earnings release initially sent FCEL down nearly 20%, forcing it to break below its May and October lows.

However, the extent of the steep selloff also likely created a potential bear trap for investors looking for a downside break of its critical support zone. Shrewd market operators have probably used the selloff to cover a highly profitable short setup predicated against its pre-earnings December highs.

We cautioned investors in an early September piece that FCEL’s momentum has weakened further. It has also lost all its gains from the passage of the Inflation Reduction Act (IRA) in August.

Moreover, FuelCell reported a significant reduction in its backlog by nearly 15% YoY, as the company determined that its “economic profile” was no longer attractive based on the terms of its contracted power purchase agreements (PPA). Notably, CEO Jason Few’s commentary suggested that the elevated natural gas pricing likely impacted the project’s feasibility, as he articulated:

It’s a project where we had exposure to gas prices. And as we looked at when we originally did this agreement to now, there’s been a pretty significant shift in gas prices. And so, as we looked at our ability to manage the gas price risk and that exposure, the risk around interconnection, we made a decision that right now, this program didn’t make sense for us to continue to move forward. That being said, we will continue to have conversations and look for ways to restructure that PPA. And if we can, we’ll look to bring that back into the backlog. (FuelCell FQ4’22 earnings call)

Given the surge in natural gas prices in 2022, we believe negotiating and restructuring its PPA is sensible. However, it has also impacted its backlog markedly, potentially resulting in lower revenue growth moving ahead.

Despite that, the company remains confident in meeting its medium-term FY25 revenue target (year ending October 2025) of $300M. In addition, CFO Mike Bishop reminded investors that the IRA tailwinds have not been reflected in its targets, suggesting that the company “[expects] to revise [its] long-term revenue targets during fiscal year 2023.”

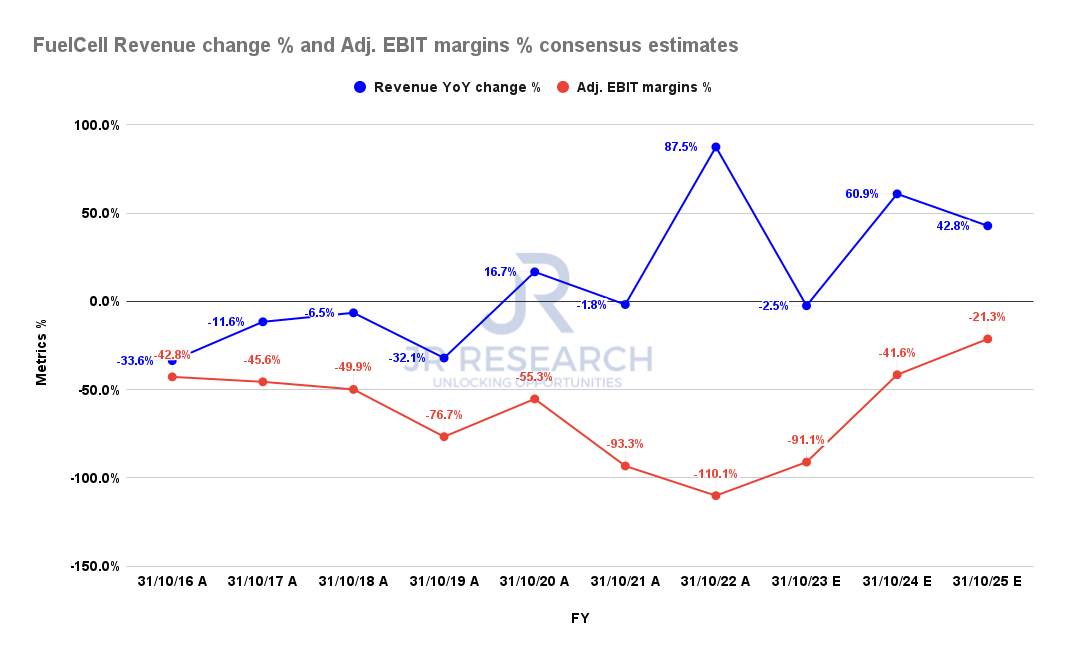

FuelCell Revenue change % and Adjusted EBIT change % consensus estimates (S&P Cap IQ)

However, with the company expected to report losses through FY25, we believe the de-rating yesterday was necessary, helping to reset investors’ expectations.

The company reported cash and equivalents of $481M, including $458M of unrestricted cash. Based on the revised consensus estimates, the company could reach its FY25 revenue target with sufficient cash flow runway.

However, we believe the market needs to de-risk FuelCell’s FY25 revenue target of $300M, as FuelCell is projected to report a revenue decline of 2.5% in FY23.

As a result, it has ratcheted up the need for the company to meet more challenging revenue growth requirements in FY24-25, suggesting potential downside risks to its guidance.

Hence, investors need to consider whether elevated natural gas pricing could persist in the medium term, complicating the company’s efforts to scale its manufacturing capacity.

While we may not witness those spikes in NYMEX (NG1:COM) and Dutch TTF futures last seen in August/September, demand/supply dynamics could remain structurally tight.

Bloomberg also discussed in a recent article that “the market is expected to remain tight until 2026 when additional production capacity from the US to Qatar becomes available.”

Therefore, Europe’s energy crisis could continue to hamper FuelCell’s ability to scale toward profitable growth.

Moreover, FCEL remains priced at a premium against its peers. Given its unprofitability, we could only rely on our less preferred revenue multiples to assess its relative valuation.

Accordingly, FCEL last traded at a NTM revenue multiple of 7x, well above its peers’ median of 5.6x. Hence, we assessed there’s little doubt that the market has priced FCEL for growth.

Therefore, the reduction in its backlog is an unwelcome development, suggesting that the market cannot ignore potential downside execution risks moving ahead. Consequently, investors also need to be wary about further writedowns to its estimates, impacting its recovery momentum.

FCEL’s dominant medium-term trend remains to the downside. Hence, investors buying at the current levels are going against the market’s bias. As such, any exposure should be considered speculative.

If you have a long/short portfolio, taking a short exposure against FCEL’s well-established resistance zones could have yielded a solid performance since its November 2021 highs.

Hence, FCEL remains a prime target for short-sellers, as it reported a short interest as a percentage of shares outstanding of nearly 12% recently.

FCEL price chart (2-Day) (TradingView)

Notwithstanding, we see a potential speculative setup at the current levels, as seen in FCEL’s 2-Day chart.

The steep selloff appears to have created a bear trap (pending validation), which could offer investors a reasonable reward/risk entry zone for a mean-reversion rally against its bearish bias.

However, investors need to apply robust risk management plans for this setup, as we believe FCEL is not a stock you want to apply “diamond hands” on.

Therefore, a price target (PT) below $3.5 looks appropriate. Depending on your stop-loss level, the reward/risk ratio seems reasonable, allowing more than a 2:1 ratio.

Revising from Hold to Speculative Buy with a max. PT of $3.5.

Be the first to comment