Florida Chuck/iStock Editorial via Getty Images

Frontier Airlines (NASDAQ:ULCC) reported second quarter earnings on the 27th of July. Shares of Frontier Airlines ended up over 20% higher in Thursday’s trading session, but this had little to do with the airline’s earnings which were not great but also not bad. In this report, I take a quick look at the reason why Frontier Airlines stock surged and I will be analyzing the company’s results, management comment and guidance.

Why Did Frontier Airlines Stock Surge?

Frontier Airlines stock appreciated significantly after Spirit Airlines (SAVE) terminated the merger agreement with the airline. Airline stocks had been under pressure for quite some time as fears of a recession mounted and Frontier Airlines had some pressure on share prices as well as its transaction to acquire Spirit Airlines was financed mostly with company stock and as a result would dilute existing shareholders. Furthermore, JetBlue (JBLU) went aggressive in its attempt to acquire Spirit Airlines and there might have been some fear that Frontier Airlines would follow suit and overpay for Spirit Airlines.

As I explained in a recent report following the combination agreement between JetBlue and Spirit Airlines, shares of Frontier Airlines received significant lift as Spirit Airlines calling off the transaction removed any concern about Frontier Airlines overpaying or any dilutive impact.

Frontier Airlines will receive $25 million from Spirit Airlines and an additional $69 million upon completion of the transaction with JetBlue as stipulated in the initial merger agreement. This $94 million in my view is not really a reason for Frontier Airlines shares to jump but somewhere it must feel nice for the company that it led JetBlue pay $1 billion more than it wanted to spend on Spirit Airlines itself and they are actually receiving money for that.

Frontier Airlines Faces Fuel Environment Reality

Earnings Frontier Airlines (Frontier Airlines)

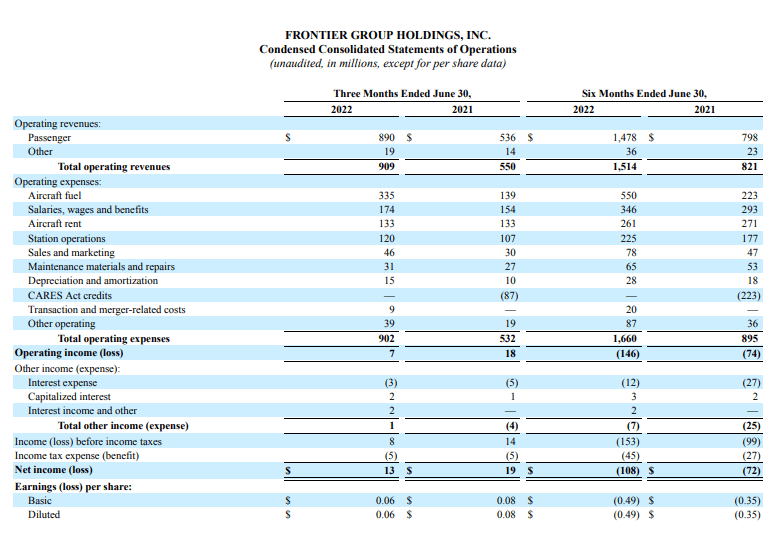

During the second quarter, Frontier Airlines faced the reality of the current fuel price environment. Revenues increased by $359 million compared to last year and 43% compared to 2019, but its cost increased by $370 million, over half of which was driven by a combination of higher fuel consumption and prices. So, operating income actually decreased year-over-year though adjusting for the CARES Act credits, profitability improved by $76 million.

It wasn’t enough to beat the consensus. Frontier Airlines beat on revenues by $43.24 million but missed EPS by $0.03. Initially, the ultra low-cost carrier for adjusted operating expenses of $545 million to $555 million. This already drove costs up by $0.06 covering much of the miss, while fuel cost per gallon exceeded the upper bound of the guided range by 13% providing a $0.17 headwind. Much of that was absorbed by strong unit revenues but not completely resulting in earnings miss.

Frontier Airlines had guided for a 10 to 12 percent increase in capacity and realized that capacity expansion with an expansion of 10.4%

Is Frontier Airlines a Buy?

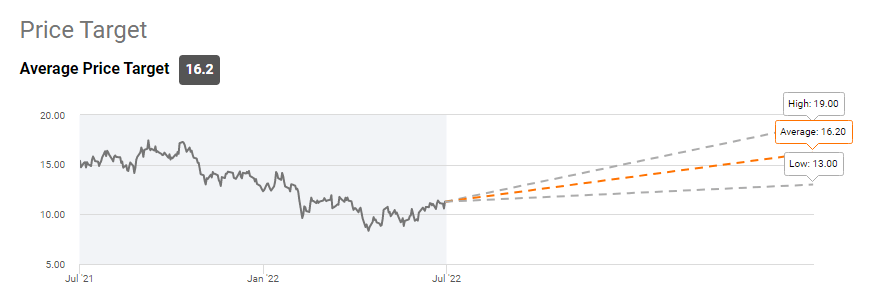

Wall Street price target ULCC stock (Seeking Alpha)

With its current performance, one can wonder whether Frontier Airlines stock is a buy. If you ask Wall Street analysts, they will say that is indeed the case with a price target that around 20% higher than Thursday’s closing price.

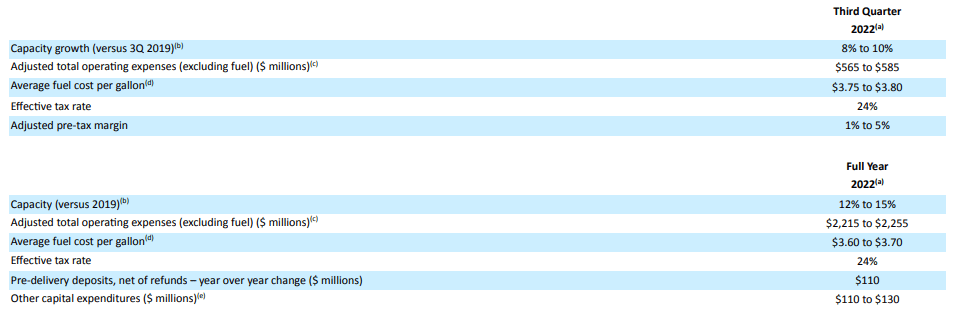

Guidance Q3 2022 (Frontier Airlines)

One thing that I can appreciate about Frontier Airlines is that the company is growing capacity. It is not recovering capacity growth, but already operating above pre-pandemic levels with a fuel-efficient fleet which helps the airline weather the current fuel price environment. The company foresees fuel prices at $3.75 per gallon go $3.80 per gallon. Currently prices are at around $3.35 per gallon roughly 20% lower than a month ago. We don’t know what fuel prices will do in the remainder of the quarter but the current fuel price levels could indicate that average fuel costs will below the guided range. With targeted capacity growth and fuel costs possibly be below the guided range, Frontier Airlines could be worth considering for investment.

Conclusion

Frontier Airlines stock gained significantly, but this was driven by the announcement that the merger agreement with Spirit Airlines was terminated and not so much its in-quarter performance where the company exceeded revenue expectations but costs including and excluding fuel were higher than anticipated. Wall Street has a buy rating on Frontier Airlines stock and much of that already materialized on Thursday. While I am not a huge fan of Frontier Airlines, I am liking the fact that they are a step ahead in the recovery trajectory and operate a fleet with almost 70% next-generation aircraft which should give them an edge in the competitive field.

Be the first to comment