welcomeinside/iStock via Getty Images

I have a Hold rating on the shares of Frontier Airlines (NASDAQ:ULCC). The company recorded a small profit in its most recent quarter and is gearing up for significant growth in the coming year.

Company overview

Frontier is the seventh largest U.S. airline, and the second largest of the three ultra low-cost carriers, behind Spirit (SAVE) and ahead of Allegiant (ALGT). It had agreed to merge with Spirit earlier in the year, only to be outbid by JetBlue (JBLU), an unexpected turn of events that could turn out to be a major blessing in disguise as it can focus on its unique strategy and the significant embedded growth it has for 2023 and beyond.

Strong shareholder alignment

Indigo Partners, an airline-focused private equity firm founded by industry veteran Bill Franke with particularly deep expertise in founding and managing low-cost airlines, has created several valuable low cost carriers, including Spirit (SAVE), Wizz Air (OTCPK:WZZAF) and Volaris and has investments in Frontier, Volaris, and JetSMART. It acquired Frontier from Republic Airways in 2013 and has been its majority shareholder ever since. It currently owns over 80% of its shares with a market value of approximately $1 billion, which represents its largest current investment in the sector by a wide margin. While it has already taken significant dividends from the airline prior to its IPO, and will eventually look to exit its shares, it should be very motivated to maximize the value of this equity. Indigo’s other airline relationships are a benefit to Frontier, including its partnership with Volaris. It has also utilized the group of airlines to increase bargaining power with Airbus to order aircraft at attractive prices. With the stock about 40% below its IPO price, hopefully Indigo will not look to exit prior to a substantial rebound in share price.

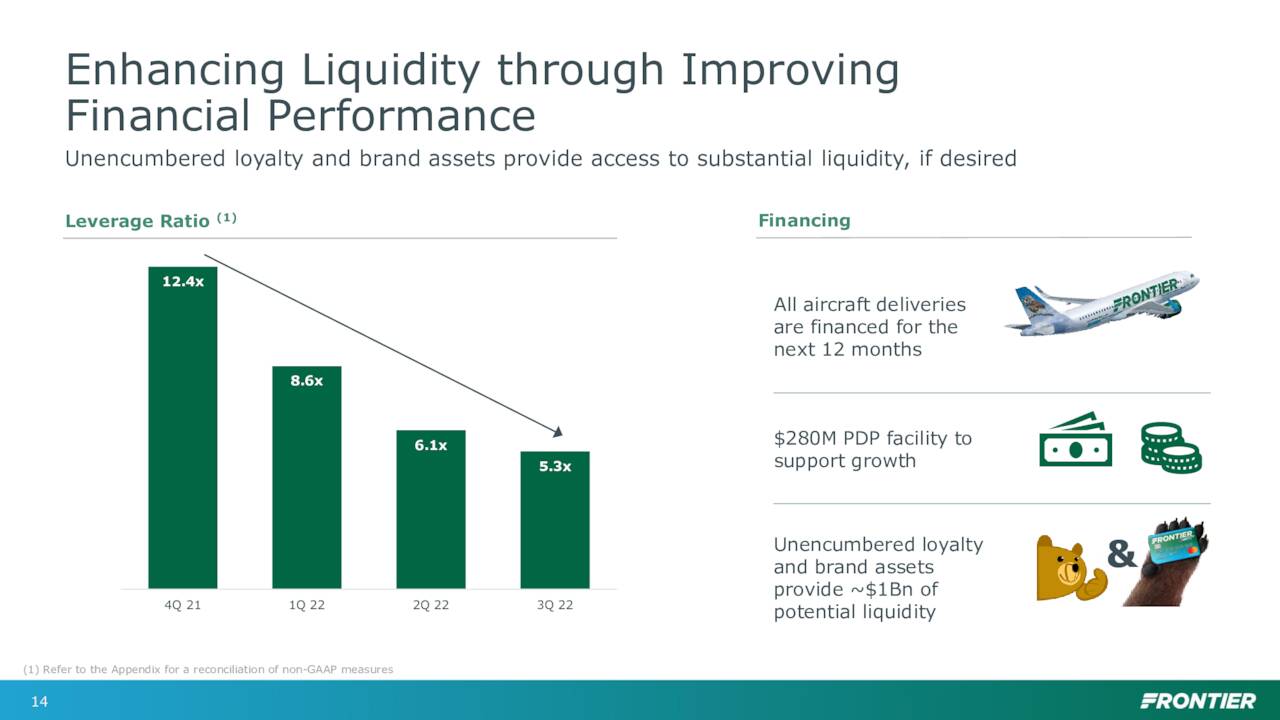

Capital allocation

This is a growth story more than most other airlines, so capital returns in the near-term are fairly unlikely, as the focus remains on managing leverage while funding growth of the business, including delivery of over 200 aircraft that the airline has on order from Airbus. They have a longstanding pre-delivery payment (PDP) credit facility to manage progress payments on these aircraft, and will likely continue to favor lease financing to minimize near-term capital outlays in order to facilitate growth. Their leasing partners may be willing to finance PDPs for them as well as a sweetener to any lease financings, and they’ve already secured financing for the next 12 months’ worth of deliveries. In the meantime, the airline will opportunistically add further capacity, as shown by its decision to source an additional ten A321neo aircraft from lessors that will deliver this quarter and during 2023. The repayment of its loan from the U.S. Treasury “substantially unencumbered” its valuable loyalty and brand assets, which could provide significant liquidity if needed to support expansion.

Source: Frontier Airlines

Risks to investment thesis

Economic recession

Though recession may be the end result of Fed tightening, even a severe recession would likely be more manageable than the upheaval caused by COVID-19. Frontier has already succeeding in reducing leverage from a year ago which, while still somewhat elevated, is down significantly. Leverage should remain modestly elevated for some time given their growth plans; however, the company likely has a reasonable amount of flexibility to defer aircraft deliveries in order to preserve cash. In addition, the fact that its fleet is almost entirely leased gives them an ability to negotiate with their lessors, who supported the airline with payment deferrals through the pandemic. Frontier’s focus on leisure travelers and on minimizing costs present an interesting dichotomy in a potential recession – on the one hand, they are the lowest cost provider of capacity, which should give them a built-in advantage against peers, but they’re also potentially exposed to the most price-sensitive customer that might delay traveling in an economic downturn.

Source: Frontier Airlines

The loyalty and brand assets are likely their only significant sources of cash that would not involve dilution of shareholders; however, the potential for them to generate $1 billion in proceeds from these provides material flexibility should market conditions worsen.

Fuel and interest rate hedging

Fuel and labor are the two biggest costs for airlines, and there is some chance that fuel costs exceed recent levels, which would result in substantial additional expenses for the company. Frontier has not recently utilized derivative contracts or other methods to hedge its fuel costs. Its biggest hedge when it comes to fuel is the proportion of next-generation aircraft it operates, which is high and continues to rise given its significant order backlog and gradual roll-off of leases of older-technology equipment. These aircraft have more fuel-efficient engines and more seats, which both act to reduce the airline’s fuel CASM. It has minimal revenues and expenses in foreign currencies which is a positive. It has put in place interest rate hedges related to $245 million in aircraft rent related to seven aircraft which deliver next year. Most of the company’s leases are likely tied to an interest rate benchmark to set the rent payable, so this will hopefully provide some protection against rising rate levels. Per the company, lease rates are usually set based on the seven-year or nine-year swap rate, so its existing obligations should be fixed, though future deliveries are likely to fluctuate prior to delivery based on the level of those benchmarks.

Conclusion

Frontier’s business model is unique amongst U.S. airlines and it has made significant strides since Indigo acquired it in 2013. Their focus on leisure travelers, cost savings and a differentiated product has given it momentum, and the airline has increased non-fare revenue per passenger by nearly six times since Indigo took over. However, a 35% growth in capacity is large in any year, particularly one with as much industry and macroeconomic uncertainty as currently exists. For this reasons, we would either wait for the picture to become clearer, or for share prices to decline further, prior to making an investment in Frontier shares.

Be the first to comment