If you see danger and the herd sees the same danger, should you feel safe? Maybe you need to be looking at what the herd does not see.

Laurinson Crusoe/iStock via Getty Images

The current “consensus” view among US economic analysts is that the US economy will experience a recession at some point during the next 12 months. In this article we will document the nature and extent of this confluence of opinion by reviewing data from a wide variety of sources that document current expectations about the probability of recession.

Through the research provided in this article, readers will be able to acquire a sense of the truly remarkable extent to which the expectations of a US recession during the next 12 months has become the “consensus” view. Furthermore, readers will be able gain an appreciation for the extent to which this consensus view is currently shared by a very wide array of constituencies, including professional economic forecasters, corporate executives, fund managers, professional investors and retail investors.

The extraordinary confluence of opinion documented in this article naturally raises the question: “Given the remarkably strong consensus expectation of a recession, are all of the potential negative effects of a prospective recession already fully discounted in the stock market?”

But before answering this question about the potential effects of a “consensus,” we believe it is important to actually document the existence of and the extent of this “consensus” — with data and within proper context.

Professional Economic Forecasters: Expectations of Recession

Below are examples of three important surveys that document the expectations of professional forecasters regarding the probability of recession in the next 12 months:

1. Philadelphia Fed Survey of Professional Forecasters. For over 50 years, through its Survey of Professional Forecasters, the Philadelphia Fed has surveyed a large group of professional economic forecasters and has documented their economic outlooks on a number of critical macroeconomic issues. One of the sections in the survey asks economists to estimate the probability of negative quarter-on-quarter (QoQ) GDP growth during the current quarter and the next four quarters into the future. Although the survey does not specifically ask the forecasters what their estimated probability of recession is, one can approximately infer the probabilities that they assign to prospective recessionary conditions by carefully observing the probabilities that they assign to the possibility of negative GDP growth during the current quarter and for each of the next four quarters.

According to the latest edition of this survey released in November 2022, if you take the average probability of negative quarter-on-quarter (QoQ) GDP growth estimated for each of the next four quarters, and then average them, the resulting figure is 46.55%. In the 54-year-old history of this survey, this was, by far, the highest estimate of future recessionary growth, that has been recorded while the US economy was estimated (by the same forecasters) to presently be in expansion. Indeed, the only other times in which the probability of negative QoQ GDP growth in future quarters was estimated to be greater was when the US economy was already in recession.

Average probability of negative QoQ GDP growth, average of next 4 quarters. (Philadelphia Fed Survey of Professional Forecasters, Investor Acumen)

In order to put these figures in context, it will be useful to keep in mind the following reference points obtained from aggregating data from the 52 years of the history of this survey.

A. Expansion. During times of economic expansion, the average probability of negative QoQ GDP growth, averaged over the next four quarters, was 16.41%, compared to 46.55% currently.

B. Recession. During times of economic recession, the equivalent figure cited above was 28.16%, compared to 46.55% currently.

C. Pre-Recession. During the 12 months leading up to a recession – the situation that economists generally consider the US economy to be in right now – the historical average estimates were 25.25%, versus 46.55% currently.

D. All. The average of all estimates during the entire 52-year history of the survey were 17.98%, compared to 46.55% currently.

Therefore, the current expectations of future recession that are being reflected in this survey are both remarkable and unprecedented.

2. WSJ Economic Forecasting Survey. According to an extensive survey of economic forecasters that has been regularly updated by the Wall Street Journal for over 35 years, as of October 2022, the average probability of recession as estimated by the participants was 63%. This figure is unprecedented outside of an ongoing recession.

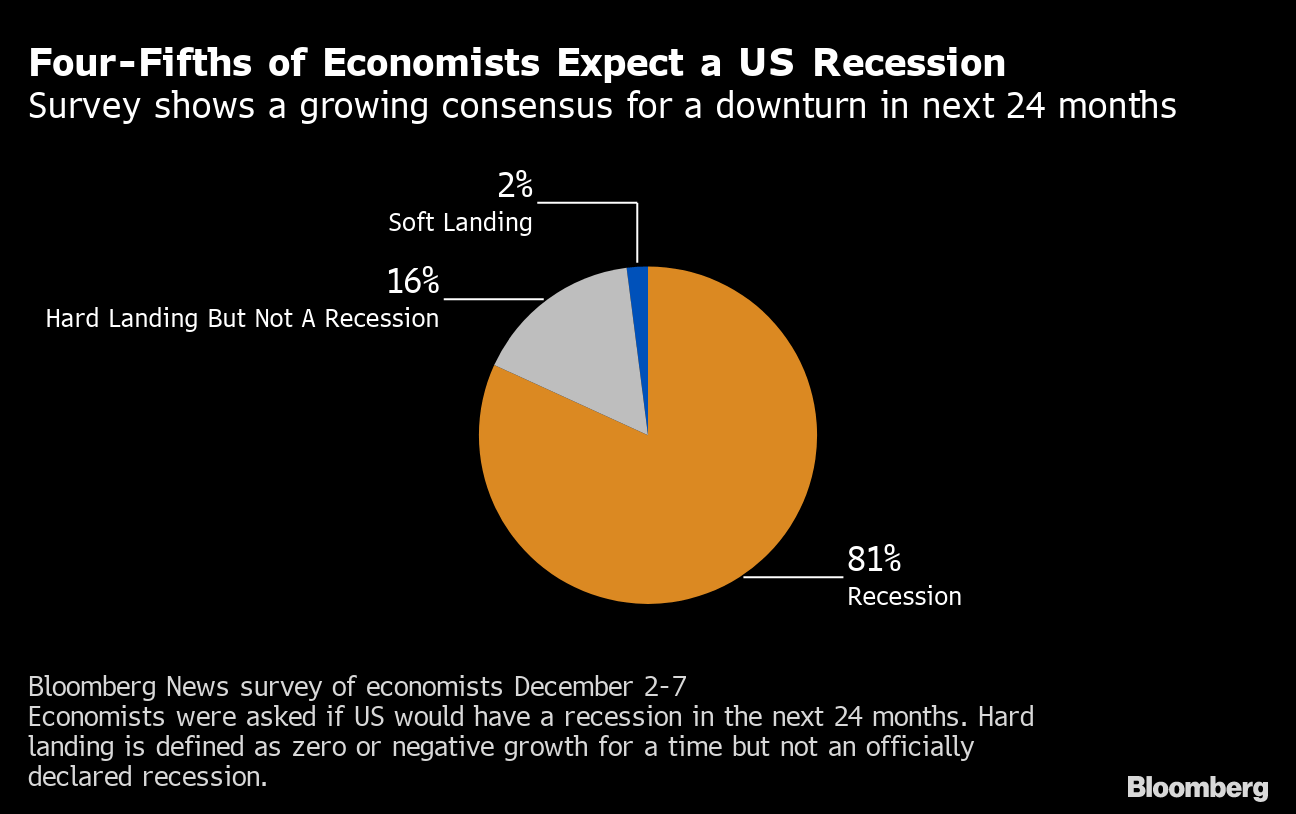

3. Bloomberg Monthly Survey of Economists. A monthly survey of economists conducted by Bloomberg in November revealed that the median estimate of the probability of recession at some point during the next 24 months 81%. The combined probability those forecasting a “non-recessionary hard landing” (16%) plus those forecasting a recession (82%), rises to a total of 98%. Only 2% of the economists surveyed believe a “soft landing” will occur.

Recession & Hard Landing Probabilities (Bloomberg)

Corporate Executives: Expectations of Recession

Below are examples of two highly reputable surveys that document the expectations of corporate executives regarding the probability of recession:

4. Conference Board CEO Confidence. According to a survey conducted by the Conference Board in between September 19 and October 3 of 2022, 98% of US CEOs say that they are preparing for a recession in the next 12-18 months.

5. KPMG Banking CEO Outlook. According to a survey by KPMG conducted with 1,325 Bank CEOs, 85% of the respondents believe that the US will experience a recession in the next 12 months.

Fund Managers and Investors: Expectations of Recession

Below are examples of two surveys that document the expectations of fund managers, professional investors and retail investors regarding the probability of recession:

6. Bank of America Global Fund Manager’s Survey. According to the monthly Global Fund Managers Survey conducted by Bank of America in December 2022 (300+ fund managers participated), 68% of fund managers surveyed believe that a recession is likely in the next 12 months.

Fund Manager Survey: Recession Probabilities (Bank of America)

For periods in which the economy was still in expansion – other than the prior month of November 2022 (in which 77% of managers said recession was likely) — this was the highest average expectation of a future recession recorded in the history of the survey. Indeed, the survey only registered higher expectations of future recession during periods in which the economy was already deeply in recession. Current expectations of recession by the fund managers surveyed are vastly above what they were right before the 2007-2009 Global Financial Crisis or right before the 2020 COVID recession.

7. Bloomberg MLILV Pulse Survey. According to the MLIV Pulse Survey, which is a weekly survey of professional and retail investors conducted by Bloomberg, between December 5, 2022 and December 9, 2022, 81% of investors said that they expect a recession in 2023. 65% expect a “mild recession”, while 16% expect a “long and ugly” recession. Only 19% of the investors surveyed believe that the US will avoid a recession.

Retail & Professional Investors Recession Probabilities (Bloomberg)

Reflections on What the Consensus About Recession Means for Investors

In this article we have conducted a review of numerous sources regarding the expectations of a recession in the US. Our sources covered several important constituencies, including professional economic forecasters, corporate executives, fund managers, professional investors and retail investors.

We have shown that the depth and breadth of the prevailing “consensus” regarding the likelihood of a US recession (at some point during the next 12 months) is unprecedented. Never before in history have estimates of the probability of a future recession been so high and/or the pervasiveness of these estimates been so broad – particularly during a time of economic expansion, prior to the occurrence of an actual recession.

This state of affairs naturally gives rise to the following questions:

1. Given the depth and breadth of the consensus regarding the probability of a US recession, have all of the potential negative effects of this prospective recession already been fully discounted by the stock market?

2. Assuming that a recession actually materializes, is there any more downside risk left in the US market?

When presented with the sort of data documented in this article many investors and traders will be tempted to arrive at the rather facile conclusion that just because average estimates of the probability of recession by economists, corporate executives and investors is currently very high – i.e. that recession is the “consensus view” — that the market has already “fully discounted” the negative effects of a prospective recession. This would be an incorrect and dangerous inference.

Ironically, it appears that the expectation of recession has become so “normalized” that many market participants may have become complacent about the potential risks that a recession could bring to the market.

Therefore, the interesting thing about the current state of affairs may not be that a historic consensus recession has become established. The interesting thing may be that a “consensus about a consensus” may have surreptitiously formed. Specifically, we should ask whether a “consensus” or perhaps a “shared feeling” has emerged that “the bad news has already been discounted, so we don’t have to worry about it.”

Would it not be ironic, indeed, if this “complacency about consensus” is what sets up the behavioral conditions for a nasty surprise in 2023?

One of the things we do constantly, and in great depth, in Successful Portfolio Strategy is to examine risks versus rewards in our overall asset allocations and in our individual positions. We are constantly looking for opportunities to find the things that most others are not even looking for and to bring into focus the things that most others are not seeing. Could it possibly be that merely “observing” the consensus about recession is a little “too obvious”? Could there be something about this particular consensus that many or most market participants are not seeing? Could the consensus actually be blinding many market participants to risks that are lurking?

Indeed, in our very next article, we are going to show in detail why existence of a consensus about the probability of a recession does NOT imply that the risks of a recession are already fully discounted in the stock market, nor or that there are no further downside risks that should be expected in connection with a prospective future recession. As a preview to that article, we will discuss in detail the following four points:

1. Estimates of probability can and do change. Estimates of probability of recession can move from high to higher; and then from higher to absolutely certain. If perceptions of the odds of recession become more certain, market prices will adjust downward accordingly. Furthermore, perceptions about the particular recession that is “expected” can shift from “certain” to “worse than expected.” Whatever it is that market participants are expecting could turn out to be (or feel) considerably worse than they currently expect — and this would result in downside that they do not currently foresee.

2. Recessions come in many flavors. Don’t confuse estimates of probability with estimates of severity. Currently the consensus expectation is that a prospective recession, if it occurs at all, will probably be both mild in intensity and short in length. If perceptions shift, causing estimates of recession intensity to increase and/or expectations of recession duration to lengthen, then market prices will probably adjust downward significantly.

3. The sell-side thinks the prospective upcoming recession will be no big deal. Do you agree? Look closely at sell-side estimates to estimate implied probabilities and severity. When one analyses these estimates in detail, one finds that to the extent that a recession is anticipated at all, it is expected to be extraordinarily mild. What if these expectations shift? Furthermore, when has the sell-side ever been right when it downplays risk of recession?

4. Market prices are saying: “What Recession? Who cares?” If one looks closely at market prices, one can infer implied estimates of the probabilities and severity of recession. Price-based indicators in both the bond and equity markets clearly show that to the extent that market prices have discounted a recession at all, it would be an extraordinarily mild one. History shows that these expectations can shift, and sometimes violently. History has also shown that market prices often remain “calm for too long” and then “panic too much.”

An Invitation & Final Food for Thought

In our next article here on Seeking Alpha we are going to explore each of the above points in depth and also reach some unexpected conclusions.

The point we want to leave you with is that there is a major market opportunity that is potentially developing right now. Understanding what sort of an opportunity a “consensus” can create is not obvious. Recognizing and exploiting an opportunity requires data, analytical tools, the proper mental models and second-level thinking. (Click the “Follow” button on the top right or bottom right of this article to follow the analysis.)

Be the first to comment