Kativ

Despite market volatility, FS Bancorp, Inc. (NASDAQ:FSBW) remains a durable company. It keeps a sound performance despite the rising prices and interest rates. Operating revenues grow while margins start to rebound from the sharp plunge. Its impeccable loan and security quality and growth generate more returns. However, it must still watch out for loans as they appear excessive relative to deposits.

Thankfully, cash levels remain adequate to cover outstanding borrowings and dividends. These are visible in the consistent dividend payouts and attractive yields.

Meanwhile, the stock price stays consistent with the fundamentals. The recent downtrend opens an entry point for a buy position.

Company Performance

The recession specter has seeped into every household amidst interest rate hikes. Despite this, FSBW rebounds and becomes more resilient. Inflation is not a friend, so the bank is getting a firm hold of its operations as it lulls. The downtrend, matched with the increase in interest rates, works in favor of the company. But it must be more careful, as a massive portion of its market is more volatile than others.

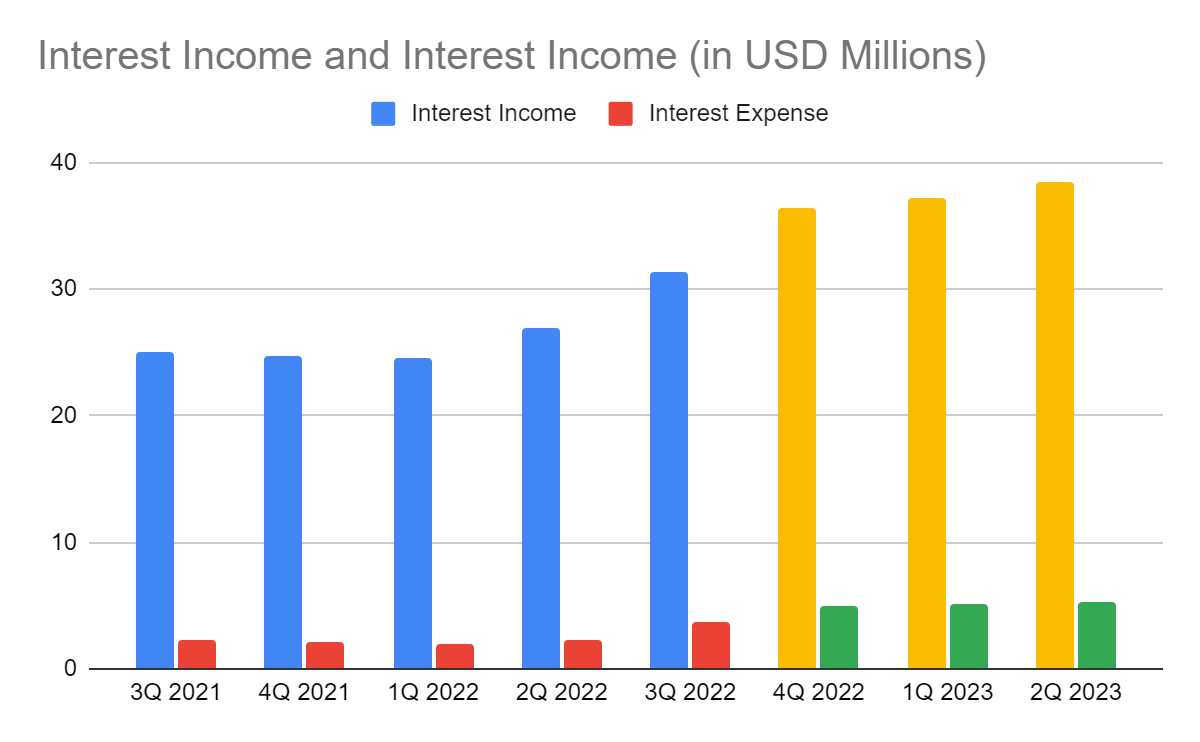

The operating revenue amounts to $31 million, a 25% year-over-year increase. In addition, sequential values show a consistent uptrend in 2022. Interest income on loans remains the main driver, with a 26% year-over-year growth. The remaining component from income on securities also shows an uptrend of 17%. With that, all its segments have relative stability. I will focus on the two primary factors helping maintain steady revenue growth.

First, FSBW had a substantial loan growth of 20%. It comes mainly from real estate loans. If we split it between C&I and consumer and personal loans, they comprise 24% and 57% of the total loans. The remaining 19% comes from construction and other forms of loans. It is consistent with the still-fired-up real estate market. House prices and mortgages stay elevated.

Interest Income And Interest Expense (MarketWatch)

However, it must run its business with extra caution as the market remains uncertain. Although house demand remains high, buyers may adjust their demand or shift to other alternatives. The US housing market analysts are wary of the current pattern. They anticipate the second-largest market crash since the Great Depression. Nevertheless, I am still optimistic as I see factors that may keep risks at bay. I will discuss more of them in the next section.

Another revenue growth contributor is its prudent security diversification. Although yields comprise a small portion of revenues, these are forces to reckon with. Most of these securities are composed of municipal bonds and US agency securities. As such, FSBW has more inflation-linked securities, which can generate higher yields. These have an extra shield against inflation and devaluation. Deposits in other banks also generate more interest income for the company.

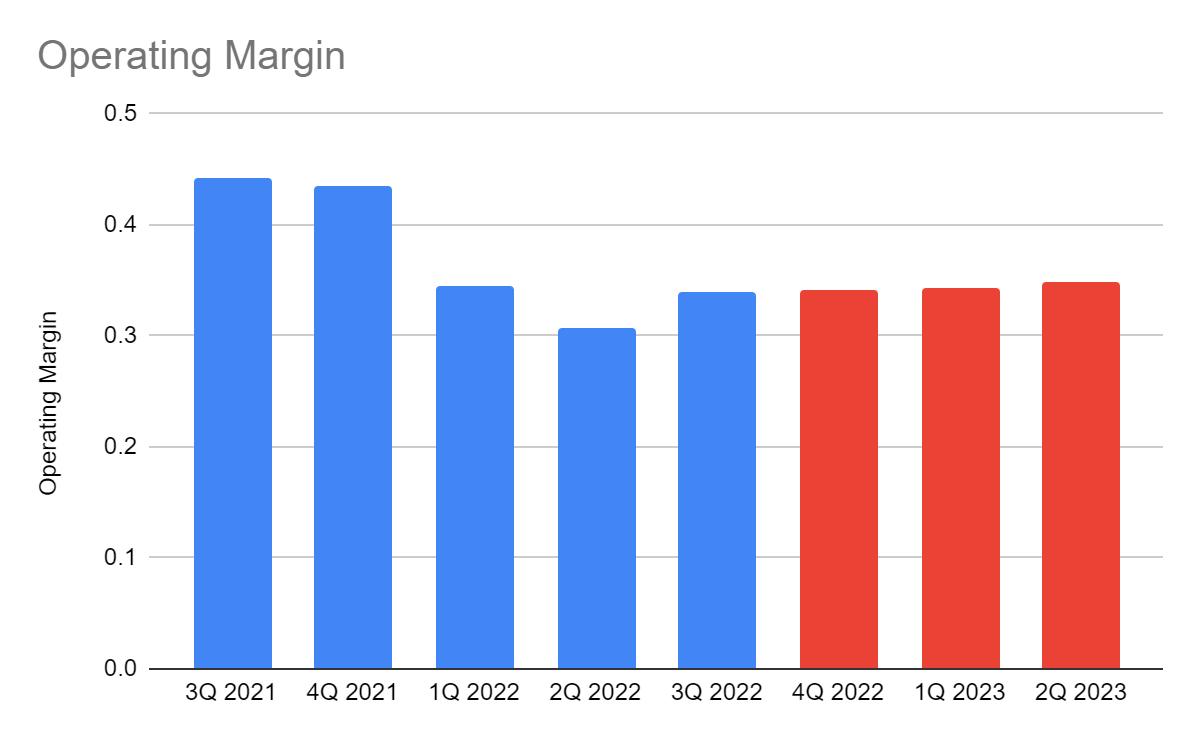

Moreover, FSBW focuses on what it can control and does best. It maintains its efficiency to stabilize costs and expenses despite the increased NPAs. Its interest segment has higher expenses, showing deposits are more interest-sensitive. Note that there is a substantial increase in interest-bearing, unlike non-interest-bearing deposits. Meanwhile, non-interest segment expenses remain well-managed. Thanks to the continued inflation lull, helping FSBW lower its direct expenses. With that, the operating margin rebounds to 34% from 30% in 2Q 2022. Despite the year-over-year decrease, a sequential improvement continues.

Operating Margin (MarketWatch)

FSBW may have a higher operating capacity this year. FSBW just got several Columbia Banking System (COLB) branches. They have a similar loan structure, except that it has a higher concentration on C&I loans. Also, it appears to be more conservative with provisions of 1.32% versus FSBW with 1.24%. They also seem more interest-rate sensitive, which can be a great addition. With increased domestic presence and interest rates, interest income and expenses may rise. Meanwhile, I expect its operating margin to be almost unchanged. Interest rates have yet to peak, which can compress near-term margins.

How FS Bancorp, Inc. May Withstand Market Changes

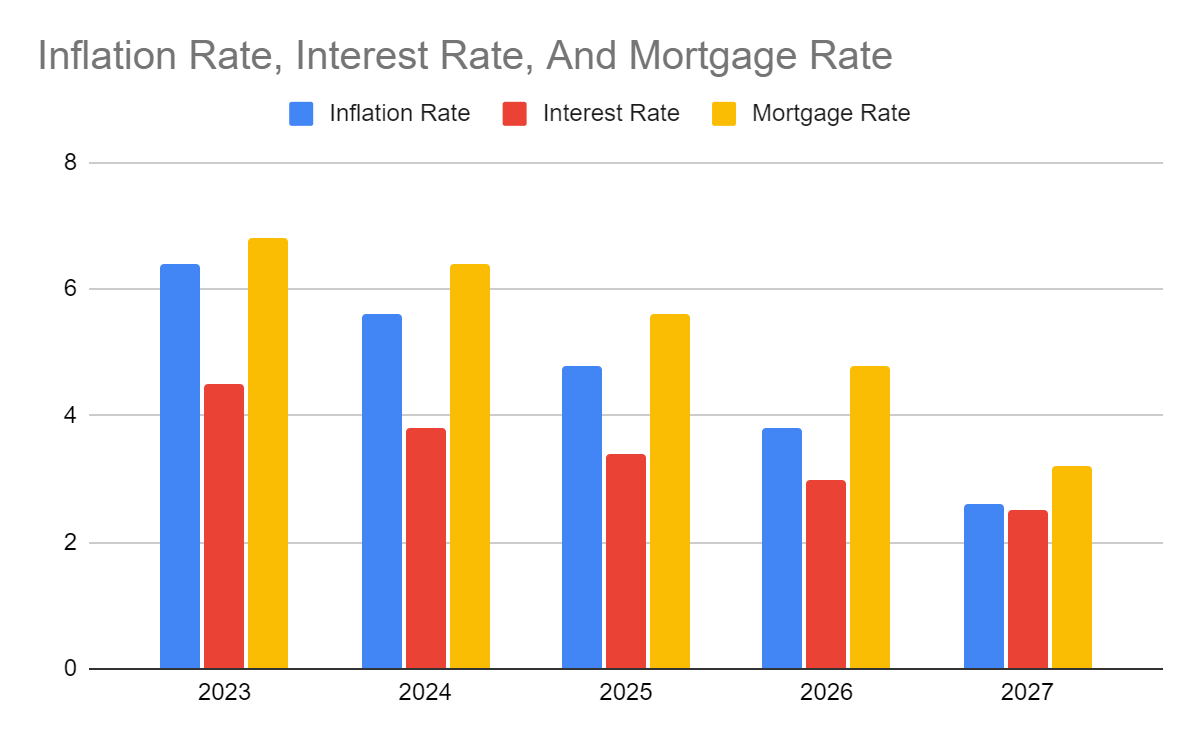

Clearly, inflation is not a friend of FS Bancorp, Inc. We can see how it drops and rebounds in line with inflation changes. If the lull continues, it may keep decreasing to pre-pandemic levels in the following years. Meanwhile, I expect interest rates to keep increasing this year. The Fed must remain conservative to stabilize inflation further. But I also expect its increments and peak to be lower than anticipated. The same goes for mortgage rates. Their trends may become uniform. With the faster inflation drop, I expect higher returns for mortgage lenders and brokers. When interest rates cool down, there may also be more loan demand and stable deposit costs. It matches with its acquisition of several COLB branches.

More importantly, I don’t think the current property market trend will lead to a crash affecting FSBW. Other factors must be considered despite the cooling of property sales. Property inventories remain low to meet the current market demand. Let’s face it, property builders have not fully ramped up since the 2007 market crash. Demographic changes with stable unemployment may also open opportunities. Also, strict lending standards can help lower foreclosures of commercial and personal properties.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

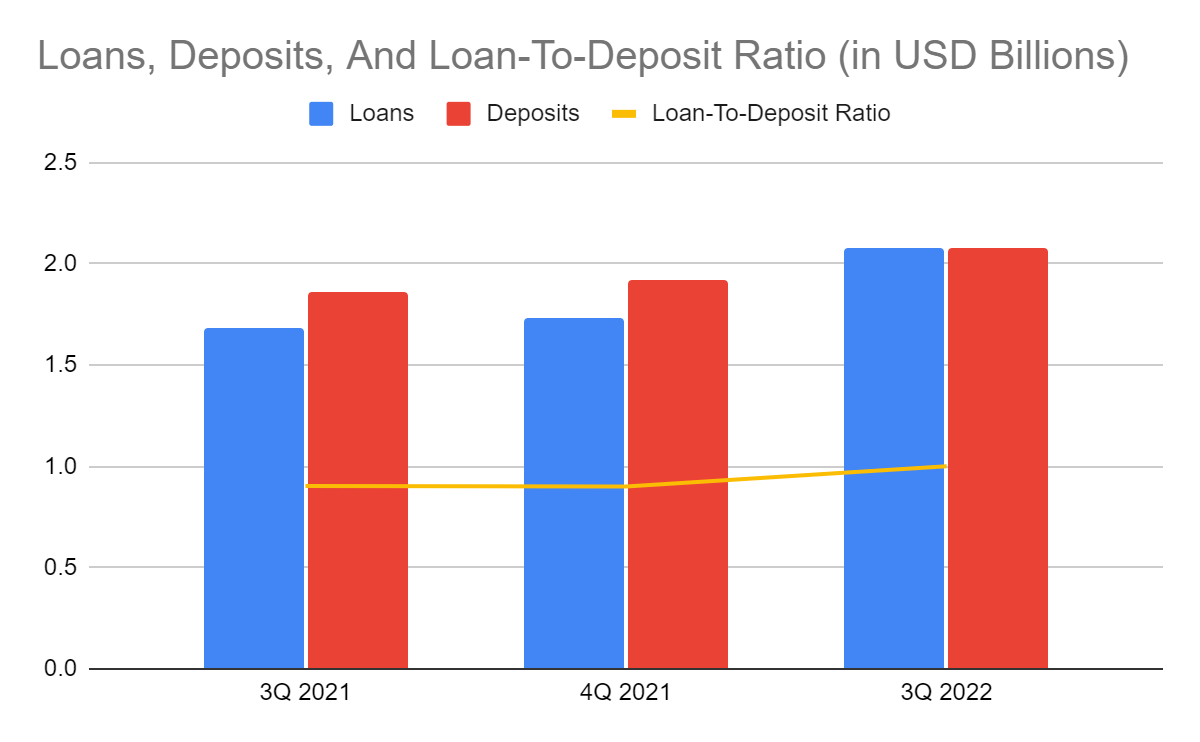

What may drive the sustainability of FS Bancorp, Inc. is its loans and deposits. Loan growth is impeccable despite the interest rate hikes. My worry is that loans are excessive relative to deposits. The loan-to-deposit ratio is already 101% vs 90% in 3Q 2021. Also, the efficiency ratio is lower, showing increased sensitivity of deposits relative to loans.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

But I expect the company to improve liquidity by setting higher interest rates to entice more deposits. It may even try to securitize a portion of its loan portfolio. Near-term results may not be as desirable as the current quarter, but they may pay off in the long run. Also, the company has improved efficiency despite the increased non-performing assets. It has a 1.34% ROAA, higher than the first two quarters.

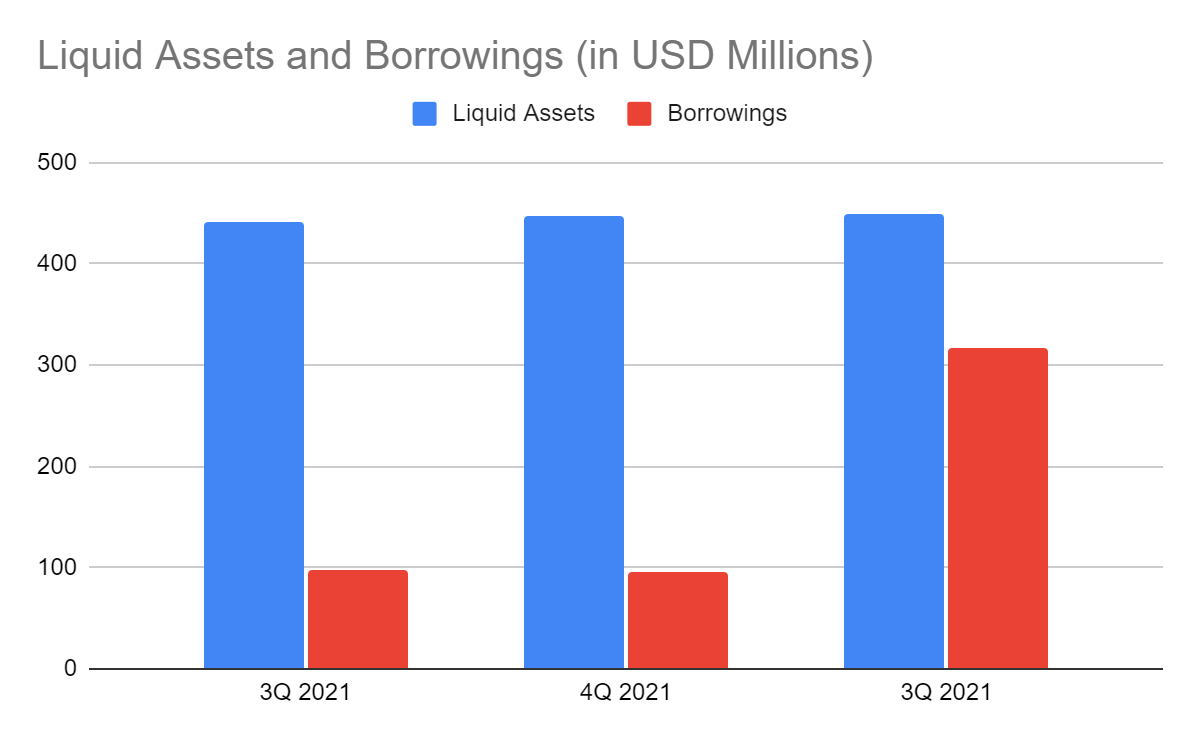

Moreover, cash and investments are on a steady increase. They can cover borrowings despite the higher interest expenses. With 17% of the assets, the company remains liquid.

Liquid Assets And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of FS Bancorp, Inc. shows a slight downtrend after its most recent peak. But the overall pattern remains upward. At $33.10, it is 4% lower than November highs. Despite this, an investor may see this as an opportunity to make a position. With a price-earnings multiple of 8.95x and my 2023 EPS estimates of $4.1, the target price is $36.78. NASDAQ is more optimistic, with EPS estimates of $4.3, showing a target price of $38.57. With that, there may be an 11-17% uptrend in the next 12-18 months. Even better, dividend payments are still well-covered. Growth may still be inconsistent, but payouts are continuous. Also, it has an attractive dividend yield of 2.4%, way better than the NASDAQ composite average of 1.27%. It has a dividend payout ratio of 19%, so there is still adequate capacity to sustain it. To assess the stock price better, we will use the DCF Model.

FCFF $24,000,000

Cash $11,500,000

Borrowings $317,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 7,704,373

Stock Price $33.35

Derived Value $38.48

The derived value is adherent to the undervaluation using price-earnings multiple. There may be a 16% upside in the next 12-18 months. Investors may use this opportunity to buy the stock at a discounted value.

Bottom line

FS Bancorp, Inc. faces market headwinds hampering its growth. But it stays durable with its stable margins and prudent asset management. It has adequate cash levels to sustain operations, pay borrowings, and cover dividends. Even better, the stock price seems undervalued, an entry point for investors. The recommendation is that FS Bancorp, Inc. is a buy.

Be the first to comment