Lemon_tm

Introduction

I’ve written two bullish articles on SA about third-party logistics provider Radiant Logistics (NYSE:RLGT), the latest of which was in October when I said that accounting errors stemming from the timing of the recognition of the estimated accrual of in-transit revenues and related costs were unlikely to affect the FY22 EBITDA and net income to a large extent.

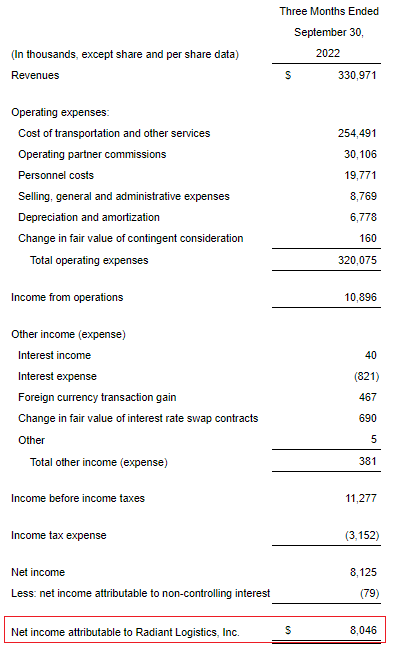

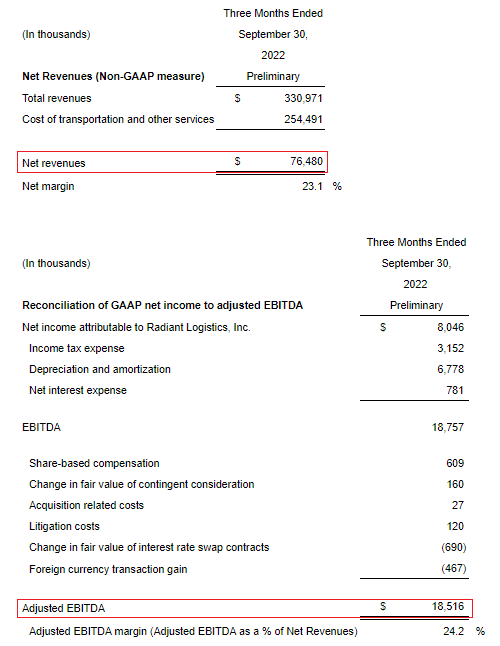

While Radiant still hasn’t released its FY22 annual report or its restarted FY21 accounts, on November 9, it posted preliminary financial results for the quarter ended September 2022 and I think they look compelling. Net revenues rose by 17.9% year on year to $76.5 million while adjusted EBITDA soared by 27.3% to $18.5 million. Considering the purchase of Minnesota-based sector player Cascade was completed in early October, Q4 2022 could see a further improvement in financial performance. In addition, Radiant repurchased over half a million shares in the four months ended October 2022 and I think that the bull case looks better than ever. Let’s review.

Overview of the Q3 2022 financial results

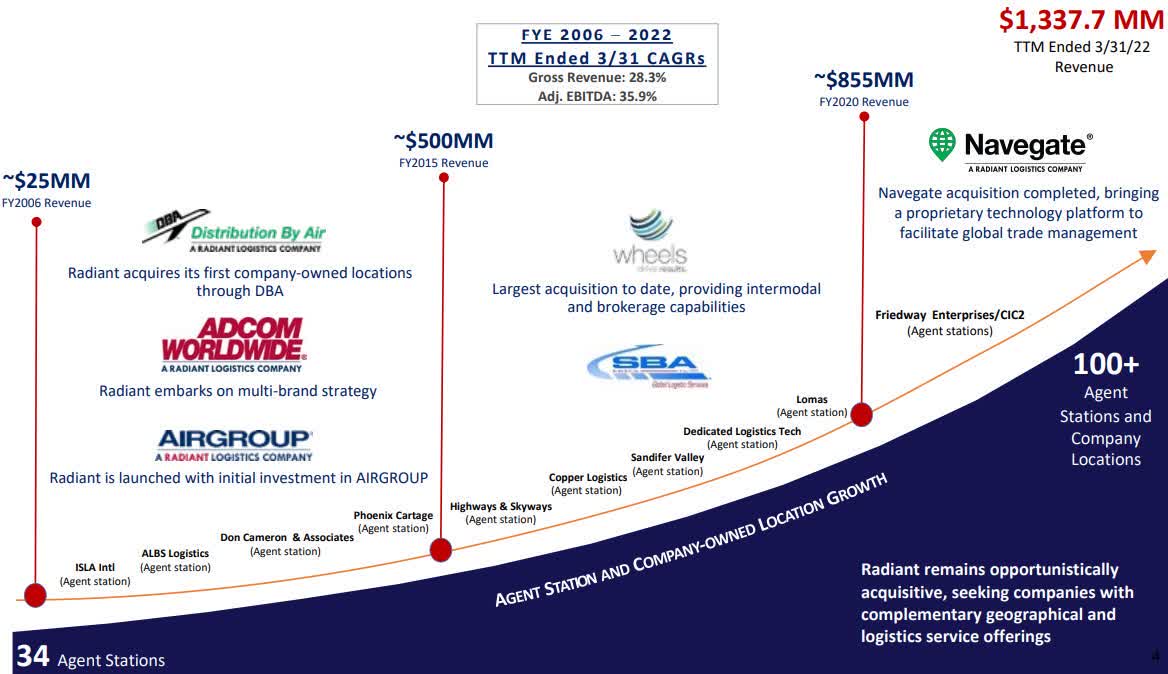

In case you haven’t read any of my previous articles about Radiant, here’s a quick description of the business. The company specializes in the provision of air and ocean freight forwarding and truckload, less-than-truckload, and intermodal freight brokerage services and its main markets include the USA and Canada. The majority of net revenues come from freight forwarding. The company has more than 12,000 clients but none of them accounts for over 4% of net revenues. Over the past several years, Radiant has been expanding its operations rapidly thanks to the acquisition of companies with complementary geographical and logistics service offerings, with compound annual growth rates for gross revenues and adjusted EBITDA between FY06 and FY21 of 28.3% and 35.9%, respectively.

Radiant Logistics

The latest announced acquisition includes a company named Cascade, which has been operating as a strategic operating partner under its Airgroup brand since 2007. Today, Radiant has over 100 operating locations worldwide offering a wide range of services ranging from supplying white-glove delivery services to the retail sector to transporting heavy machinery.

To be fair, Radiant’s financial results in FY21 received a significant boost from supply chain disruptions and COVID-19 test kit chartering. In Q1 2022 alone, the company was involved in the chartering of 24 aircraft flying 85.4 million COVID test kits and revenues from its COVID-related charter business stood at $62.2 million during the period. With the global supply chain returning to normal and COVID lockdowns around the world ending, Q3 2022 net revenues and adjusted EBITDA slumped by 13.6% and 33.2% quarter on quarter, but they were much higher than I expected them to be. Back in July, I said that EBITDA levels could drop to about $10 million per quarter in the near future. Yet, this was Radiant’s best third quarter in its history, with net revenues, EBITDA, and net income all at record levels for this period of the year. Compared to Q1 FY22, net revenues, adjusted EBITDA, and net income rose by 17.9%, 27.3%, and 13.7%, respectively.

Radiant Logistics Radiant Logistics

Also, Radiant generated an estimated $25.6 million in cash from operations and invested $1.3 million in the repurchase of 219,517 shares at an average cost of $6.11 during the quarter. Another 352,231 shares were bought back in October for a total of $2.1 million thus bringing the number of shares outstanding down to 48,315,935. In February 2022, the company renewed its stock buyback program which allows it to repurchase up to 5 million shares through December of 2023 and I think this could provide a significant boost for the share price in the near future.

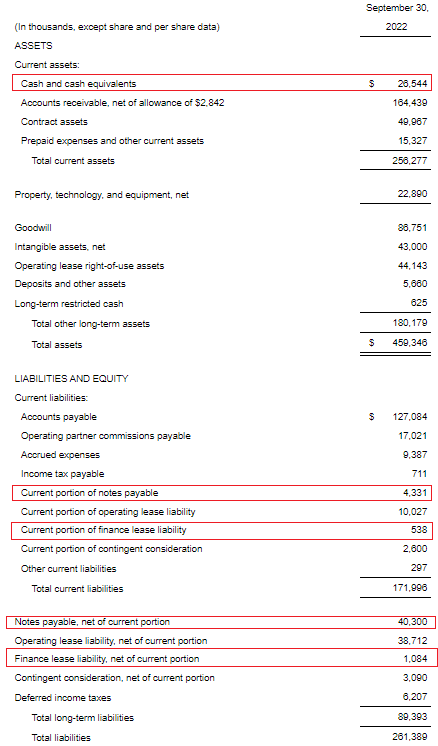

In my view, the balance sheet looks strong as Radiant’s net debt was down to $19.7 million as of September while cash and cash equivalents stood at $26.5 million. Back in September 2021, net debt was $35 million, and I wouldn’t be surprised if the company makes another major acquisition over the coming months.

Radiant Logistics

The enterprise value stands at $273 million as of the time of writing and the EV/EBITDA ratio on an annualized basis is just 3.7x. If we take a conservative approach and assume that quarterly EBITDA drops to about $10 million per quarter in the coming year due to an economic slowdown, the EV/EBITDA ratio would still be below 7x. I continue to think that Radiant should be trading at around 12x EV/EBITDA thanks to its history of compelling growth since its founding in 2005 and this would put the share price at about $9.50.

Turning our attention to the risks for the bull case, I think that there are two major ones. First, the US economy could enter a prolonged recession in 2023 which is likely to put significant pressure on the logistics sector. It’s possible that Radiant’s quarterly EBITDA dips below $10 million per quarter. Second, some investors could be keeping away from this stock due to the unresolved accounting issues. It’s unclear when the company will publish its FY22 annual report.

Investor takeaway

I view Radiant as a compounder with a compelling track record of growth and I’m pleasantly surprised that net revenues and EBITDA are still at high levels after the boost from supply chain disruptions and COVID-19 test kit chartering to its business has faded. The company’s balance sheet looks strong as net debt is down below $20 million and the number of shares outstanding has declined by 1.5 million since September 2021 thanks to buybacks.

Overall, I think that Radiant is undervalued but I rate it as a speculative buy considering major economies around the world seem perilously close to a recession.

Be the first to comment